In the week since our last edition of What’s Affecting Oil Prices, Brent prices fell $1.54 a barrel to average $76.02. Brent will likely remain weak through the week ahead, averaging closer to $72 dollars a barrel.

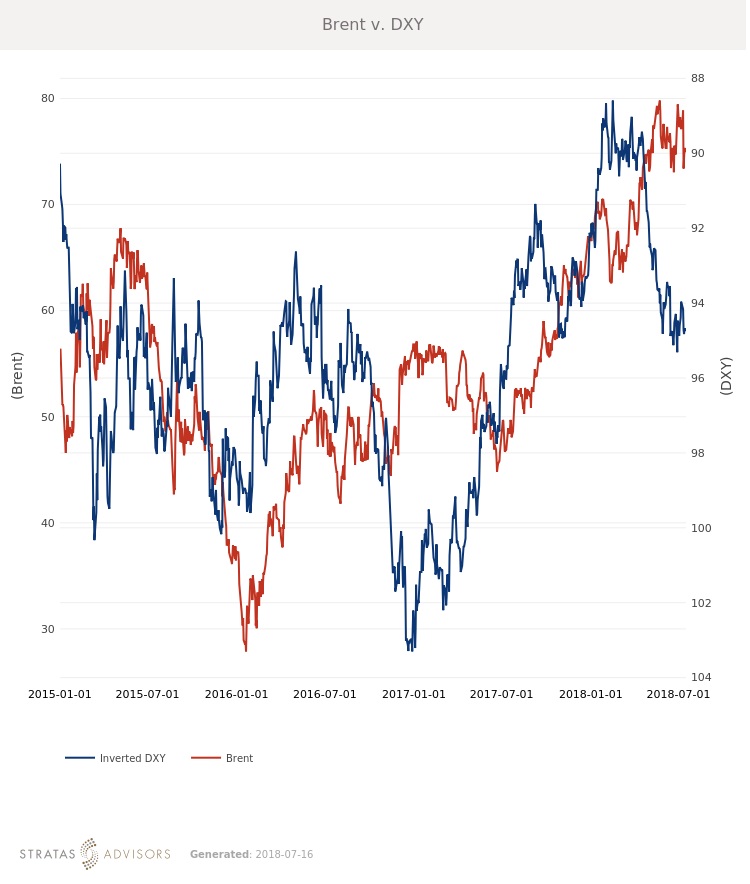

Brent and WTI both fell last week as supply outages eased and Russia and other producers continued to reiterate that they could provide additional supplies if needed. Brent declined $1.54/bbl while WTI declined $1.86/bbl. Prompt Brent has actually fallen below the September to December futures contracts, creating a shallow contango. Given an ongoing strike in Norway, and kidnappings and unrest in Libya and Iraq there could be some support this week, but it is unlikely to reverse the downward trend.

