[Editor's note: A version of this story appears in the February 2020 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Alaska, the giant oven mitt-shaped state of ice, fortitude and darkness, is not known for its heat waves—the average temperature in 2019 was a freezing 32.2 degrees. But that doesn’t mean the state never burns anyone.

The summer of 2019, while still not swimming weather, saw Alaska record its hottest July, averaging 58.1 degrees, about 5.4 degrees above normal, according to federal data. Scientists also published papers suggesting Alaskan glaciers were melting at a rate 100 times greater than previously thought.

The oil and gas industry, a central pillar of the state’s economy, faced its own scorcher. Some voters in the “Land of the Midnight Sun” began agitating to raise taxes on Alaska’s largest oil producing fields—even as the state finds itself hundreds of millions of dollars in arrears to E&Ps. Alaska lease sales and exploration have been up and down. And like its cousins in the continental U.S., consolidation is rising with recent deals concentrating 72% of production in the hands of just two companies: ConocoPhillips Co. and Hilcorp Energy Co.

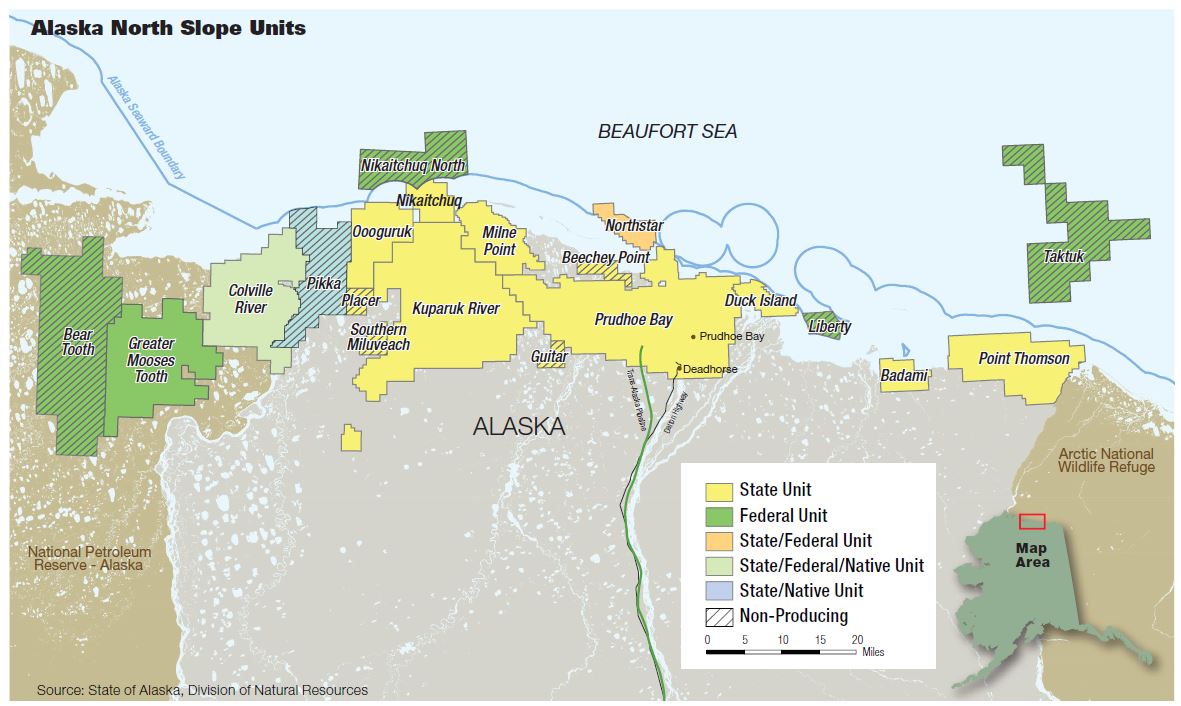

Among those burned by Alaska is Jim Musselman, who still has not made peace with dueling emotions—awe and anger—that the state evokes. In two deals struck in January and June, Musselman’s Caelus Natural Resources sold interests in Oooguruk Field to Italian major Eni S.p.A and its 21,000-acre Nuna discovery to ConocoPhillips for undisclosed sums.

“I’m fascinated by Alaska,” Musselman told Investor. “We got treated very poorly up there, unfortunately, which is too bad because we put together a really nice company.”

Caelus was among several companies that had taken up on an offer by Alaska to find oil in the frontier areas outside of the state’s large legacy fields as Alaska sought to turn around its sagging production. In exchange, E&Ps were to receive tax credits for their wells. But after oil prices tanked in 2015, the state was unable to make good on promised payments. Musselman said Caelus is still owed about $160 million.

