With Ovintiv Inc. scooping up three EnCap-backed drillers in the Permian, public E&Ps have fewer places to look to add quality inventory runway. (Source: Shutterstock)

After Ovintiv’s $4.275 billion acquisition in the Permian Basin, opportunities for attractive, inventory-rich M&A in the Lower 48’s premier shale play are shrinking, analysts say.

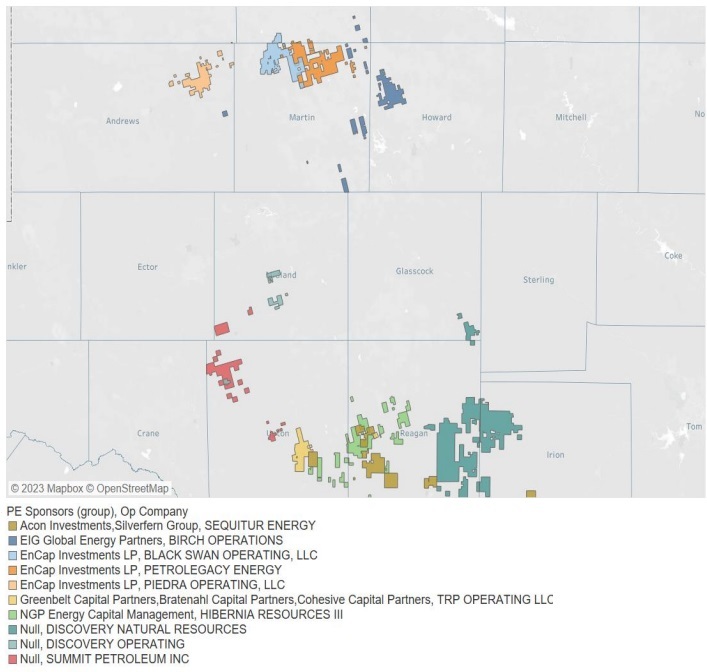

Ovintiv Inc. agreed to scoop up three EnCap-backed privates – Black Swan Oil & Gas, PetroLegacy Energy and Piedra Resources – in the Northern Midland Basin in a cash-and-stock deal valued at $4.725 billion, the companies announced April 3.

After first-quarter oil and gas deal activity rivaled COVID-19 lows, Ovintiv’s acquisition kicked off a strong start to M&A in the second quarter, analysts at Piper Sandler & Co. wrote in an April 4 report. The firm’s detailed analysis of private Permian Basin E&Ps — including Hibernia Resources and Summit Petroleum — shows several middling operators remain on the outskirts of the core.

As Ovintiv President and CEO Brendan McCracken alluded to in an April 3 call with analysts, attractive core inventory in the Permian Basin is becoming harder to find.

“With shale hitting the middle innings, the asset we are acquiring is a rarity,” McCracken said.

Amid the mad dash to add inventory, many of the larger public oil and gas companies, including Ovintiv, Matador Resources and Diamondback Energy, have signed big deals with private E&Ps in the Permian in the last year.

Outside of the Permian, Marathon Oil Corp. completed a $3 billion acquisition deal of Ensign Natural Resources’ Eagle Ford assets in December 2022. Gassier plays such as the Haynesville Shale have more runway than deals have in 2023 as prices remain depressed.

In fact, more than $30 billion worth of private companies and assets were sold to public E&Ps in 2022 — accounting for about 60% of total upstream M&A activity last year, according to data from Enverus.

But analysts say opportunities to roll up higher-quality private operators with attractive core inventory are dwindling.

“There’s just not that many big, strategic deals out there to be had if you look at the remaining private or private equity companies in the core of these basins that might sell,” Enverus Intelligence Research Director Andrew Dittmar told Hart Energy. “There’s lots of public companies out there that still need inventory, so we think it’s a competitive market.”

RELATED

Ovintiv’s $4.2 Billion Permian Deal Improves Inventory Runway, Crude Output

Hunting for inventory

Black Swan, PetroLegacy and Piedra’s assets in the northern edges of the Northern Midland Basin represented some of the highest-quality private-equity backed opportunities in the area, Dittmar said.

“We have about an average $44 breakeven pricing on the inventory that …[Ovinitiv’s] picking up, which slots into a very competitive set,” Dittmar said.

With the three EnCap portfolio companies off the table, there are fewer quality opportunities for M&A to choose from. Public E&Ps will likely need to push further into the edges of the Midland and Delaware to find inventory deals, he said.

“That’s just the nature of what opportunities are available in the market right now,” Dittmar said. “The center, core-of-the-core portions of the basin have really been picked over, and even the good assets that are available are probably going to be a step out toward one of the margins.”

High decline rates and the limited inventory held by private E&Ps in the basin pose challenges to public companies looking to add high-quality inventory, according to Piper Sandler.

“The core of both the Delaware and the Midland has basically been captured,” Mark Lear, senior research analyst at Piper Sandler and one of the note’s authors, told Hart Energy. “I think what we’re really playing for is maybe smaller bolt-on opportunities in the core.”

Out of 10 private E&Ps operating in the Midland Basin analyzed by Piper Sandler, the three companies Ovintiv is acquiring each showed strong productivity and sizable acreage positions. Together, they have a larger base of proved developed producing (PDP) reserves and acreage than most of the private E&Ps analyzed.

Though there is a shrinking number of top-tier M&A opportunities in the Permian, there are still some standout private companies operating in the Midland and Delaware, according to Piper Sandler data.

One is Birch Operations, which was the most productive private operator analyzed in the Midland despite owning a relatively smaller acreage position of about 40,000 acres.

