AUVs are on their way. With vast scope for their application, AUVs are finally gaining pace in the commercial sector. The technology, which has its origins in military activities such as mine counter-measure and rapid environmental assessment, also has a strong presence in research activities, from research mapping to environmental sensing. In fact, the military and research sectors have strong links that enable collaboration; therefore, some units can be used across the sectors. The two sectors currently form 97% of AUV demand. However, Douglas-Westwood’s “World AUV Market Report 2014-2018” forecasts an annual growth of 36% in the commercial sector, predominantly driven by deepwater oil and gas activities, expanding the share of the total market from 3% in 2014 to 8% in 2018.

Overview

AUVs have no umbilical connecting them to a host support vessel (as opposed to ROVs) as these have the advantage of carrying both onboard power and the computer capability to travel a preset path through the water, using a combination of internal and external positioning sources as well as sensors that give direction, depth, altitude and speed. AUVs, however, do not provide real-time data such as video. They are used by civilian researchers and academics, commercial survey and inspection companies, and by the world’s militaries to either provide information about the seabed; identify objects on the seabed or in the water column; or provide a means of observing physical, chemical and biological processes. AUVs can be used to survey an area in a regular pattern or to follow a linear feature such as a pipeline.

The benefits of AUVs include operability in a wide variety of water depths and where surface vessels cannot be used due to surface restrictions/obstructions. They have a wide range of deployment options ranging from manual to dedicated vessels and can help reduce threats to personnel by increasing either the distance between hazard and operator or by performing reconnaissance in advance of manned operations.

Key developments

There are some key developments that should enable strong commercial uptake from 2014. These include sensors, battery endurance and positioning. Multiple sensors form a key component and continue to increase in data quality and resolution. Endurance also is under constant development, with rechargeable batteries powering the majority of AUVs now in use, while nonrechargeable batteries offer greater endurance but at a significant cost.

A small number of AUVs use fuel cells, but their use is not widespread due to concerns with the storage and disposal of the chemicals. Even small AUVs typically now have quoted endurance of more than 10 hours, with larger vehicles in the 50- to 70-hour range. High endurance is central as it enables AUVs to offer vast reduction in time lost in operations in addition to the time savings when turning from one survey line to another when compared to a survey vessel towing sensors in deepwater.

Unmanned launch and recovery is a goal of many developers as that phase of operations is perhaps the riskiest for the personnel involved. The launch and recovery requirement and methodology for AUVs vary. Smaller units are routinely deployed from the beach or small craft, whereas larger vehicles require the use of either a vessel’s deck crane or a dedicated launch and recovery system. This is an area in which many operators think there should be further improvements.

Commercial applications

The oil and gas industry is historically conservative when adopting new technologies; however, the above developments will act as enablers for commercialization, with 2014 expected to be a pivotal year. Growing energy demand globally will be met by supply from increasingly deep waters as easy-to-reach reserves mature.

Mature offshore fields and remote areas represent higher capex per barrel, while oil prices are stabilizing. The result is that oil and gas companies are striving for the most cost-effective solutions. AUVs are widely accepted to be cost-effective and have been proven as an optimum solution in harsh environments.

Although shallow-water E&P will remain dominant during the next five years, most commercial demand for AUVs is expected to come from deepwater in the “Golden Triangle” of Brazil, Gulf of Mexico (GoM) and West Africa. Deepwater capex is expected to double over the next five years, with $260 billion to be invested as the market continues to recover from the global economic downturn.

Growth in maintenance markets is a key indicator for life-of-field inspection (LFI) and pipeline inspection. Offshore drilling is expected to boost oil and gas site survey activities, the main commercial application of AUVs, accounting for almost a third of commercial demand. To a lesser extent, AUVs also are expected to increase utilization rates in shallow waters.

With increasing regulations and costs, LFI is a long-term goal for deepwater and remote production facilities inspection, run by unmanned or hybrid (AUV-ROV) vehicles. The application is still in precommercial stages but has great potential to demand a number of units for installations in Angola, Nigeria, Brazil, South Asia, the North Sea and the U.S. GoM since LFI using AUVs is more applicable in deeper waters. Site surveys also will drive demand again in the Americas and Asia, while Africa should be the largest market, demanding 47% of the units in 2018.

