The Dallas Fed’s first quarter survey of oil and gas executives reveals concerns over inflation, growth and future uncertainty. (Source: Tallmaple/Shutterstock.com)

Growth has stalled, production is sluggish, costs are up and oil and gas executives are grumpy, the Federal Reserve Bank of Dallas reported in its first-quarter energy survey on March 29.

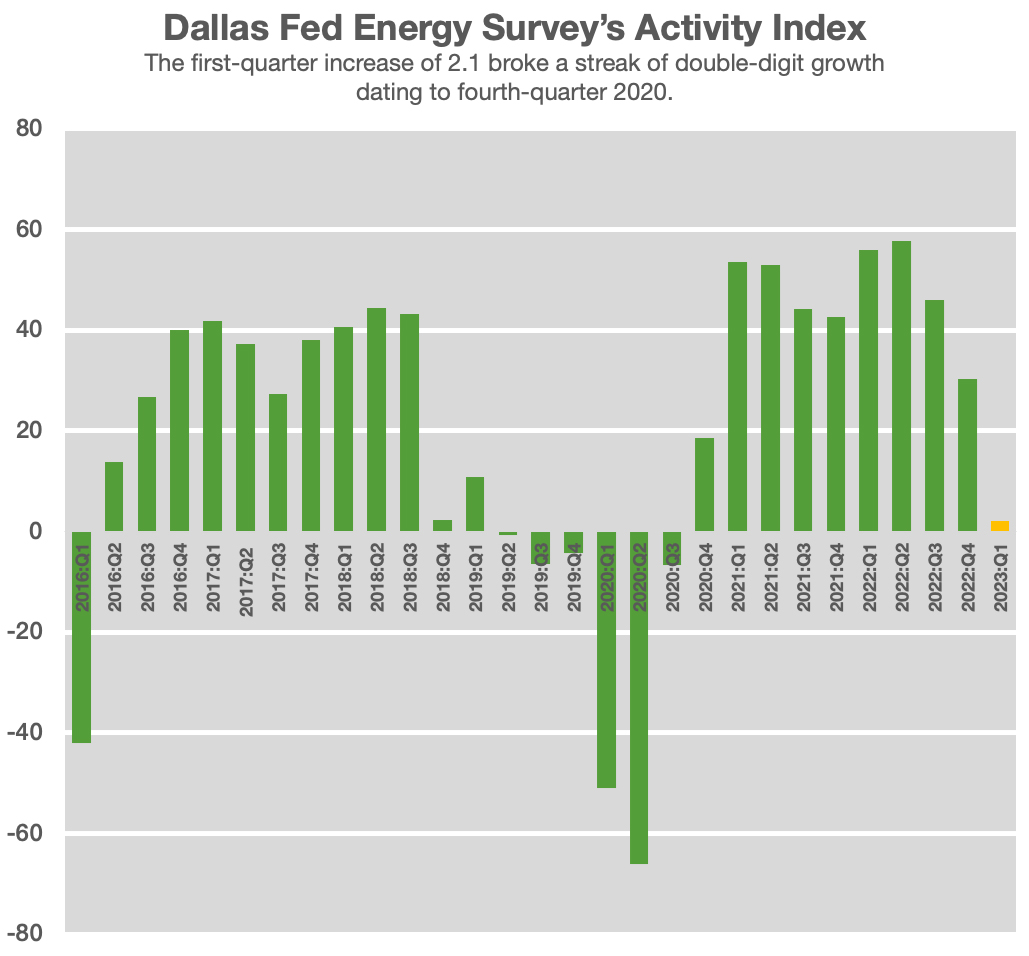

The business activity index plunged to 2.1 in the quarter from 30.3 in fourth-quarter 2022, indicating that activity grew little in the first three months of the year. For more than two years, activity had been on the rise in double-digits, and the drop, based on responses from energy executives, is due to the cloud of uncertainty hanging over the industry. The index is the survey’s broadest measure of conditions facing energy firms in Texas, northern Louisiana and southern New Mexico.

Inflation and the health of the global economy will have the most influence on profitability this year, executives at 136 oil and gas companies said in response to the Dallas Fed’s survey earlier this month. Access to and the cost of capital, government regulations and supply chain issues ranked further down the list.

Comments by executives reflected uncertainty colored by dread:

- “It is extremely difficult to plan for the future with so much of the base data we are used to using being all over the board. Seems like business patterns go against trends proven over the last 30-40 years in the oil and gas industry as a whole and the oil and gas service business specifically.”

- “Outside investors seem to be losing interest in hydrocarbons. The worldwide macroeconomic and political outlook is cloudy. The road ahead looks difficult but passable. We expect another ‘muddle through’ period in a cyclical business where more players will be winnowed out.”

- “Oilfield inflation has to be the No. 1 problem. Capital expenditure increases are soaring well past consumer price index data. I’m noticing apparent quality problems beginning to plague new projects; specifically, I’ve never seen so many cases of parted tubing with new tubing, particularly with poor quality collars, as I’m seeing in recent months.”

