MPLX LP’s Garyville, La., products system moves refined products 70 miles from Marathon Petroleum’s refinery in Garyville through this 20-inch pipeline to either Plantation Pipeline in Baton Rouge, La., or Marathon Petroleum’s Zachary, La., tank farm. Capacity is 389,000 barrels per day. All photos courtesy of MPLX LP

Midstream’s “thanks, guys, we’ll take it from here” phase has begun and muscled MLPs like MPLX LP are poised to step up.

“I expect that the entire MLP space is going to be in a consolidation mode going forward,” Gary Heminger, chairman of the board and CEO of the Findlay, Ohio-based company MPLX LP, told Midstream Business. “You just look at the entire industry and the amount that is required in order to grow in the MLP space. We estimate somewhere between $22 billion and $25 billion a year of projects to satisfy growth if you assume an 8% to 10% composite growth rate for the industry.”

The challenge, he said, will be to identify those big projects and develop the capability to complete them in ways that satisfy customers and investors while growing the industry. Few midstream players have a $26 billion corporate sponsor like Marathon Petroleum Corp. (MPC) that positions them to do that.

“That’s why I say that we think this market is going to change to be a very large consolidation market,” Heminger said, “and that’s why I think it gives us a certain discreet competitive advantage.”

Growth from the start

Heminger and his management team launched MPLX in 2012 with the intention of creating a top-quartile growth company. Since the initial filing, the sponsor, MPC, has commenced several organic growth projects, including:

- A joint venture with Enbridge Energy Partners LP to develop the Sandpiper Project, a crude oil pipeline extension to link Beaver Lodge, N.D., to Superior, Wis.;

- A separate joint venture with Enbridge (Southern Access Extension Pipeline) to deliver Canadian and Bakken crude to the Patoka, Ill., pipeline hub; and

- Construction of two condensate splitters at two of its refineries, one with 25,000 barrel-per-day (Mbbl/d) capacity in Canton, Ohio, and the other with 35 Mbbl/d in Catlettsburg, Ky.

“At that time, the definition of top quartile was growth somewhere between 15% and 18%, and that was considered to be very strong growth for a while,” Heminger said.

But a funny thing happened since the filing—18% growth was no longer enough.

“In order to be a top-quartile MLP, the bar had been lifted to a minimum of about 20%,” he said. “So over the last year, we’ve embarked on a very detailed analysis, working with our board, on a number of different scenarios and concepts on how we see MPLX.”

Growing quickly

The result is a no-holds-barred leap into the future.

“We’ve announced plans to substantially increase the pace of growth of the partnership to build size and scale more rapidly,” MPLX President Pamela Beall told analysts during the company’s third-quarter earnings call. “As part of this growth, we expect to provide an average annual distribution growth rate in the mid-20% range over the next five years.”

Long story short: “We now have a backlog of $1.7 billion of EBITDA including growth projects that we think should grow the value of MPLX to somewhere between $17 billion and $20 billion,” said Heminger. “So if I take that $1.7 billion on top of what we’ve already accomplished, we should be somewhere around a $20 billion market cap for our MLP as we go forward.”

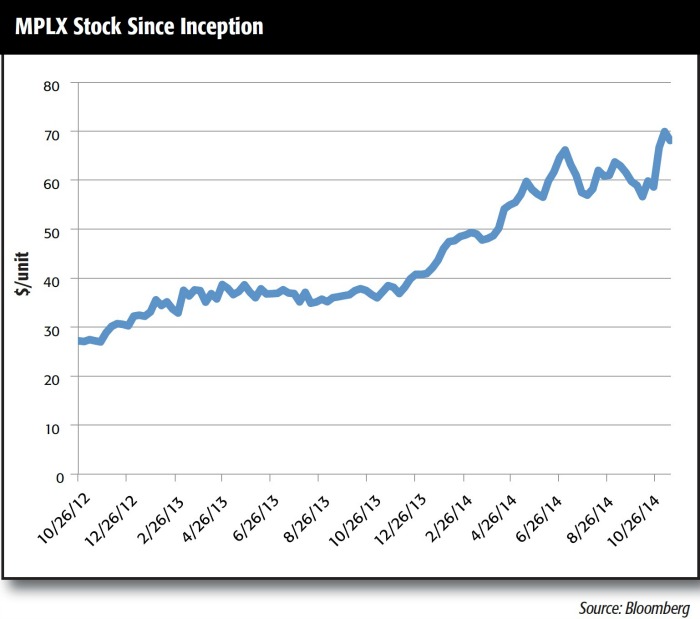

That’s the company’s five-year guidance to investors. At the close of third-quarter 2014, MPLX posted a market capitalization of around $5.1 billion, more than double the $2.4 billion it was worth at the end of 2012. The plan is to go with what it’s got and then grow from there.