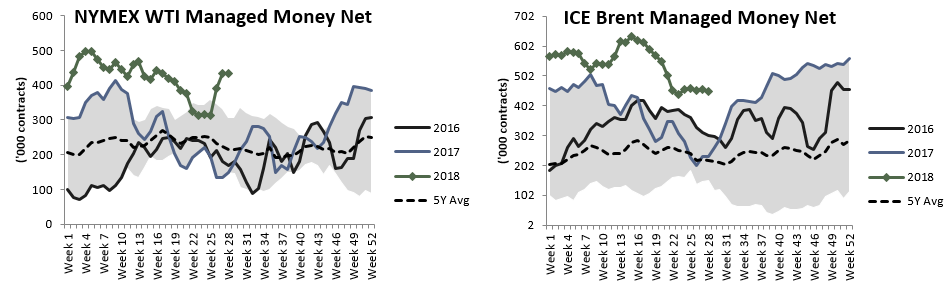

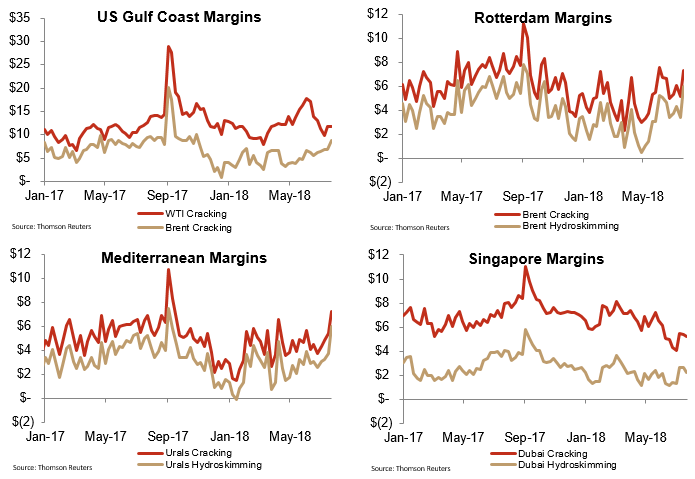

While positioning has not seen a dramatic change, sentiment will likely pressure prices lower with the appearance of a slight contango in the next four months. Additionally, sporadic outages have not been enough to have a serious impact on global supply and many major producers continue to message that production will be increasing. With prices lower, margins have bounced back and are now at or above their five-year average in most enclaves, which could support higher run rates where possible.

Geopolitical: Positive

Geopolitics will be a positive factor in the week ahead as unrest in Libya and Iraq provide some supply outages.

Dollar: Neutral

The dollar will be a neutral factor in the week ahead as fundamental and sentiment-related drivers continue to have more impact on crude oil prices.

Trader Sentiment: Negative

Trader sentiment will be a negative factor in the week ahead after prompt month Brent slipped into contango.

Supply: Neutral

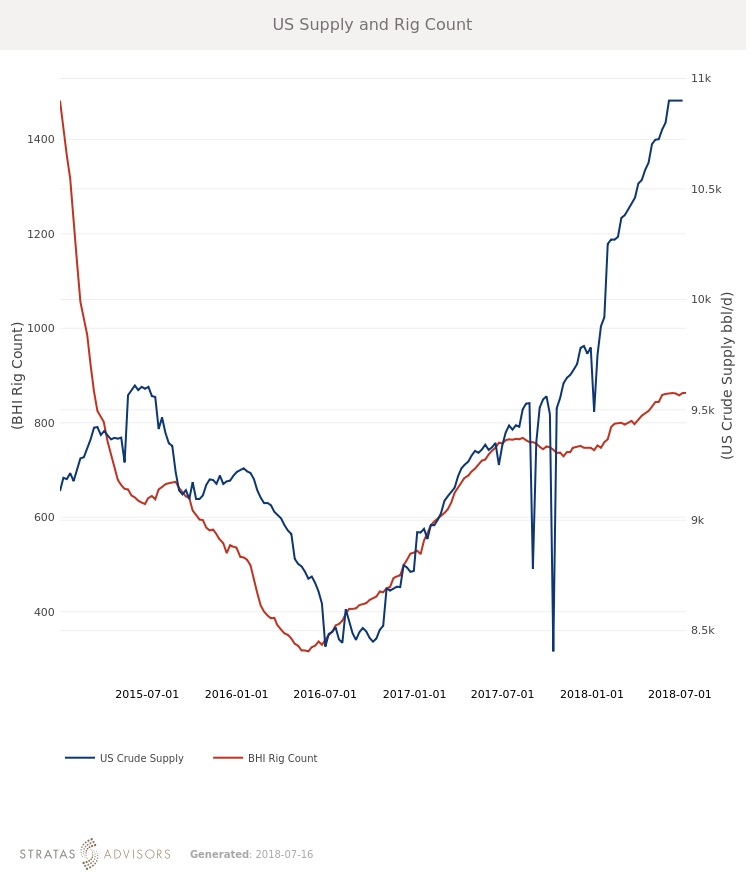

Supply will be a neutral factor in the week ahead. While short term outages in Libya and Iraq should theoretically provide support, Russia and other major producers continue to broadcast their ability to raise production.