“We had good assets, but we just could not get any capital to go up there because the state had this tax credit scheme that really jumped us,” he said. “And then they just ghosted. They said, ‘We will pay you, but we can’t pay you now because we’re broke.’ And it was a true statement. They were broke at the time.”

Yet Musselman, who serves as chairman of blank-check company Alussa Energy Acquisition Corp., which closed a $287 million IPO in November, said the public company might consider acquiring assets in Alaska.

“Absolutely. We’ve depicted our search as an international search, but I’ve always kind of dinged Alaska as international,” he said. “It’s certainly different than the Lower 48 states in many respects.”

Alaska operators generally grapple with the same dilemmas as the industry writ large: money, politics and consolidation. Musselman found his private-equity partners unwilling to commit more money to his project.

Some of Alaska’s financial woes are coming from the inside out.

“We do have this looming, potential ballot initiative hanging over our heads” that would raise severance taxes, Kara Moriarty, president and CEO of the Alaska Oil and Gas Association told Investor. “We’ve got everything in place to have a strong energy sector for the next decade. As long as the fiscal stability regime remains” in place.

Like other oil producing states, most prominently Colorado, Alaska faced environmental ballot measures. Voters defeated a 2018 initiative that would have established new permitting rules for areas near waters used by salmon, steelhead or other fish that swim upstream from the ocean to spawn.

But a group of Alaskans want to increase taxes on production companies through an initiative called the Fair Share Act. The measure is so far not on the ballot.

Alaska does not allow the voters to amend its constitution through initiatives. However, voters may submit legislation to introduce and enact as law.

Fair Share supporters say the state is “giving away” up to $2 billion annual in tax breaks for large and profitable legacy fields. In 2015, Alaska spent more per capita on any other state and, at nearly $20,000, twice the national average, according to the Texas Policy Center. In 2019, Alaska residents’ annual state dividend was $1,606, according to the Alaska Permanent Fund.

Habitual fights over how to tax oil and gas companies have given Alaska a name for being fiscally fickle, Moriarty said.

“We just have this reputation that we like to change taxes on a constant basis,” she said. In the past 14 years, the fiscal regime has been tweaked or changed substantially seven to eight times, she said.

“We’ve got yet another situation,” she said. “That is the challenge. Are we truly a stable fiscal environment? And in this fiscal environment, companies are, under our current system, investing billions of dollars in the state.”

Executives at ConocoPhillips, which plans to invest $25 billion in 10 years in Alaska and about as much again on operations, fired a not-so-subtle shot across the bow of the proposal.

ConocoPhillips COO Matt Fox said during a November analyst and investor meeting that if the measure makes it on the 2020 ballot, Alaskans will understand “the lifeblood of the state’s economy” is at stake.

“Our sense is that once the dust has settled, then everybody understands what’s at stake. Alaskans will understand that short-term revenue gain is a risky proposition if you’re going to give up all this long-term potential,” he said. “Because our investment plans would need to change if there was a change in the fiscal regime.”

Beating the slump

Musselman and his exploration team were enthralled by Alaska after he founded Caelus in 2011.

“My explorers have been all over the world, but after our initial look up there we thought, ‘Man, this is the oiliest place in the world.’ And that’s still the case,” he said. “But it’s expensive and it’s difficult and it’s a harsh environment.”

By 2017, the company had invested $2.2 billion in the state. The heartbreak awaiting Caelus was that after discovering 150 million barrels (bbl) of proved and probable reserves it could not get money to drill it.

“The geology and the availability of good rocks were high with the difficulty of getting it out was maybe a little higher,” he said.

Despite efforts to encourage exploration and investment, Alaska production continues to flag. Since peaking in 1988, oil production has fallen 76%, according to U.S. Energy Information Administration (EIA) data. From 2000 to 2018, Alaska oil production slumped by an average of nearly 495,000 barrels per day (bbl/d).

Alaska is often described in terms of its length and breadth. The state could squeeze in Texas, California and Montana within its borders with enough room left over for an Idaho-sized parking lot.

But the size and scale of “The Last Frontier” masks its continuing fight to turn back its dwindling production, which has largely seen limited success.

Among oil producing states, Alaska was sixth in 2018—toward the back of a middling pack that includes New Mexico, Oklahoma, Colorado and California. Put another way, in 2018, Texas pumped enough crude to match Alaska’s total annual oil output roughly every 39 days.

For smaller, independent companies, the barriers of entry are sometimes hard to surmount, said Edward Hirs, an energy economist and a BDO Natural Resources fellow.

Because of the capital, equipment and manpower necessary to explore, drill, produce and transport oil and gas, costs tend to be overwhelming for E&Ps.

