While not a cause for celebration, NGL, natural gas and crude oil prices holding firm the week of Jan. 7 provided some needed relief to the marketplace as producers are hopeful that the pricing floor was finally met.

We frequently discuss shoulder seasons—basically the early fall and spring periods between winter and summer when heating/cooling demand are at their lowest. In 2015, we’re in the midst of another form of shoulder season: one in the center of the market’s nominal peak demand season, but instead experiencing lower prices due to an oversaturated market.

The outlook for crude prices has been mixed, with several analysts, notably Goldman Sachs, stating that values could fall below $40 per barrel (bbl). However, other firms, such as Barclays Capital, En*Vantage and Global Hunter Securities are targeting prices above this threshold in 2015.

According to En*Vantage, geopolitical risks in economically weak oil producing nations could cause production declines or disruptions. “There is no way that geopolitical risks are not increasing in these countries and yet the market has completely wiped out the price risk premium for crude disruptions or declines in these unstable regions. We look for crude prices to retrace some of the gains that were achieved [this week] and hope to see some consolidation in the $45 to $50 range over the next several weeks,” the firm said in its Weekly Energy Report for Jan. 15.

Barclays Capital also anticipates crude prices will consolidate, as it retained a neutral outlook. “While the absence of bottoming patterns in price makes us reluctant to call for a base, we do expect a period of consolidation. … We expect prices to acclimatize at lower levels and would only turn bearish again on a break below support in the $45.37/bbl area. Such an instance would signal a further downside squeeze towards the $32.50/bbl area, the lows of 2008. For now, sideways chop is most likely as investors catch their breath,” the investment firm said in a Jan. 13 research note.

Global Hunter Securities anticipates a near-term drop in values with West Texas Intermediate prices falling to the mid-$40s/bbl, which is roughly its current value of $46.28/bbl as of Jan. 15. Gasoline demand has been increasing while prices fall to five-year lows as drivers are adding more mileage and, increasingly, buying less fuel-efficient vehicles such as trucks and SUVs.

Though many analysts have concluded that the increased sale of these vehicles is directly tied to the downturn in crude and gasoline prices, Jeep reported that it was on track to achieve its record sales level even before this turnaround. In addition, Ford’s F-150 has long been the nation’s best-selling vehicle.

“When we were still at $3.80 per gallon (gal), we were still up 38% year-over-year. We ended the year up 41%. So our growth story was happening prior to the lows we’re seeing today,” Fiat Chrysler CEO Sergio Marchionne told the Associated Press. This indicates that there is still room for North American consumer demand even if, and when, crude prices improve in the future.

Even if buyers begin to shy away from SUV buying in the coming years, this buying spree—caused from a combination of the need to replace older vehicles and the cold winters experienced the past two years—will help to increase gasoline demand as the lower fuel efficiency these vehicles provide will remain with customers for at least five years on average.

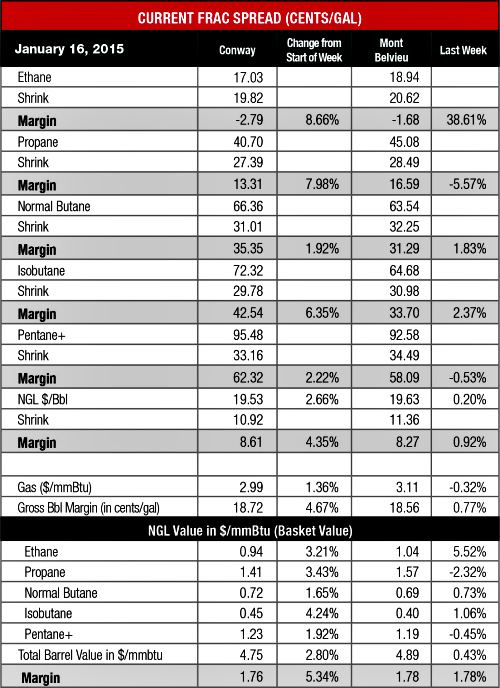

The cold temperatures being experienced in the Midwest and Northeast are helping to increase heating demand, which should begin to support gas and propane prices. These demands resulted in Conway prices, which are more susceptible to heating demand, to improve. However, Mont Belvieu prices took a downturn as LPG export demand is falling as the arb for Asia and Europe is less than transportation costs based on forward prices. This could lead to delivery cancellations in March, according to En*Vantage.

Though the outlook for propane is gloomy, ethane is at last undergoing its turnaround (see this week’s story). After a rough 18 months, the combination of ethane rejection and increased cracking capacity is having a positive impact on the market. Prices rebounded 3% at Conway to 17 cents/gal and 6% at Mont Belvieu to 19 cents/gal. Though the Mont Belvieu price is 10 cents/gal lower than at the same time last year, the Conway price is nearly level. Both are indications of an improving market when you factor in the large downturns being experienced by other NGL prices in the same 12-month period.

The theoretical NGL bbl price improved at both hubs with the Mont Belvieu price up slightly to $19.63/bbl with a 1% increase in margin to $8.27/bbl while the Conway price rose 3% to $19.53/bbl with a 4% improvement in margin to $8.61/bbl.

The most profitable NGL to make at both hubs was C5+ at 62 cents/gal at Conway and 58 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 43 cents/gal at Conway and 34 cents/gal at Mont Belvieu; butane at 35 cents/gal at Conway and 31 cents/gal at Mont Belvieu; propane at 13 cents/gal at Conway and 17 cents/gal at Mont Belvieu; and ethane at negative 3 cents/gal at Conway and negative 2 cents/gal at Mont Belvieu.

Frigid winter temperatures saw gas storage withdrawals go sky high the week of Jan. 9 as the U.S. Energy Information Administration reported that storage was down 236 billion cubic feet to 2.853 trillion cubic feet (Tcf) from 3.089 Tcf the previous week. This was 11% above the 2.571 Tcf posted last year at the same time and 4% below the five-year average of 2.966 Tcf.

Recommended Reading

SLB Earnings Rise, But Weakened 4Q and 2025 Ahead Due to Oil Glut

2024-10-22 - SLB, like Liberty Energy, revised guidance lower for the coming months, analysts said, as oilfield service companies grapple with concerns over an oversupplied global oil market.

Woodside Reports Record Q3 Production, Narrows Guidance for 2024

2024-10-17 - Australia’s Woodside Energy reported record production of 577,000 boe/d in the third quarter of 2024, an 18% increase due to the start of the Sangomar project offshore Senegal. The Aussie company has narrowed its production guidance for 2024 as a result.

BP Profit Falls On Weak Oil Prices, May Slow Share Buybacks

2024-10-30 - Despite a drop in profit due to weak oil prices, BP reported strong results from its U.S. shale segment and new momentum in the Gulf of Mexico.

Cibolo Energy Closes Fund Aimed at Upstream, Midstream Growth

2024-09-10 - Cibolo Energy Management LLC closed its second fund, Cibolo Energy Partners II LP, meant to boost middle market upstream and midstream companies’ growth with development capital.

TC Energy Completes Spinoff of Liquids Pipeline Business South Bow

2024-10-01 - South Bow Corp. will commence trading on the Toronto Stock Exchange on Oct. 2.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.