The Double E pipeline is set to deliver gas to the Waha Hub before the Matterhorn Express pipeline provides sorely needed takeaway capacity, an analyst said. (Source: Shutterstock.com/ Summit Midstream)

Summit Midstream Partners announced an open season for capacity on its Double E Pipeline, a currently underutilized transport that will play a key role in the Permian Basin’s future, an analyst said.

The open season commenced April 1 and closes at 2 p.m. Central Time on April 29.

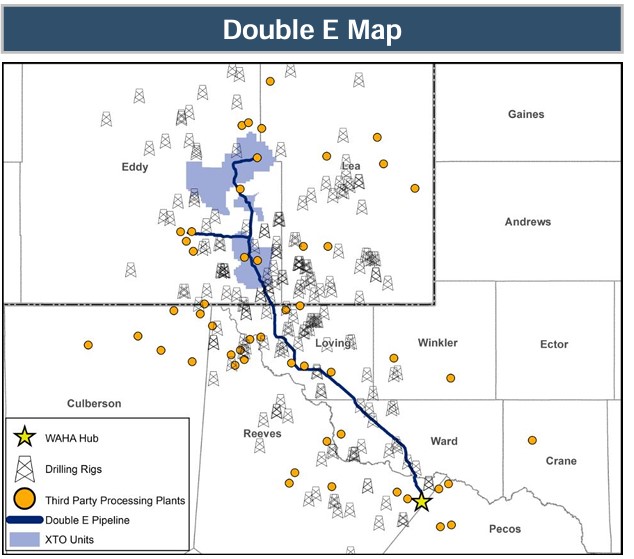

Double E begins at the Summit Lane gas processing plant in New Mexico and terminates about 135 miles away at the Waha Hub near Pecos, Texas.

Recently, gas has been so plentiful at the Waha Hub that spot prices have dipped into negative territory.

However, that should change once Matterhorn begins to take gas away from the Waha Hub sometime later this year.

“It will be important for Double E to be able to deliver more gas into Waha and other points before Matterhorn starts up next quarter,” Jack Weixel, senior director of East Daley Analytics, wrote in an email to Hart Energy. “I think the idea is that Matterhorn will take away 2 Bcf/d of gas from Waha, so there will be more space at Waha to deliver gas into.”

Double E is soliciting non-binding bids for the firm transportation service rate schedule of Double E’s tariff, according to the press release from Summit Midstream.

“Double E is an interesting pipe,” Weixel said. “It is currently severely underutilized.”

According to East Daley’s tracking numbers, during the last quarter of 2023 the line carried an average 386 MMcf/d. The line’s capacity is 1.35 Bcf/d. Weixel said the line will receive some incremental volumes of about 300 MMcf/d from the EOG Resources' Janus plant by second-quarter 2025, but still has much more room to carry gas.

Meanwhile, gas producers in the Permian are anxious for the opening of the Matterhorn Express.

“The market has been eagerly waiting on Matterhorn because capacity out of the Permian is so tight,” Weixel said. “It’s so tight that even the slightest disruption to outbound capacity results in negative prices.”

Last month, two maintenance periods on two lines — Kinder Morgan’s Permian Highway and El Paso’s North Mainline — caused the Waha Hub price to dip into the negatives twice.

From April into May, maintenance on the jointly-owned Gulf Coast Express pipeline is expected to lower Waha prices again.

“All of these maintenance events effectively cut capacity out of the basin, bottle up supply and send prices tumbling,” Weixel said. “Matterhorn is super important to relieve this condition and Double E wants to take advantage.”

The Permian is second to the Marcellus/Utica Basin in U.S. gas production. However, while the Appalachian basins are gas-focused, natural gas from the Permian is a byproduct of crude oil production called associated gas.

Permian gas production is consequently driven by the price of crude, rather than the price of gas, which nationally has been under $2 per MMbtu since February.

Recommended Reading

Patterson-UTI Braces for Activity ‘Pause’ After E&P Consolidations

2024-02-19 - Patterson-UTI saw net income rebound from 2022 and CEO Andy Hendricks says the company is well positioned following a wave of E&P consolidations that may slow activity.

Oil and Gas Chain Reaction: E&P M&A Begets OFS Consolidation

2024-04-26 - Record-breaking E&P consolidation is rippling into oilfield services, with much more M&A on the way.

E&P Earnings Season Proves Up Stronger Efficiencies, Profits

2024-04-04 - The 2024 outlook for E&Ps largely surprises to the upside with conservative budgets and steady volumes.

Chesapeake Slashing Drilling Activity, Output Amid Low NatGas Prices

2024-02-20 - With natural gas markets still oversupplied and commodity prices low, gas producer Chesapeake Energy plans to start cutting rigs and frac crews in March.

Jerry Jones Invests Another $100MM in Comstock Resources

2024-03-20 - Dallas Cowboys owner and Comstock Resources majority shareholder Jerry Jones is investing another $100 million in the company.