Although the end of 2014 might have shown the midstream industry nearing the end of MLPs that can be spun off from the large integrated companies, that doesn’t mean there’s an expected shortage of MLP IPOs to be filed in the new year, analysts say.

“I think we’re kind of nearing the end of MLPs that can be spun off from big companies. There aren’t too many of those left,” Hinds Howard, vice president and senior financial analyst at CBRE Clarion Securities told Midstream Business.

“We’ve got Hess Corp. that’s on file probably for [filing] early next year. Also Sempra, but not too many left. The utilities were the last ones. We had Dominion, CenterPoint/OG MLPs this year,” Howard explained, and some others have been discussed behind-the-scenes by bankers for several years.

The holdouts

However, for the most part, he said, “They’re finally coming to market. I think these are the last holdouts of people who didn’t want to do an MLP for many years, for whatever reason. Maybe they just didn’t want to deal with the hassle. But the allure of the MLP IPOs has finally, I think, reached everybody.”

What generates that allure varies for different companies, Howard said.

“The reasons a sponsor would do an MLP: They get a higher valuation, so all the reasons you would have an MLP are constants. I think a lot of times it’s driven by capital needs at the parent company. If, at the parent company, they’ve got a lot of drilling capex they need to do, one source of that can be selling assets into an MLP and they can take the proceeds back to put into their business. That’s usually one of the drivers. Sometimes it’s hedge funds, getting in and being activists and saying, ‘Why aren’t you doing an MLP?’”

Beyond that, success breeds success—as midstream companies watched their peers succeed, they were drawn into the fray. A key driver for some of these recent IPOs was the Western Gas IPO in 2012. Western Gas Equity Partners LP went public, and it put a value on what Anadarko Petroleum Corp. was able to create with its midstream MLP; that value was somewhere in the neighborhood of $4 billion, just on the general partner (GP) stake. That was value created in the four years prior to taking the GP public out of just the incentive distribution rights (IDRs)—vast sums of money generated, basically, from nothing, Howard said.

“That was a wake-up call to companies that had midstream assets within upstream companies or within utilities to see that they could do an MLP, ramp up the cash flows really fast, and then do a GP IPO and all of a sudden, they have a similar $4 billion of value created out of thin air,” he explained. “That’s real money. For a long time, some of these big companies, whether it’s Phillips 66 or [Royal Dutch Shell Plc], they were averse to doing an MLP because it wouldn’t move the needle. It wasn’t going to make enough difference, and I think when Anadarko showed they could make that kind of money in four years, it was a wake-up call to them because $4 billion is something that matters to companies.”

Shell’s IPO

Indeed, when Shell made the move to spin off its midstream assets last fall, its offering generated more money than had been seen in 10 years of IPOs: $1.06 billion.

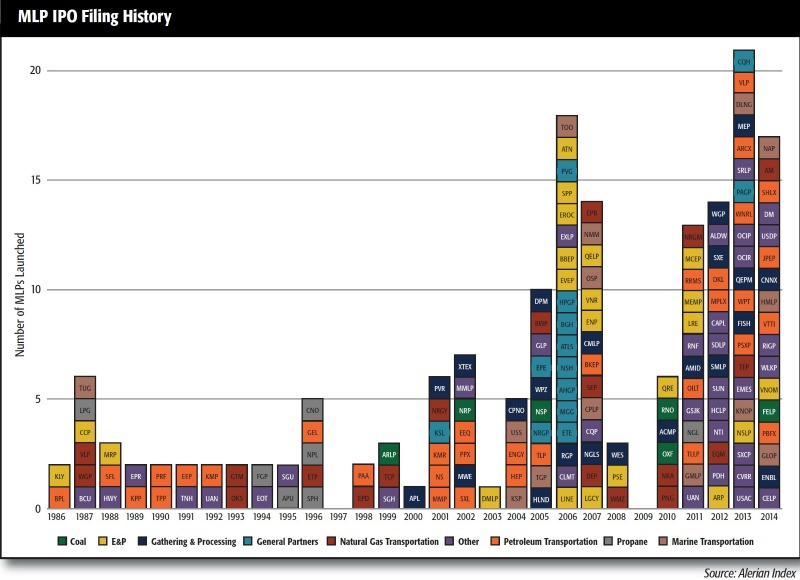

2013 was a record year for MLP IPOs with 21 offerings. However, in 2014, the value of the 18 IPOs filed by early December had surpassed 2013, according to Dealogic, with a record $6.8 billion generated compared to last year’s $5.9 billion.

But just because perhaps the biggest companies are reaching the tipping point for spin-offs, experts say that doesn’t mean a slowdown on MLP offerings is around the corner.

Kenny Feng, president and CEO of the Alerian Index, a bellwether in the MLP sector, noted that as companies such as Shell, Marathon Oil Co. and Phillips 66 Co. have been “rewarded” with good returns, the “drop-down” concept might not be complete. He added that as use of MLPs has matured, they’ve evolved more from being just an asset class into a structure that’s becoming not only more alluring, but more open-ended.

