In recent years, technological breakthroughs and sustained high oil prices helped shift the U.S. oil and gas transaction market toward onshore unconventional assets. Although unconventional transactions have recently dominated the upstream M&A space, there has been a noticeable shift to an increased number of conventional asset transactions. We expect this shift to continue gaining momentum due to valuations and the capital-intensive nature of unconventionals, consolidation in the “Big Three” oil plays (Permian, Eagle Ford and Bakken), yield-oriented acquisition appetite and a growing supply of available conventional opportunities.

Increasing valuations, high initial production rates and short payback periods have made unconventional assets popular acquisition targets, while also constricting demand for conventional assets. In 2007, conventional asset transactions in the U.S., excluding Gulf of Mexico activity, comprised 80% of transaction volume and 73% of transaction value. By 2010, the conventional asset transaction market share had fallen to 38% of transaction volume and 22% of transaction value.

During the same period, the average simple production transaction multiples in the Big Three soared from about $71,000 per flowing barrel of oil equivalent (boe) to about $267,000 per flowing boe. Although production multiple increases subsided in the subsequent years, averaging $144,000 per flowing boe, the value of unconventional asset transactions continued to dominate the M&A landscape.

After 2012, however, there was a significant uptick in conventional asset transaction activity, indicating a potential reversion to a more conventional-weighted transaction market.

Recent unconventional activity, particularly in the Big Three, indicates that there is considerable consolidation occurring across these plays. Evidence of this trend can be found in the Eagle Ford in Baytex’s acquisition of Aurora ($2.6 billion), Encana’s acquisition of Freeport McMoRan’s Eagle Ford asset ($3.1 billion) and Devon Energy’s acquisition of GeoSouthern Resources ($6 billion); in the Bakken in Whiting Petroleum’s acquisition of Kodiak Oil & Gas ($6 billion); and in the Permian in American Energy Partners’ acquisition of Enduring Resources ($2.5 billion) and Encana’s acquisition of Athlon Energy ($7.1 billion).

As consolidation continues, smaller assets are likely to get consumed by larger strategic buyers, forcing buyers who don’t have the appetite for larger transactions, or can’t compete with large strategics, to pursue alternative opportunities in other basins, which might shift demand to more conventional plays.

The increase in public and private yield-oriented acquisition activity has also contributed to a return to conventional assets, as these buyers are committed to making distributions to unitholders, and are therefore actively pursuing long-lived, low-decline assets due to their predictable and typically lower capital-intensive nature. Since 2010, the top four most-active upstream MLPs by total acquisition value, Linn Energy, BreitBurn Energy Partners, Vanguard Natural Resources and Memorial Production Partners, are in the top 10 buyers of conventional assets and have executed more than $15 billion of transactions. As yield-oriented investment vehicles continue to expand in the upstream space, they will continue to have a significant impact on the M&A marketplace, furthering momentum in the conventional market.

Pure-play pursuit

The supply of conventional assets has also been subject to changing market dynamics. The expansion of the unconventional market has led some operators with robust unconventional asset bases to divest conventional assets so as to be perceived as “pure play” companies and to provide a source of capital to develop higher return assets. This trend is increasing the amount of conventional assets that are coming to market, resulting in increased conventional transaction activity.

Some recent 2014 examples of this dynamic are Devon Energy’s sale of diversified conventional assets to Linn ($2.3 billion), Pioneer Natural Resource’s sale of Hugoton Field assets to Linn ($340 million) and WPX Energy’s sale of its Piceance Basin asset to Legacy Reserves ($355 million).

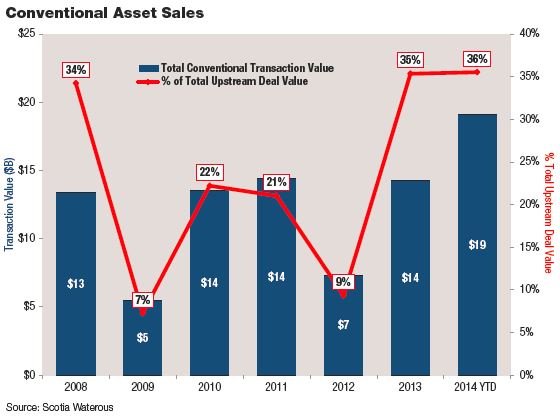

The development in unconventional assets, the proliferation of yield-oriented investment vehicles, and the increase in conventional acquisition opportunities have already had a material effect on the conventional asset market. Since 2012, conventional transactions as a percentage of total upstream U.S. transaction value increased from 9% to 35% in 2013 and 36% year-to-date in 2014. Although unconventionals have dominated headlines, conventional assets are poised to make a strong comeback.

—Buddy Carruth, Chase Machemehl and Robert Urquhart, Scotia Waterous, 713-437-5045,

buddy.carruth@scotiabank.com

Recommended Reading

Shell Shakes Up Leadership with Upstream and Gas Director to Exit

2025-03-04 - Zoë Yujnovich, Shell’s Integrated Gas and Upstream director, will step down effective March 31.

Occidental Temporarily Reduces Warrants Price to Raise $1.6B

2025-03-03 - Occidental Petroleum’s offer to warrant-holders at a reduced exercise price of $21.30 would raise $1.6 billion, the company said.

Dividends Declared Week of Feb. 24

2025-03-02 - As 2024 year-end earnings wrap up, here is a compilation of dividends declared from select upstream and midstream companies.

Q&A: Patterson’s OFS Perspective on the Shale Boom, Pandemic and Current Upswing

2025-02-27 - Former Basic Energy Services CEO Roe Patterson details his perspective on the shale boom and the lessons learned to get back to the current upswing in the industry.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.