Price Outlook

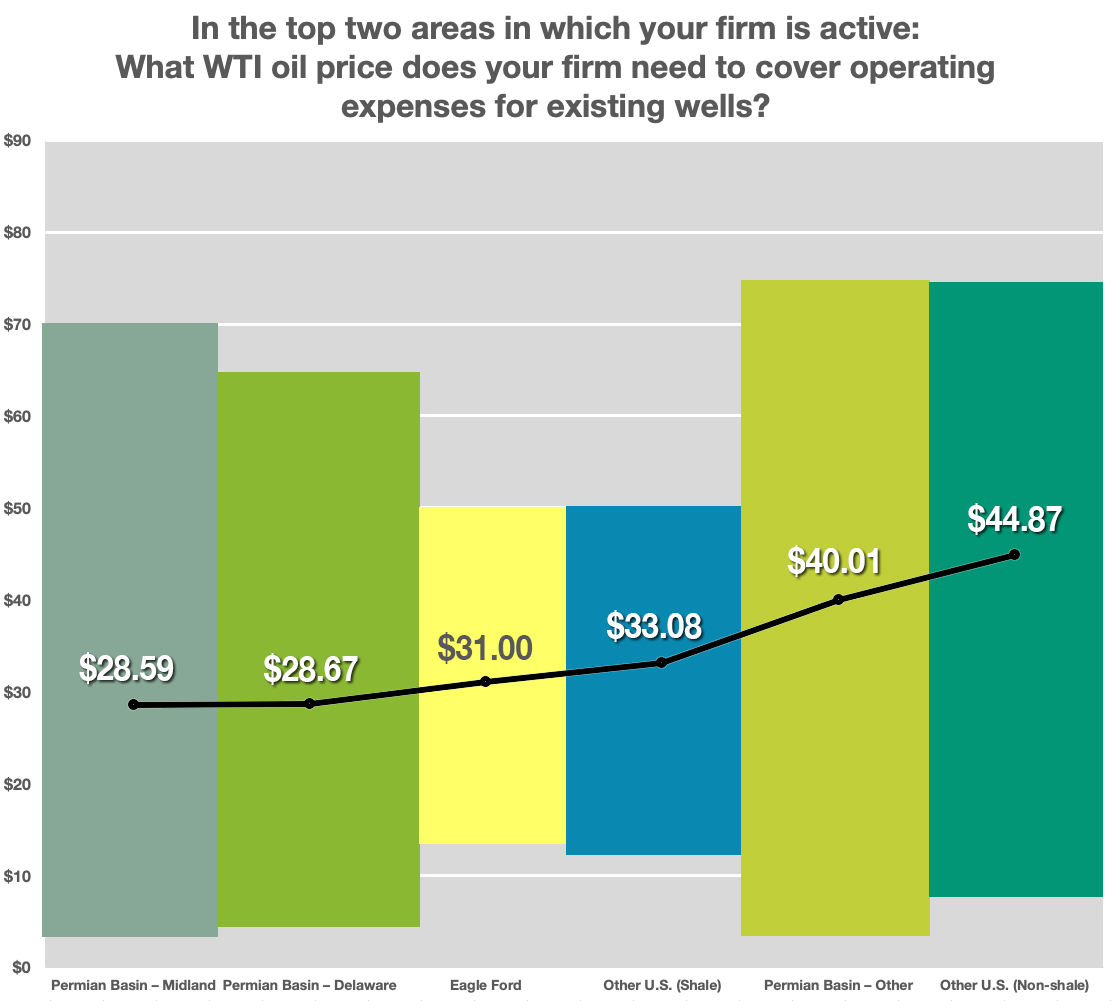

Across the regions where the surveyed companies operate, the average WTI price needed to cover operating expenses for existing wells ranging from a low of $29/bbl in the Midland Basin to $45/bbl in U.S. non-shale areas. The average price of $37/bbl was up from $34/bbl in 2022.