“Alaska is not overrun by independents,” Hirs said. “It’s a big boy’s game.”

While the Lower 48 offers a chance for a team of “five guys and $100 million” to lease acreage in the Permian Basin, “Alaska is just different,” he said.

Without permanent infrastructure to transport equipment and supplies, Alaska operators often build ice roads to drilling locations. The roads alone cost between $300,000 and $400,000 per mile, according to a Bureau of Land Management (BLM) report. When temperatures or snowfall are inadequate, operators may use gravel roads that cost up to $1 million per mile to construct. Even if an ice road was built once every three years, costs to construct it would exceed building a permanent road within nine years, according to BLM’s report.

In 2018, ConocoPhillips reported building about 140 miles of ice roads and 161 acres of ice pads to support the second season of exploration in the Greater Mooses Tooth Unit.

Costs to operate in Alaska are so expensive that development is more akin to deepwater projects, with returns expected years out. ConocoPhillips uses megaproject vernacular for its operations there, describing its plans for Nuna Field in 2019 as awaiting a “financial investment decision.”

With seismic data shot across Alaska, producers have a good idea of where hydrocarbons are and access to markets in California, Japan or China. Alaska North Slope crude also trades at a premium to West Texas Intermediate.

“If you’re successful with your exploratory well, then development becomes a very profitable enterprise,” Hirs said.

To address those hurdles, in 2013, Alaska took action to lure in smaller, exploration-oriented companies with a tax credit for exploration outside the state’s major legacy fields. The credit ultimately backfired as oil prices swooned. By 2018, the state owed producers roughly $1 billion, according to analytics company GlobalData.

The legality of a potential bond issuance to pay companies is before Alaska’s Supreme Court. If the state receives a favorable ruling, the Alaska Revenue Department said it would appropriate $700 million to pay explorers.

Musselman, one of the five founders of deepwater company Kosmos Energy, is no stranger to risk. But his experience with the state and Caelus-backer Apollo Global Management LLC may serve as a cautionary tale for would-be explorers in Alaska.

Still convinced of Alaska’s opportunities, Musselman continues to work with a company in Alaska on Caelus’ former leasehold. But he’s not sure smaller, private-equity-backed companies are eager to embrace the state.

“As far as creating a company like Caelus, [like we] did with Apollo, starting from scratch there and buying the assets, I think that’s pretty hard to do,” he said. “And some of that is probably because of our experience. I think people were forewarned by our experience just [of] the state not being terribly welcoming.”

In early December, Michael A. Barnhill, the acting commissioner for the Alaska Department of Revenue, projected further declines in oil production in 2020 and 2021.

“New fields offer tremendous potential to increase production later in the 2020s, but these developments are still contingent on final investment decisions and commitment of billions of dollars of new investments on the part of oil and gas producers,” Barnhill said in a letter to the governor.

West of North Slope

In February, the Nordic-Calista No. 3 rig, winterized to operate in arctic climes, sent plumes of exhaust white as snow into the night sky.

Like other pioneers in Alaska, Australian company 88 Energy Ltd. is pushing out into new territory. The company is targeting horizontal drilling on 225,000 net acres in an area dubbed Icewine. It began the New Year embarking on a campaign that first involves a 30-mile ice road to the south of the community of Deadhorse, about 5 miles inland from the Beaufort Sea in Prudhoe Bay.

The company planned to begin construction of the ice road in January as it makes its way to the drillsite for the Charlie-1 appraisal well, which is expected to be drilled in February. It’s taken roughly four years for 88 Energy to get to this point, after the company first acquired 2-D seismic in 2016, followed by 3-D seismic in 2018.

“Alaska, the North Slope in particular, has been experiencing a renaissance over the past 10 years, which seems to be accelerating,” David Wall, managing director of 88 Energy, told Investor.

That renaissance is largely focused on discovery. In 2019, the state enjoyed one of its best exploration seasons in decades. This year, ConocoPhillips is launching its largest-ever exploration and appraisal program, with four wells planned for prospects in its Willow discovery in the Bear Tooth Unit in addition to three exploration wells in the Harpoon prospect. The company plans to invest about $25 billion in Alaska over the next decade.

“On the exploration front for Alaska, 2019 was one of the busiest exploration seasons we’ve had in almost 20 years, and 2020 is shaping up to be another really strong exploration year for Alaska,” Moriarty said.

Hilcorp, Eni and Oil Search are planning projects and investments totaling billions that could generate several hundred thousand barrels of oil per day, Moriarty said.

Wall also noted several deals that have transacted. Among the more jarring M&A in 2019, BP Plc ended six decades of operations in the North Slope, after selling its operations, pipelines and other assets to Hilcorp for $5.6 billion. ConocoPhillips also plans to sell a 25% farm-down of its working interests.