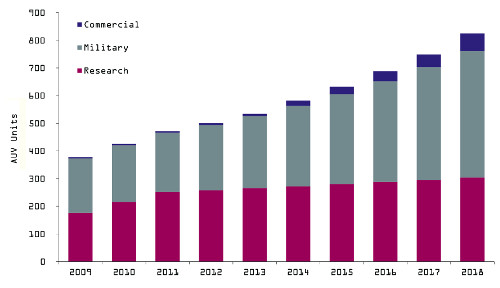

The chart shows Douglas-Westwood’s demand forecast for AUVs. The combined sectors account for 97% of global AUV demand in 2014. The commercial sector is expected to show exponential growth, more than tripling demand from 2014 to 2018. The total number of units across all sectors is expected to exceed 800 by 2018, an increase from about 600 in 2014.

The global AUV demand forecast shows a steady increase in the number of AUV units used in the commercial, military and research sectors from 2009 to 2018. (Source: Douglas-Westwood)

North America will remain the overall leading region in the next five years, demanding most AUV units. However, other regions will become more active in all sectors, which should mean a decrease in the proportion of active units for the region, mainly driven by military activities in developing economies such as China and Brazil that are increasingly investing in their navies.

Turning point

Douglas-Westwood has forecast that the military sector will remain the largest AUV market in the next five years, driven by military investment from the developing economies. The sector is likely to direct less investment into AUV R&D, while commercially driven developments grow. The ocean research sector also will remain strong with increasing attention to topics around environmental issues, resulting in a growing demand for data from environmental sensing and research mapping, including from deepwater and the Arctic. As AUV technology matures in such applications, it should enable continued growth in those areas that are unsuitable for conventional access methods.

For the commercial sector, 2014 could be a turning point in AUV market uptake. The commercial use of AUVs has seen only moderate growth in recent years. The technology has evolved, and while oil and gas operators remain risk-averse, opportunities in the commercial sector could increase, enabled by developments in areas such as battery endurance, navigation systems, tracking systems, vehicle stability, data and imagery.

Barriers may be primarily in launch and recovery systems for larger units and data transmission as AUVs do not offer real-time data. These areas should be progressively addressed by developments such as unmanned launch and recovery systems, hybrid vehicles and docking stations for in-water charging, and improved through-water data transmission.

The increased economic challenges of deepwater oil and gas developments lead to a desire to introduce cost-effective approaches. AUVs have been proven to be optimum cost-effective solutions for surveys and inspections as opposed to the higher costs of vessel-based activities. Factors include operation and time costs and reducing direct human involvement in activities in high-risk environments. Douglas-Westwood expects further increases in AUV use in deep waters and under-ice as an alternative to ROVs.

AUVs are still considered an emerging technology and require more uptake and investment before posing a significant substitution risk for surface vessels and ROVs. However, 2014 is expected to represent the first year of significant growth, which should allow the technology to be the industry eyes in the deepest waters.

Recommended Reading

Spicewood Acquires Multiple Permian Basin Mineral Interests

2024-10-22 - Spicewood Mineral Partners added mineral and royalties interests in the Midland and Delaware basins, operated by E&Ps including Occidental Petroleum, ConocoPhillips and BP.

WhiteHawk Badgers Response from PHX on Acquisition Offer

2024-11-12 - WhiteHawk Energy’s move follows months of unsuccessful attempts to engage PHX Mineral's leadership, including a previous stock-for-stock merger proposal in August 2023.

Marketed: Stapleton Group Gulf Coast Texas Opportunity

2024-10-21 - Stapleton Group has retained EnergyNet for the sale of 51,816 non-producing net mineral acres in Walker, Montgomery and San Jacinto counties, Texas.

Alliance Adds Mineral Interests to Its Permian-weighted Portfolio

2024-10-28 - Alliance Resource Partners reported purchasing about $10.5 million of mineral assets in the third quarter.

In Busy Minerals M&A Year, Freehold Grabs $152MM Midland Interests

2024-12-10 - Canadian player Freehold Royalties is getting deeper in the Permian with a CA$216 million (US$152 million) Midland Basin acquisition as minerals buyers intensify M&A in the basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.