Despite the downturn in commodity prices, operators and other prospective investors have demonstrated a notable interest in the SCOOP and STACK regions of the Anadarko Basin in Oklahoma (Figure 1). The STACK (“Sooner Trend Anadarko Canadian Kingfisher”), with an overpressured hot spot, has illustrated some particularly eye-popping results, boasting some of the highest oil well 30-day IP rates in the country.

Stratas Advisors currently forecasts West Texas Intermediate (WTI) to range between about $50 and $55 through year-end 2017. At those prices and assuming all else is equal, Stratas believes that this area will continue to attract investment. As illustrated in Figure 2, the STACK has consistently generated above-average IP, and most of the industry believes 2016 results will continue to impress. Stratas Advisors analyzed just more than 10,000 oil wells drilled in 2014 and 2015 across several plays, and the results for the STACK were strong even just based on the historical drilling that has been reported.

Wells targeting the various reservoirs within these formations tend to exhibit a slower decline pattern on average, yielding a steadier flow for the first six to 12 months of the well’s life. Decline patterns seen within the region also exhibit large EURs when coupled with higher starting points. New operators to the region are looking to optimize well designs to perpetuate these results.

The corresponding economics for these wells show why interest will be sustained. Using results from 162 wells that were drilled within the STACK in 2014 and 2015, Stratas analyzed how key operators compare and contrast. Of particular interest was Newfield Exploration. This company has stepped out of the pack and drilled laterals that were often more than twice as long as others in the area, with notable success in terms of IP rates and expected EURs.

Figure 3 compares the 30-day IP rates of the wells against their resulting EURs (Mboe). The majority of wells posted IP rates between 0.2 Mboe/d and 1 Mboe/d. The associated EURs show a range between 200 Mboe and 1 MMboe.

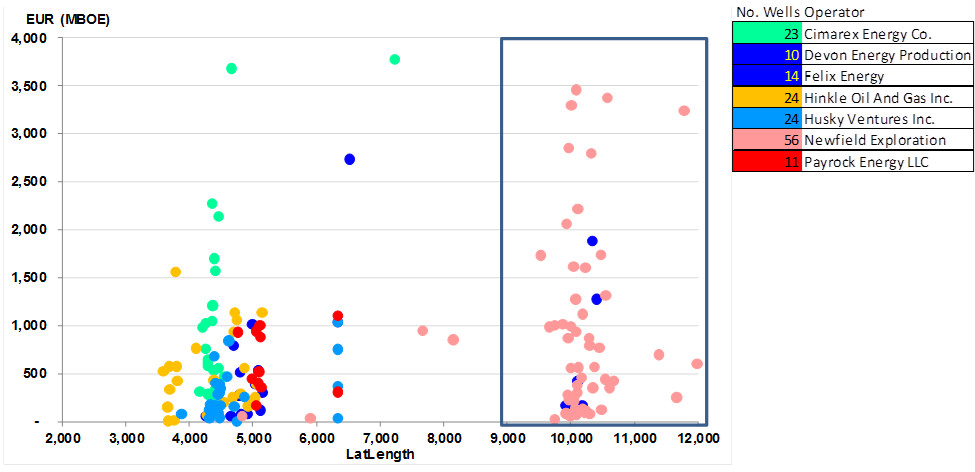

FIGURE 3. This figure (right) compares 30-day IP rates (Mboe/d) to EUR (Mboe) for top operators within the STACK. (Source: Stratas Advisors)

Newfield drilled numerous wells that fall outside of this range, and it has been able to achieve much larger production results.

The median Newfield well exhibited an IP of just under 0.9 Mboe/d, with resulting median EURs at just under 590 Mboe. But of particular interest is the number of wells that show up in the tails of the distribution. As shown in Figure 4, Newfield was able to drill a number of wells, predominately located in Kingfisher and Canadian counties, which produce at rates far in excess of what its competitors were able to accomplish. The average EUR was more than 900 Mboe. The large spread between the median and the average highlights the existence of a number of significantly larger wells.

When analyzing these results relative to the well designs, another aspect stands out (Figure 4). Newfield made the decision to drill some of the longest lateral lengths in the area, averaging about 3,048 m (10,000 ft). Devon and Felix Energy also have drilled a few laterals at similar lengths, but the majority of the 162 wells Stratas analyzed had more modest lengths, ranging between 1,219 m and 1,524 m (4,000 ft and 5,000 ft). Figure 5 illustrates the difference in completion approaches and the resulting reserve estimates.

