CGG’s Ocean Sirius cuts a lonely swath on a recent survey. (Source: CGG)

The years 2015 and 2016 have seen some remarkable discoveries—Zohr in Egypt, Teranga offshore Senegal and, just recently, Apache’s massive oil discovery in the Permian Basin. But these significant announcements belie a deeper problem. The industry just isn’t exploring as much as it used to, and when it does, its success rate is dismal.

Several factors come into play here, but by far the most important are the continued depressed commodity prices. Major discoveries are most likely in deep water, and these fields simply aren’t economic at $50 oil. Add to that the fact that $50 oil sounded downright dreamy in January 2016, when prices dipped into the $28/bbl range, and most companies weren’t even considering the location of the next big elephant.

Why look for more oil when the world already has too much of it?

In some ways, of course, this makes sense—why look for more oil when the world already has too much of it? But an industry plagued by quarter-itis still needs to look farther into the future and consider the importance of reserves replacement, not to mention world demand.

Lying Low

According to an article by Gaffney, Cline & Associates, uncertainty over sustained low prices has caused companies, and their investors, to change their focus. “A clear trend has developed whereby investor interest has moved away from exploration and predevelopment assets to developed mature assets that can demonstrate an active and positive cash flow under the current market conditions,” the article stated. “These mature assets tend to have reduced subsurface uncertainty due to extensive data acquisition and production history, with EURs often determined solely by simple decline curve analysis.”

This type of focus can offset the need for exploration for quite some time, according to Leta Smith, director of IHSMarkit. “This actually can be substantial,” Smith said. “We did a study last year looking at field growth in terms of the reserve sizes, the 2P reserves. Sometimes it’s just having better data, but other times it’s actual field growth—finding another horizon to drill, drilling infill wells. Some of the larger fields that are more worthy of investment can increase in size by as much as 25%.” She cited Chevron’s recent decision to invest $37 billion in its Tengiz Field as a good example of this.

But this type of reinvestment can only go so far. A recent Deloitte webcast indicated that the industry needs to meet a demand growth of 1% to 2% yearly as well as overcoming natural field declines of between 7% and 8% annually. Before prices started falling, the industry was replacing 125% of its production, but today companies are spending about 80% of their capital just to keep their proved and developed reserve share flat.

The webcast also indicated that, based on the finding and development costs of 50 to 70 of the world’s largest E&P companies, the industry will need to invest at least $3 trillion between now and 2020, a figure that is a good 40% higher than spending plans for 2016.

Finding New Reserves

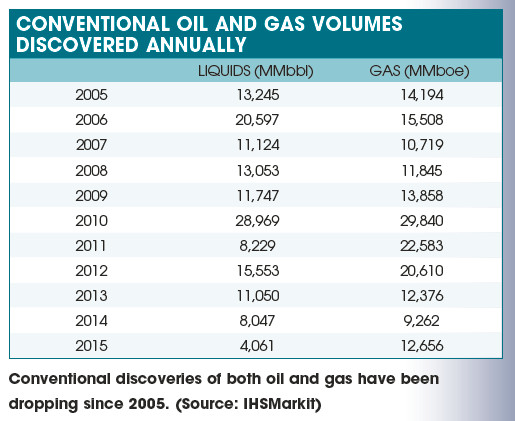

An even more disturbing trend is emerging, one that predates the drop in commodity prices. Data from both IHSMarkit and Richmond Energy Partners indicate that conventional discoveries are on the decline and have been for several years. Smith, for instance, authored a report that indicated that conventional discoveries outside of North America in 2015 were lower than any year since 1994. “I went back and looked at the discovery volumes since 1952, and we’ve never seen a downturn in discovered volumes that lasted more than a couple of years,” she said. “I think 2016 is going to be even lower than 2015, and 2015 was the fifth straight year in overall declining volumes found.”

“I think 2016 is going to be even lower than 2015, and 2015 was the fifth straight year in overall declining volumes found.”

A recent study by Richmond Energy Partners echoed these findings. “In a world awash with the stuff, new oil discoveries continue to be elusive,” the report stated, adding that global exploration drilling in 2016 is forecast to be down 73% over 2014 levels, with discovered oil volumes at a decade low. The current downturn certainly doesn’t help.