Beall attributed the tremendous potential for growth in the midstream for instigating the accelerated growth program.

“Certainly one of the significant contributors to that decision is the substantial growth in the domestic oil and gas production and the tremendous buildout that we see for the midstream assets in the U.S.,” she said. There are “many opportunities where really size and scale become strategically important in midstream growth for a vehicle like MPLX, and it’s fully our intent to participate in that development.”

Another factor, closer to home, was the perception that investors were not giving the entire MPC enterprise its due.

“By accelerating the growth of these highly valued portions of the business, between MPLX now and Speedway [an MPC-owned retail business], we believe that will highlight the tremendous value that really exists in the business, that’s being missed in MPC’s valuation today,” Beall said. “So growing the MLP, MPLX, will position us well to participate in larger opportunities directly.”

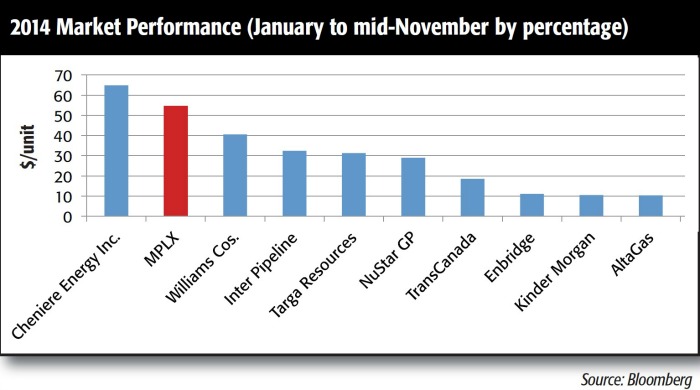

MPC’s stock, from January through mid-November 2014, had increased in value by less than 1%.

Organic potential

Cornerstone Pipeline is an example of the MPLX strategy. Part of the Utica buildout, the 50-mile proposed pipeline will move condensate from Harrison County, Ohio, to MPC’s refinery in Canton, Ohio, when it is completed in 2016. Its route will take it past several Utica Shale condensate and fractionation facilities.

“This pipeline, along with associated buildout projects are designed not only to feed MPC’s condensate splitter at its Ohio refinery, they’re designed to meet the needs of producers, other refiners, as well as processors and marketers of a variety of natural gas liquids,” Beall said. “These investments will allow our sponsor to leverage growing Utica production in eastern Ohio and position MPLX to participate directly in the development of the needed infrastructure.”

If the business grows, so will the pipeline.

“Phase two, if the Utica production region continues to grow, would be to consider taking some of these condensates and crude and going west back to the Lima and Toledo, Ohio, refining complexes,” Heminger said.

Aside from Cornerstone, MPLX is exploring the possibility of delivering natural gas liquids to the Chicago area and to pipelines that supply diluents to western Canada.

Theory of evolution

In the short term, management aims to almost triple annualized EBITDA to $450 million as of December 2015, compared to the current $160 million annualized EBITDA, based on third-quarter 2014. It plans to evaluate the acquisition of the remaining 31% interest in MPLX Pipe Line Holdings, which would add about $80 million of EBITDA. Net earnings were $146 million for 2013; $172 million for third-quarter annualized 2014 and are expected to reach $212 million for 2015 per analyst consensus estimates.

The story line is the evolution of MPLX into a large-cap, diversified logistics MLP.

Investors eagerly await the next chapter. By mid-November, MPLX’s stock growth of 54.6% had outperformed all of its competitors in the midstream space for the year with the exception of high-flying Cheniere Energy Inc. Analysts are enthused over the aggressive strategy, too.

Pointing to “a deep drop-down inventory” and its organic growth options, J.P. Morgan’s research report covering third-quarter earnings said, “we believe Marathon Petroleum has created a best-in-class growth MLP with MPLX.”

For all of its optimism, the target price set by J.P. Morgan’s Jeremy Tonet of $73 per share (the mid-November price was $68.86) is modest compared to other analysts. Shneur Gershuni of UBS is looking at $75, Brian Zarahn of Barclays expects $78 and Richard Roberts Jr. of Howard Weil Inc. predicts $79.

While declines in oil and gas prices have rattled some investors, Beall’s reminder that “MPLX’s fee-based portfolio has no direct exposure to commodity risk” was not lost on J.P. Morgan.