Demand: Neutral

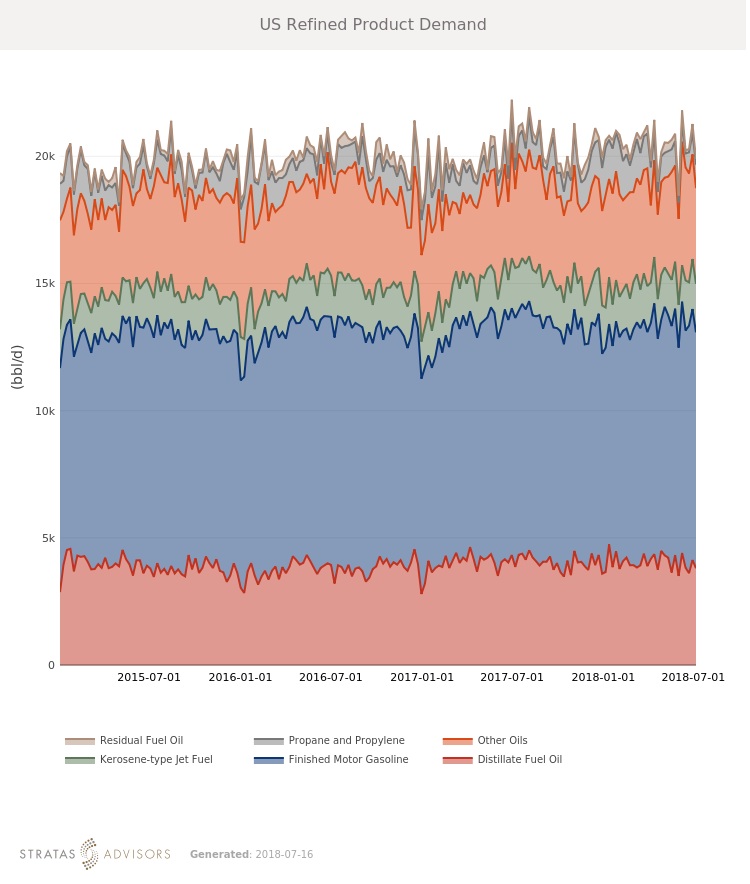

Demand will be a neutral factor in the week ahead as rising prices fail to stymie demand.

Refining: Positive

Refining will be a positive factor in the week ahead, with margins in most enclaves now at or above their five-year seasonal average.

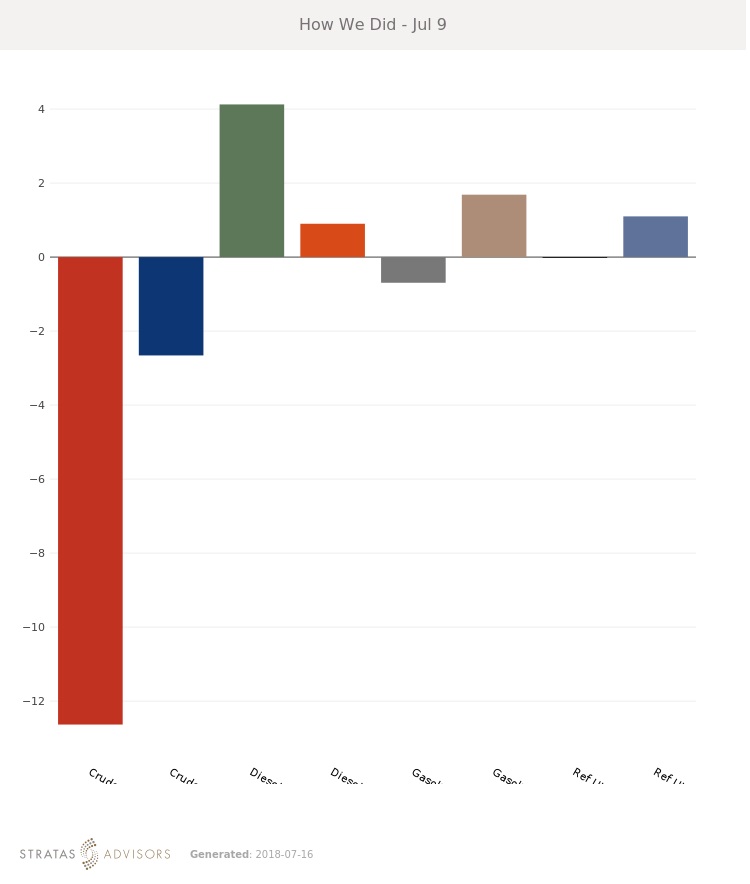

How We Did