Summit Petroleum and Hibernia Resources III also boast large, contiguous acreage positions in the Midland. But they’ve also shown signs of asset degradation recently, with Summit shifting activity in Texas from Midland County to Upton County. Hibernia has shifted from Upton to Reagan County, according to Piper Sandler.

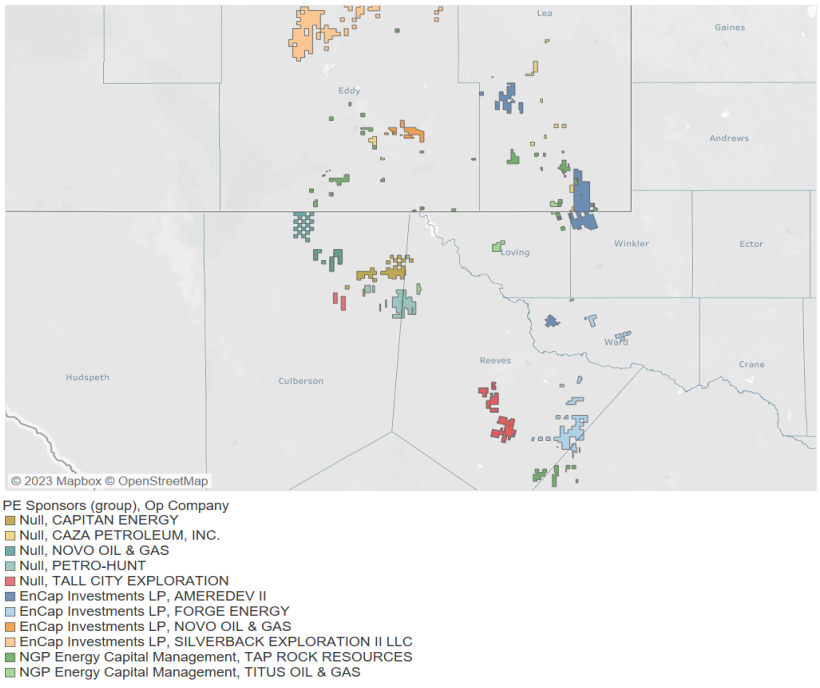

Private operators also generally own more fringe positions and less core acreage in the Delaware Basin after years of industry consolidation.

Tap Rock Resources, backed by private equity firm NGP Energy Capital, has acreage in core Lea County, New Mexico, Piper Sandler noted.

Ameredev II, another EnCap-backed E&P, also has attractive blocky core acreage and a flat production profile across its Delaware position.

Larger private producers in the Permian that are unlikely to be sellers, including Mewbourne Oil Co., Endeavor Energy Resources and CrownQuest Operating, were not analyzed.

RELATED

Public, Private E&Ps Split on Permian Basin Drilling Strategies

Haynesville M&A opportunities

Oil deals might be getting more scarce in the core, but there are abundant opportunities for deals with private E&Ps in the gassy Haynesville Shale, Lear said.

Haynesville operators, including Aethon Energy, GEP Haynesville II, Rockcliff Energy and Paloma Resources, have amassed sizeable inventories and scaled gas production in the basin in recent years, Piper Sandler said.

But gas-focused M&A activity has been effectively shut down in 2023 after U.S. natural gas prices plunged more than 50% compared to 2022.

Henry Hub natural gas prices are expected to average around $3 per million Btu (MMBtu) this year after averaging $6.42/MMBtu in 2022, according to U.S. Energy Information Administration (EIA) data. Henry Hub prices topped $9/MMBtu last summer, according to the EIA.

Natural gas futures for delivery in May were trading up over 1% at $2.13/MMBtu in afternoon trading on April 5.

TG Natural Resources, a unit of Tokyo Gas, was advancing discussions earlier this year to acquire Rockcliff in a deal worth $4.6 billion. But that deal reportedly fell apart due to weak gas pricing making deals more challenging, Piper Sandler said.

The only announced gas deal of much consequence last quarter was Diversified Energy Co.’s acquisition of Texas upstream assets from Tanos Energy Holdings II LLC for $250 million, according to Enverus data.

“I do think that there’s a prevalent view that gas is still pretty abundant and easy to get – maybe not at $2, but certainly in that $3 to $4 ballpark,” Lear said. “I think that’s where a lot of things come into play.”

RELATED

Oil, Gas Price Volatility Slows Upstream M&A Market

Recommended Reading

Ovintiv Closes Montney Acquisition, Completing $4.3B in M&A

2025-02-02 - Ovintiv closed its $2.3 billion acquisition of Paramount Resource’s Montney Shale assets on Jan. 31 after divesting Unita Basin assets for $2 billion last week.

Coterra Energy Closes Pair of Permian Basin Deals for $3.9B

2025-01-28 - Coterra Energy Inc. purchased Delaware Basin assets from Franklin Mountain Energy and Avant Natural Resources for $3.9 billion.

CNX Expands in Appalachia with Closing of $505MM Apex Deal

2025-01-27 - The bolt-on of Apex Energy II's upstream and midstream assets expands CNX’s stacked Marcellus and Utica undeveloped leaseholds.

New Era Helium Signs NatGas Deal to Supply Permian Data Center Campus

2025-03-02 - The AI data center project will be developed on 200 acres of land the Texas Critical Data Centers joint venture will be acquiring. The project is expected to be online by the end of 2026.

NAPE Panelist: Occidental Shops ~$1B in D-J Basin Minerals Sale

2025-02-05 - Occidental Petroleum is marketing a minerals package in Colorado’s Denver-Julesburg Basin valued at up to $1 billion, according to a panelist at the 2025 NAPE conference.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.