Other completion-related concepts to keep in mind include the concept that operators are using slickwater and crosslink frack fluids most commonly in their designs. They also have coupled this with raw sand as the main proppant type. Using these relatively cheaper completion materials, operators are able to benefit from lower service costs per well. In general, low commodity prices have pushed operators to emphasize their drilled but uncompleted inventories. However, many operators within the midcontinent region are able to remain focused on drilling new wells, maximizing the potential recovery. Stratas Advisors estimates that the half-cycle drilling and completion costs are currently averaging between $6 million and $7 million per well.

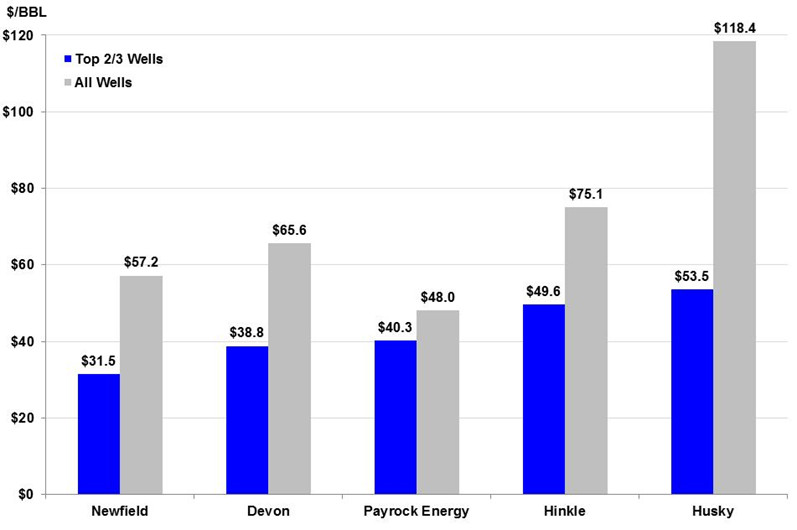

Operators in the STACK have been able to capitalize on decreasing service sector costs and better production results, posting NPV10 estimates at or below $50/ bbl. As part of the analysis performed, the breakevens for the aforementioned 162 wells were calculated using an average well cost of $6.5 million. The breakevens were then ranked and averaged for the top two-thirds of the wells drilled. Figure 6 illustrates the results of the top operators.

The three top operators were Newfield, Devon/Felix and Payrock Energy (recently acquired by Marathon in June 2016), which all showed positive economics at WTI prices below $45/bbl for most of the activity. When considering all the wells drilled and weighting the results equally, the average breakeven goes up considerably, with only one company, Payrock, showing positive results below $50. Although Payrock has drilled fewer “dogs” so far, one must consider that they have thus far only drilled about 20% of the total number of wells that Newfield has drilled and about half the number of the other operators. Given the results of the top-tier wells, positive economics should be easily obtained on a total campaign level for at least the top three companies. With further delineation and optimization of completion techniques, it is likely that these operators will continue to drive down costs and put even more pressure on breakeven prices.

For more information, contact Jessica Pair at 713-260-4604 or jpair@hartenergy.com.

Recommended Reading

Phillips 66’s NGL Focus, Midstream Acquisitions Pay Off in 2024

2025-02-04 - Phillips 66 reported record volumes for 2024 as it advances a wellhead-to-market strategy within its midstream business.

Rising Phoenix Capital Launches $20MM Mineral Fund

2025-02-05 - Rising Phoenix Capital said the La Plata Peak Income Fund focuses on acquiring producing royalty interests that provide consistent cash flow without drilling risk.

Equinor Commences First Tranche of $5B Share Buyback

2025-02-07 - Equinor began the first tranche of a share repurchase of up to $5 billion.

Q&A: Petrie Partners Co-Founder Offers the Private Equity Perspective

2025-02-19 - Applying veteran wisdom to the oil and gas finance landscape, trends for 2025 begin to emerge.

Chevron Makes Leadership, Organizational Changes in Bid to Simplify

2025-02-24 - Chevron Corp. is consolidating its oil, products and gas organization into two segments: upstream and downstream, midstream and chemicals.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.