Wood Mackenzie analyst Rowena Gunn said in August that the BP deals stood out, in particular, for the importance of BP’s 48% interest in the Trans-Alaska Pipeline.

“Growth is coming westward from ConocoPhillips and Oil Search-operated projects. But all North Slope barrels rely on the infrastructure established at Prudhoe Bay,” Gunn said, adding “this will not be the last deal in the region. ExxonMobil [Corp.] may be next to follow BP, Anadarko [Petroleum Corp.], Pioneer [Natural Resources Co.] and Marathon [Oil Corp.] in the list of companies having sold out of Alaska.”

Wall said such deals were made on “the back of over 4 billion barrels of oil discovered on the Slope in the past six years.”

He also noted substantial participation in lease sales as well as seismic acquisition and drilling activity—exploration, appraisal and development. Lease sales have been hit or miss in Alaska. In May 2019, about 10 million net acres offered by the state drew only three bids. A BLM lease sale fared better, with 92 bids, although by only three companies. “There is a lot going on,” he said.

Wall said the state’s production estimates are appropriately conservative, which “has not always been the case, historically.” Further exploration should help reverse the production declines in Alaska, he said.

Projects in Pikka and Willow to drill discoveries should add 200,000 bbl/d of oil by 2024 or 2025, he said. In 2017, Spain’s Repsol SA and partner Armstrong Energy announced what they called the largest U.S. onshore oil discovery in 30 years with a 1.2 Bbbl find in Alaska’s North Slope.

“Production at Prudhoe has also plateaued in recent years, and the decline forecast of circa 50,000 barrels per day over the next four years will be more than offset by the new production,” Wall said, adding that will be upscaled over time as more oil is discovered or commercialized. “Including by us, hopefully,” he said.

ConocoPhillips’ exploration efforts, by necessity, will be far more widespread than anything undertaken in the Lower 48.

While shale producers routinely drill 5,000-foot laterals—and Basic Energy Services Inc. and Surge Energy Inc. drilled a record 17,935-foot horizontal well in New Mexico in July 2019—wells in Alaska tend to be an order of magnitude longer.

ConocoPhillips has drilled the 10 longest wells in Alaska, with the longest at 32,000 feet, Michael Hatfield, president of ConocoPhillips’ Alaska, Canada and Europe operations, told analysts in December. But it is gearing up to reach out even farther.

“We expect to push the records even further because next year we’ll take delivery of a newbuild extended reach drilling rig [ERD],” he said.

The ERD rig will be capable of drilling more than 7 miles from a pad site, he said, and has three times the subsurface coverage of existing rigs. The rig’s reach is so great that if centered in Lower Manhattan, it could reach “the other four boroughs covering an area greater than 150 square miles.”

Despite a provision of the 2017 tax law signed by President Donald Trump opening the Arctic National Wildlife Refuge to exploration, Musselman said prospecting continues to push out from North America’s second largest oil field, Kuparuk, 40 miles west of Prudhoe Bay. He said little science has been down east of Prudhoe Bay, and there’s generally more interest in following the path of Armstrong and Oil Search.

“Those developments extend the frontier by another 8 or 10 or 20 miles to the west,” he said. “I think there’s going to be a stepping out to the West and in Alaska and the North Slope.”

Recommended Reading

Elliott Nominates 7 Directors for Phillips 66 Board in Big Push for Restructuring

2025-03-04 - Elliott Investment Management, which has taken a $2.5 billion stake in Phillips 66, said the nominated directors will bolster accountability and improve oversight of Phillips’ management initiatives.

Activist Elliott Builds Stake in Oil Major BP, Source Says

2025-02-10 - U.S.-based Elliott is seeking to boost shareholder value by urging BP to consider transformative measures, Bloomberg News reported Feb. 8.

EON Deal Adds Permian Interests, Restructures Balance Sheet

2025-02-11 - EON Resources Inc. will acquire Permian overriding royalty interests in a cash-and-equity deal with Pogo Royalty LLC, which has agreed to reduce certain liabilities and obligations owed to it by EON.

Italy's Intesa Sanpaolo Adds to List of Banks Shunning Papua LNG Project

2025-02-13 - Italy's largest banking group, Intesa Sanpaolo, is the latest in a list of banks unwilling to finance a $10 billion LNG project in Papua New Guinea being developed by France's TotalEnergies, Australia's Santos and the U.S.' Exxon Mobil.

Equinor Commences First Tranche of $5B Share Buyback

2025-02-07 - Equinor began the first tranche of a share repurchase of up to $5 billion.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.