“Long-term contracts with substantial minimum volume commitments and no direct commodity price exposure underpinned ~73% of MPLX 2013 revenues,” the analysts wrote. “Additionally, we view [Marathon Petroleum Corp.] as a strong and strategic sponsor fully motivated to grow MPLX via dropdowns, acquisitions and organic growth.”

Big picture approach

Heminger, who doubles as president and CEO of MPC, intends to exploit that advantage.

“We have a very large inventory of assets that are eligible through our sponsor, Marathon Petroleum,” he said. “We move a tremendous amount of crude and refined products—and natural gasolines—in and out of our refineries. That gives us the ability to leverage those movements to get equity positions in other pipelines.”

MPC’s midstream and downstream operations encompass a wide swath of the industry in which many smaller operators do not engage. It means that Heminger’s management teams for both the sponsor and MLP must have a grasp of the business as a whole and know where opportunities lurk.

“It’s a very, very commercial operation, so I’m looking for people who have a very strong commercial acumen, understand where the value is across the supply chain,” he said. “There can be many different points of value across the supply chain. My management philosophy is to attract people who understand the business, know where the value components of the business are located and also have the savvy and communications skills to be able to put together strong opportunities to grow our business.

“Most importantly, it’s commercial acumen,” Heminger emphasized. “It’s not necessarily accounting, finance or engineering. It kind of takes the ability to understand all of the above.”

Challenges to come

Tonet sees a chance to re-evaluate the rating for MPLX as its growth picks up, and he likes the MLP’s balance sheet and drop-down plans.

“We expect MPLX to be an active participant in capital markets given its increased capital needs in the near-term, somewhat mitigated by MPC potentially taking back units against drops,” he wrote. “As MPLX gains meaningful scale, we expect the partnership to more actively participate in organic projects.”

What could go wrong?

There are no sure things. Tonet noted that MPLX has garnered a premium valuation based on its growth potential and the expectation that the enterprise will follow through. “Should dropdowns fail to meet market expectations or expansion projects not materialize as expected, MPLX may realize a lower growth trajectory and the market may assign a lower valuation to the partnership,” he wrote.

There is also the dependence of MPLX on its sponsor, Marathon Petroleum, which is generally perceived as a positive. Tonet pointed out that 90% of the MPLX’s revenues are tied to MPC. The general partner also guarantees minimum volume commitments.

“MPLX’s strength is highly dependent upon MPC, and any events adversely impacting Marathon Petroleum (especially a refinery shutdown) would weigh on the partnership as well,” he wrote.

Heminger is focused on quality.

“The challenges are to continue to have good quality projects, to be able to grow from an organic standpoint and also to be very quality-conscious as we look to be acquisitive,” he said.

He acknowledged that “we have a very large inventory of assets that are eligible through our sponsor, Marathon Petroleum,” but that’s just part of the plan.

“Our strategy is not just to be a drop-down story,” Heminger said. “We’re going to continue to be organic, and we would expect to continue to be acquisitive in how we would look at this type of business going forward. I think we have a very, very long growth profile in this space.”

Joseph Markman can be reached at jmarkman@hartenergy.com or 713-260-5208.

Recommended Reading

Aethon Dishes on Western Haynesville Costs as Gas Output Roars On

2025-01-22 - Aethon Energy’s western Haynesville gas wells produced nearly 34 Bcf in the first 11 months of 2024, according to the latest Texas Railroad Commission data.

Matador Touts Cotton Valley ‘Gas Bank’ Reserves as Prices Increase

2025-02-21 - Matador Resources focuses most of its efforts on the Permian’s Delaware Basin today. But the company still has vast untapped natural gas resources in Louisiana’s prolific Cotton Valley play, where it could look to drill as commodity prices increase.

Antero Stock Up 90% YoY as NatGas, NGL Markets Improve

2025-02-14 - As the outlook for U.S. natural gas improves, investors are hot on gas-weighted stocks—in particular, Appalachia’s Antero Resources.

BP’s Eagle Ford Refracs Delivering EUR Uplift, ‘Triple-Digit’ Returns

2025-02-14 - BP’s shale segment, BPX Energy, is seeing EUR uplifts from Eagle Ford refracs “we didn’t really predict in shale,” CEO Murray Auchincloss told investors in fourth-quarter earnings.

Comstock Doubling Rigs as Western Haynesville Mega-Wells’ Cost Falls to $27MM

2025-02-19 - Operator Comstock Resources is ramping to four rigs in its half-million-net-acre, deep-gas play north of Houston where its wells IP as much as 40 MMcf/d. The oldest one has produced 18.4 Bcf in its first 33 months.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.