“Industry has responded to the downturn by slashing exploration budgets … Sustained oil prices above $60 per barrel are needed to stimulate exploration. The geology economic to explore at $40/bbl is actually quite limited,” the report stated.

Additional findings from the report include the fact that oil finding costs reached an eight-year high and that fewer than half of the 40 study group companies replaced production through conventional exploration over five years.

Managing Director Keith Myers said that no new multibillion- barrel conventional oil play has emerged since the presalt finds offshore Brazil in 2006 despite intense industry effort in frontier exploration. Exxon Mobil’s recent Liza discovery offshore Guyana might be the most significant, but whether it heralds a new multibillionbarrel province remains to be seen.

What Can Tip The Balance?

In addition to investing in mature fields, oil and gas companies also have a few other cards up their sleeves. For one thing, North American shale plays certainly can’t be ignored. While production in these plays has been curtailed significantly during the downturn, they remain prolific producers of oil and gas. And the inventory of drilled but uncompleted wells (DUCs) gives shale producers some future insurance.

But will this be enough? “I don’t think so,” Myers said. “In an unconventional play, when the price drops, the drillable area of the play shrinks. The higher the oil price, the more area you can afford to explore.

“At the same time, the larger the oil price, the more players explore conventionally. It’s not an either-or situation.”

Added Smith, “We’ve been looking at what kind of production we’re going to have in the future, and even by 2040 we’ll still be heavily dependent upon conventional oil and gas, particularly conventional oil.” She added that the U.S. can rely more heavily on its unconventional resources than other parts of the world.

According to Ed Morse, global head of commodities research for CitiGroup, the DUCs could indeed increase U.S. production in the short term. “If you model it at 600 bbl/d per well initial production, you get close to a 450,000 bbl/d increase from the beginning to the end of the period in which you are completing that inventory,” Morse said. “But then you don’t have that robust push again.”

Then there are the frontier areas. Mexico, for instance, could be the future home of major discoveries, and Exxon Mobil, Hess and Chevron recently signed a joint operating agreement to bid in that country’s deepwater bid round, which closes Dec. 5. According to a Reuters report, Energy Minister Pedro Joaquin Caldwell estimates that 76% of Mexico’s prospective resources are located in deep water.

“There’s going to be a farming out of PEMEX deepwater discoveries by the end of this year,” Morse said. “It looks like the line of companies interested in participating in that farm-out is very large, and they’re deep-pocketed companies.”

He added that the cost deflation in deepwater fields has not yet hit bottom. “We still have more deep cost deflation on the drilling side, cost deflation on the completion side and mammoth cost deflation on building platforms, where iron ore and steel costs have plunged,” he said.

Morse’s take on the near-term potential for price recovery indicates an eventual response to a supply shortage as deepwater projects continue to be postponed. “It’s likely there will be a price surge that can’t be dealt with solely by OPEC countries on the one hand and the U.S. on the other hand,” he said.

Contact the author, Rhonda Duey, at rduey@hartenergy.com for more information.

Read E&P's other October cover stories:

Geomechanics modeling service balances complexity, accuracy (Contributed by Baker Hughes)

Bubbling crude and understanding seeps (Contributed by MDA Geospatial Services Inc.)

Also check out this month's special section: SEG TECHNOLOGY SHOWCASE

Recommended Reading

ADNOC Contracts Flowserve to Supply Tech for CCS, EOR Project

2025-01-14 - Abu Dhabi National Oil Co. has contracted Flowserve Corp. for the supply of dry gas seal systems for EOR and a carbon capture project at its Habshan facility in the Middle East.

ProPetro Agrees to Provide Electric Fracking Services to Permian Operator

2024-12-19 - ProPetro Holding Corp. now has four electric fleets on contract.

Delivering Dividends Through Digital Technology

2024-12-30 - Increasing automation is creating a step change across the oil and gas life cycle.

Tracking Frac Equipment Conditions to Prevent Failures

2024-12-23 - A novel direct drive system and remote pump monitoring capability boosts efficiencies from inside and out.

E&P Highlights: Dec. 16, 2024

2024-12-16 - Here’s a roundup of the latest E&P headlines, including a pair of contracts awarded offshore Brazil, development progress in the Tishomingo Field in Oklahoma and a partnership that will deploy advanced electric simul-frac fleets across the Permian Basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.