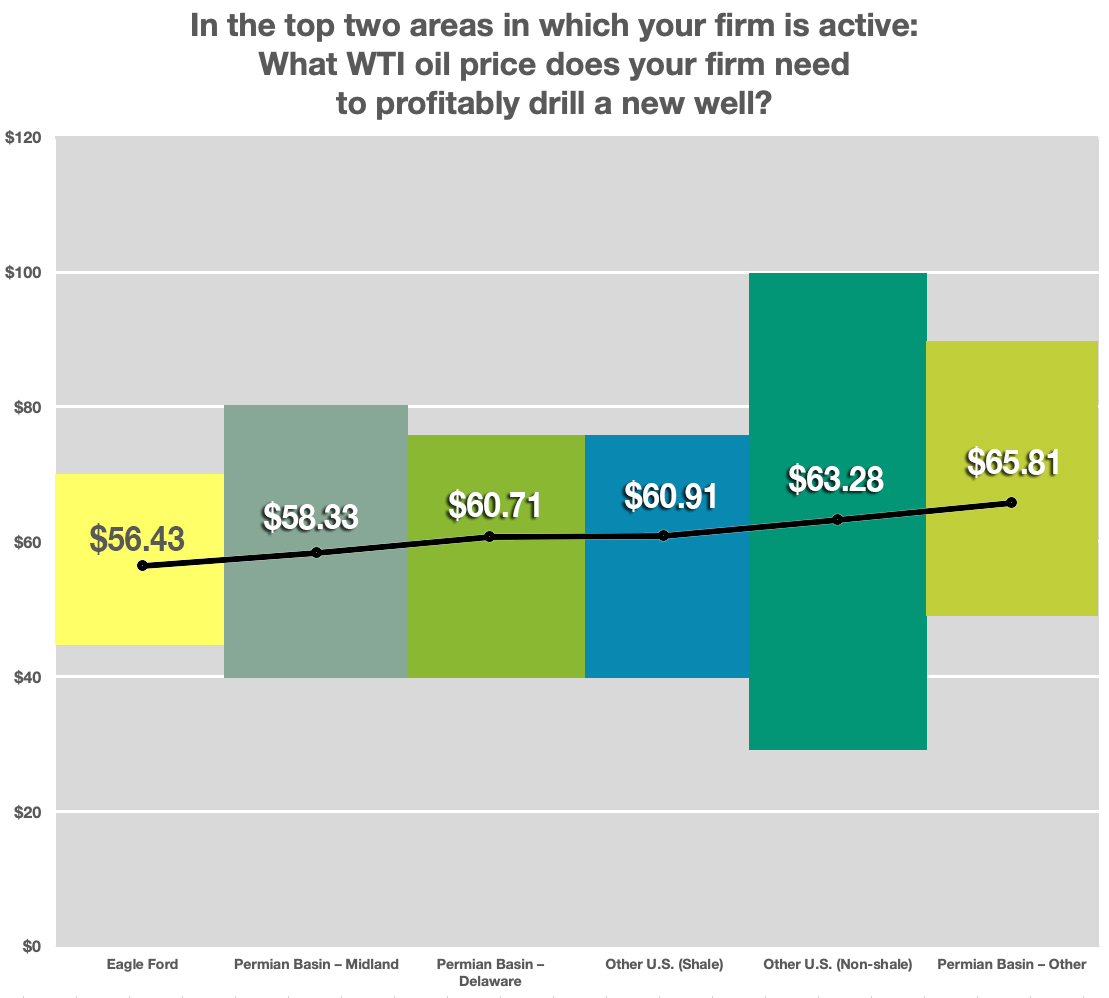

The price of WTI needs to be $62/bbl, on average, to warrant drilling a new well, executives who were surveyed said. That price is above the $56/bbl average of last year. Average breakeven prices across the regions in the Permian Basin and Eagle Ford and elsewhere range from $56/bbl to $66/bbl. In the Permian Basin, the $61/bbl average is $9/bbl higher than last year.

Size does matter when it comes to breakeven pricing. For large firms that produce 10,000 bbl/d or more, the average is about $55/bbl across all regions. Smaller companies require a WTI average price of $64.

Comments from executives on pricing:

- “Oil price correction is adding pressure on the continuation of drilling and frac activities. [We] expect the activity level to be flat to down in 2023 versus 2022’s exit.”

- “Service costs and authorization for expenditures keep climbing. The latest commodity price action feels like the sword of Damocles is back; where is oil going to bottom this time?”

- “Overall, prices have impacted the revenue but not yet costs. We are still waiting for costs to catch up with the new pricing levels. We do not expect prices to increase significantly.”

Recommended Reading

Chevron Targets Up to $8B in Free Cash Flow Growth Next Year, CEO Says

2025-01-08 - The No. 2 U.S. oil producer expects results to benefit from the start of new or expanded oil production projects in Kazakhstan, U.S. shale and the offshore U.S. Gulf of Mexico.

Chevron Technology Ventures Would Like to See the Manager

2025-03-13 - Chevron Corp.’s Chevron Technology Ventures, which turns 25 this year, pays close attention to leadership teams when making investment decisions in technology startups.

Chevron to Lay Off 15% to 20% of Global Workforce

2025-02-12 - At the end of 2023, Chevron employed 40,212 people across its operations. A layoff of 20% of total employees would be about 8,000 people.

Expand Energy Picked to Join S&P 500

2025-03-10 - Gas pureplay Expand Energy will be elevated on March 24 from its position in the S&P MidCap 400 index.

Chevron Makes Leadership, Organizational Changes in Bid to Simplify

2025-02-24 - Chevron Corp. is consolidating its oil, products and gas organization into two segments: upstream and downstream, midstream and chemicals.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.