A recent gathering of energy economists in Boulder, Colo., featured speakers ranging from oil-price bears to bulls. The 43rd Annual International Energy Conference, sponsored by the International Research Center for Energy and Economic Development (ICEED), attracts the best and brightest of the trade and always provokes lively discussions.

Julian Lee, a London-based oil strategist for Bloomberg News, offered some salient points on OPEC’s role in today’s world. OPEC’s goal has always been to safeguard the interests of its member countries, noted Lee. The organization’s members are diverse, consisting of one group of countries with low-cost, high per-capita production: Kuwait, Qatar, United Arab Emirates (UAE) and Saudi Arabia, and a second group with mixed-cost, low per-capita production: Angola, Venezuela, Libya, Ecuador, Iraq, Algeria, Iran, Nigeria and Indonesia.

“The priorities of these two groups are different,” Lee said. Criteria proposed by OPEC members for setting output quotas has ranged from oil reserves and production capacity to cost of production and levels of external debt, with members’ population and dependence on oil exports also considered. Not surprisingly, it’s difficult for countries with such differing situations to agree on a common strategy.

And make no mistake: A fundamental characteristic of OPEC is that decisions are made by consensus. The group has no power to compel its members to adhere to any of its agreements or guidelines, Lee said. “OPEC exists to serve the interests of its members—that is its only purpose.”

That said, observers have come to expect OPEC to rein in oil production from its member states when commodity prices fall to low levels. At least, that is what OPEC countries did in 1998-1999, when they cut output by 3 million barrels a day (MMbbl/d). Again in 2000-2001, OPEC took 5.4 MMbbl/d out of the market. And in 2008-2009, the group collectively cut its production by 4.3 MMbbl/d.

However, during the current price downturn, OPEC countries have increased their production levels by 2.1 MMbbl/d. The intent, according to Lee, is to drive higher-priced oil off the market— such sources as U.S. shale oil, Canadian oil sands and worldwide deepwater projects. “The policy is working— non-OPEC production is declining and is expected to continue to decline,” he said.

Much has been made of the idea that Saudi Arabia cannot withstand low oil prices for long, as its costs for social programs add a great burden to its breakeven economics. This is a fallacy, Lee said. Saudi Arabia’s foreign capital assets are down just 21% from their peak of some US$730 billion in August 2014, and at some $590 billion currently, are still well above historical levels. Indeed, in 2006, the kingdom had less than $200 billion in foreign assets.

“The point of having money in the bank is to spend it when you need it. I’m amazed that countries such as the U.S. and Japan have run on deficits for many years; yet that is something the Saudis are not supposed to do? Just about anyone in the world would lend Saudi Arabia money,” Lee said.

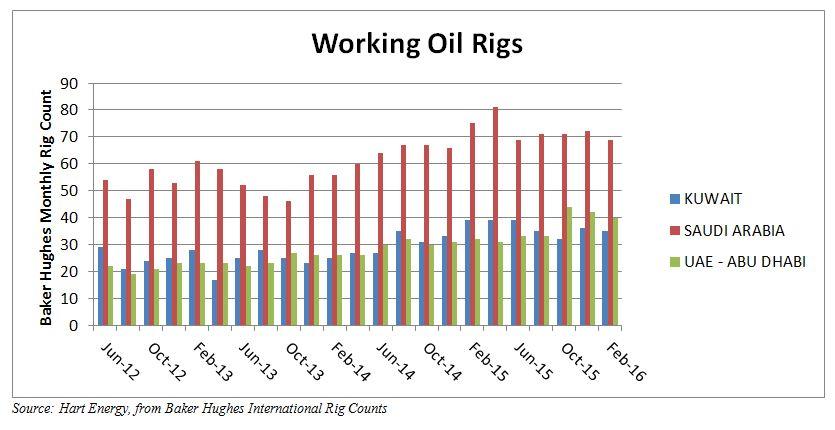

Another fascinating trend is that despite the worldwide collapse of drilling activity, oil rig counts in Saudi Arabia, the UAE and Kuwait have been steady to rising. From a level of just above 50 oil-directed drilling rigs working in January 2012, Saudi Arabia now has nearly 70 such rigs at work.

“We can’t underestimate OPEC’s ability to overcome, or simply ignore, its contradictions,” Lee noted. The fractious organization has exhibited remarkable durability, surviving the invasion of two founding members by a third one; it’s never managed to craft a rational quota system; and it has welcomed back a former member, Indonesia, that is no longer a net oil exporter.

OPEC is certainly still relevant, and unfortunately for the oil-price bulls, it appears to be continuing a successful campaign of ensuring that its oil is the oil that the world will consume.

Sheikh Yamani once famously said, “The Stone Age did not end because the world ran out of stones, and the oil age will not end because we run out of oil.” His words, spoken in 2000, were a warning to OPEC members of the risks associated with pursuing ever-higher oil prices. It is a warning that some in OPEC appear to have heeded at last.

Recommended Reading

EON Deal Adds Permian Interests, Restructures Balance Sheet

2025-02-11 - EON Resources Inc. will acquire Permian overriding royalty interests in a cash-and-equity deal with Pogo Royalty LLC, which has agreed to reduce certain liabilities and obligations owed to it by EON.

Buying Time: Continuation Funds Easing Private Equity Exits

2025-01-31 - An emerging option to extend portfolio company deadlines is gaining momentum, eclipsing go-public strategies or M&A.

Viper to Buy Diamondback Mineral, Royalty Interests in $4.45B Drop-Down

2025-01-30 - Working to reduce debt after a $26 billion acquisition of Endeavor Energy Resources, Diamondback will drop down $4.45 billion in mineral and royalty interests to its subsidiary Viper Energy.

USD Partners Expects to Sell Final Asset by Mid-April

2025-01-22 - USD Partners was obligated to sell the Hardisty terminal after entering a forbearance agreement with its lenders in June 2024.

Mach Prices Common Units, Closes Flycatcher Deal

2025-02-06 - Mach Natural Resources priced a public offering of common units following the close of $29.8 million of assets near its current holdings in the Ardmore Basin on Jan. 31.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.