Kenny Feng, president and CEO of the Alerian Index, a bellwether in the MLP sector, noted that as companies such as Shell, Marathon Oil Co. and Phillips 66 Co. have been “rewarded” with good returns, the “drop-down” concept might not be complete. He added that as use of MLPs has matured, they’ve evolved more from being just an asset class into a structure that’s becoming not only more alluring, but more open-ended.

“You’ve seen different businesses up and down the value chain, as well as outside of it, employ the MLP structure, so it’s really more of a structure than an asset class at this point,” Feng told Midstream Business. “I would tell you there are many different businesses that are either thinking about putting themselves into the MLP structure, or have been pushed by their shareholder activists to do so. So certainly, you could see a higher degree of interest in using the structure and finding a new base of investors in the coming year. I would say maybe more so than has been the case in the past.”

To be sure, several different sectors of the energy industry are expected to file MLP IPOs in 2015. Among them, Feng said, LNG, oilfield services, saltwater disposal and marine transportation may become MLP players.

IDRs

The move by Kinder Morgan Inc. to roll-up its MLPs into a corporation brought to light some questions regarding how IDRs might impact further proliferation of MLPs. The IDRs at Kinder, one of the oldest MLPs, had reached the 50% rate, in which significant income went to the general partner and left the MLP with a higher cost of capital.

But MLP investors can take heart that the Kinder Morgan transaction was more a one-off deal than a symptom of a problem with the structure, Feng said.

“It takes more to move the needle of a $100 billion company than a $10 billion company or a $1 billion company. From a pure size standpoint, in order to continue to grow, which is the hallmark of the MLP base, continuing to get—not just stable distribution, but growing distributions—the size issue was one factor that came into play, combined with that was the fact they were in the high splits. Most of the MLPs that are up there— \the larger mega caps—those guys are in a very different position,” he said.

For example, Enterprise Products Partners LP phased out its IDRs several years ago. A decade ago, Copano Energy LLC, which was acquired by Kinder Morgan in 2013, filed its offering without IDRs.

“The late John Eckel Jr. [former CEO of Copano], who thought of himself as wanting investors to invest alongside [him] and be long-term ‘greedy,’ chose not to use IDRs,” Feng explained. “And he took the stance that it’s arbitrary these things even exist, and if he was feeling particularly combative on a particular day, he would tell you the existence of IDRs has been described as a necessary offensive for the general partner to grow the distribution. And again, if he was feeling combative on a particular day, he’d say, ‘Why does the general partner need an incentive to grow the distribution besides specifically growing the distribution from a cash flow standpoint?’’’

But ultimately, most MLPs choose to go with an IDR structure when they make that public offering. Feng explained: “Highlighting the general partner, they’re just not disincentivized to do it. Until you see the marketplace push back on it, there’s not going to be a reason for the issuer to eliminate this structure for no reason. They say, ‘I can choose to do it and the marketplace isn’t punishing me for it, so why not?’”

The crystal ball

Although some companies are seeing their share prices tank with the decline in oil prices, midstream, if it’s not insulated, is at least in a safer position than most other parts of the energy industry.

“[Midstream] is a safer place, I imagine, than the upstream guys. It’s just a function of how far you are from the wellhead,” said Feng. “For example, many MLPs that are in the gathering business have minimum volume commitments and are generally fee-based businesses, so gathering is a little bit less exposed than E&P or the service companies. In those cases, you’re better insulated from what’s happening.

“If the question is, ‘What is going to have the least amount of volatility as crude prices settle out?’ then you can probably say midstream is relatively safer.”

Which means MLP IPOs aren’t likely to stop just because the price of oil drops. At CBRE, Howard said he anticipates at least a dozen new MLPs will make public offerings next year.

“I think we could see something threaten the record for size that Shell set,” he said. “Given how popular these IPOs have become and given how big the institutional market is, I think we could see a $1 billion IPO in 2015.”

Deon Daugherty can be reached at ddaugherty@hartenergy.com or 713-260-1065.

Recommended Reading

Artificial Lift Firm Flowco’s Stock Surges 23% in First-Day Trading

2025-01-22 - Shares for artificial lift specialist Flowco Holdings spiked 23% in their first day of trading. Flowco CEO Joe Bob Edwards told Hart Energy that the durability of artificial lift and production optimization stands out in the OFS space.

Exxon Slips After Flagging Weak 4Q Earnings on Refining Squeeze

2025-01-08 - Exxon Mobil shares fell nearly 2% in early trading on Jan. 8 after the top U.S. oil producer warned of a decline in refining profits in the fourth quarter and weak returns across its operations.

Artificial Lift Firm Flowco Seeks ~$2B Valuation with IPO

2025-01-07 - U.S. artificial lift services provider Flowco Holdings is planning an IPO that could value the company at about $2 billion, according to regulatory filings.

Utica’s Infinity Natural Resources Seeks $1.2B Valuation with IPO

2025-01-21 - Appalachian Basin oil and gas producer Infinity Natural Resources plans to sell 13.25 million shares at a public purchase price between $18 and $21 per share—the latest in a flurry of energy-focused IPOs.

Chevron Targets Up to $8B in Free Cash Flow Growth Next Year, CEO Says

2025-01-08 - The No. 2 U.S. oil producer expects results to benefit from the start of new or expanded oil production projects in Kazakhstan, U.S. shale and the offshore U.S. Gulf of Mexico.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.