West Texas Intermediate (WTI) crude prices took another downturn the week of March 11 as storage at the Cushing, Okla., hub is quickly filling up. Prices fell below $45 per barrel (bbl) and were $43.73/bbl at press time, which is at the bottom of the curve for the year.

According to Global Hunter Securities, the current level of 458.51 million bbl (MMbbl) at Cushing represents 30 days of supply, which is a high level but doesn’t represent an over-supplied market. “The recent blockages at the Houston Ship Channel likely created a burst of imports amidst continued higher U.S. production, resulting in a big increase in U.S. supplies. Crude imports increased by 703,000 bbl/d to 7.5 MMbbl/d, explaining part of the supply outbreak,” the firm said in a March 18 research note.

Global Hunter Securities anticipates domestic production growth to max out between late May and late July. In the meantime, the note warned that challenges to storage capacity could get “nastier” by May, which could further deteriorate WTI prices. However, as noted last week, Cushing storage and transportation capacity has improved in the last few years. It is possible that the market could improve if capacity constraints are avoided.

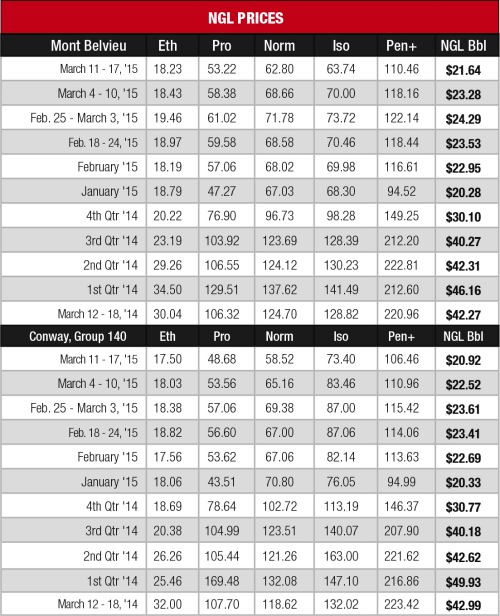

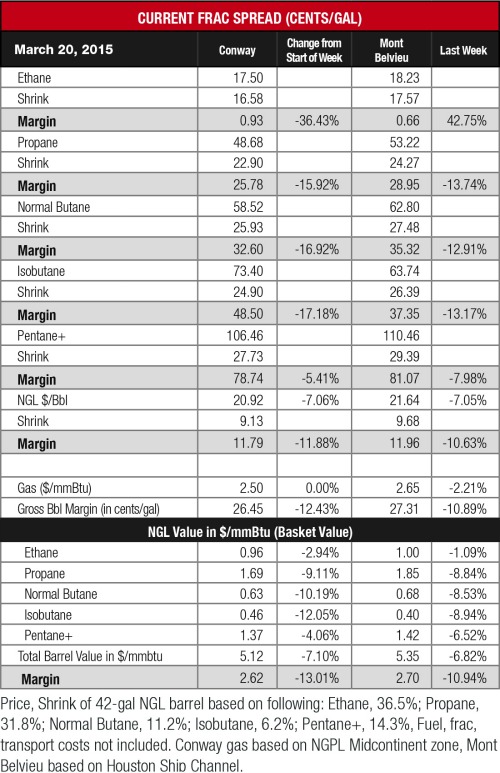

Crude’s impact on NGL prices cannot be overstated at this time, as prices took hits across the board at both Conway and Mont Belvieu. Butane and isobutane had the largest price decreases at both hubs— the switch from winter-grade gasoline blending to summer-grade gasoline makes them the most sensitive to downturns at this time of year.

The Conway isobutane price had the largest price decrease of any NGL at either hub, declining 12% to 73 cents per gallon (gal), its lowest price since it was 72 cents/gal the week of Jan. 7. The Mont Belvieu price fell 9% to 64 cents/gal, its lowest price since the week of Dec. 3, 2008, when it was 61 cents/gal.

Butane was down 10% at Conway to 59 cents/gal, its lowest price since it was 50 cents/gal the week of Dec. 3, 2008. The Mont Belvieu price fell 9% to 63 cents/gal, its lowest price since the same week of Dec. 3, 2008, when it was 57 cents/gal.

The lone NGL to maintain a value over $1.00/gal was C5+ as it was $1.05/gal at Conway and $1.11/gal at Mont Belvieu. Both prices were the lowest they have been since the week of Jan. 28.

Though lower crude prices are having the biggest impact on heavy NGL prices, light NGL prices are facing their own headwinds. Propane storage remains very high and will need a strong arb to encourage LPG exports to help balance the market. The shutdown of the Houston Ship Channel revealed how important exports are to the propane market as prices fell 9% at both hubs to their lowest levels in six weeks.

Ethane prices were negatively impacted by outages and slowdowns at several crackers. Both Huntsman International’s Port Neches, Texas, ethylene plant and Dow Chemical’s St. Charles #1 plant in Louisiana both are undergoing scheduled turnarounds. In addition, there were reported operational issues at ExxonMobil Corp.’s Baytown, Texas, cracker and The Williams Cos. Inc.’s Geismar, La., plant that may take a few weeks to repair.

The theoretical NGL bbl price fell 7% at both hubs with the Conway price down to $20.92/bbl with a 12% decrease in margin to $11.79/bbl. The Mont Belvieu price fell to $21.64/bbl with an 11% drop in margin to $11.96/bbl.

The most profitable NGL at both hubs remained C5+ at 79 cents/gal at Conway and 81 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 49 cents/gal at Conway and 37 cents/gal at Mont Belvieu; butane at 33 cents/gal at Conway and 35 cents/gal at Mont Belvieu; propane at 26 cents/gal at Conway and 29 cents/gal at Mont Belvieu; and ethane at 1 cent/gal at both hubs.

Natural gas storage withdrawal levels were greatly reduced the week of March 13 due to warmer temperatures throughout the U.S. The U.S. Energy Information Administration reported that storage was down 45 billion cubic feet (Bcf) to 1.467 trillion cubic feet (Tcf) from 1.512 Tcf the previous week. This was 53% greater than the 960 Bcf posted last year at the same time and 13% lower than the five-year average of 1.692 Tcf.

There could be solid withdrawals from storage the week of March 25 as the National Weather Service is forecasting colder-than-normal temperatures throughout much of the country, including the East Coast, Midwest and Gulf Coast. This will be somewhat balanced by warmer-than-normal temperatures along the West Coast.

Contact the author, Frank Nieto, at fnieto@hartenergy.com.

Recommended Reading

Midstream M&A Adjusts After E&Ps’ Rampant Permian Consolidation

2024-10-18 - Scott Brown, CEO of the Midland Basin’s Canes Midstream, said he believes the Permian Basin still has plenty of runway for growth and development.

Post Oak-backed Quantent Closes Haynesville Deal in North Louisiana

2024-09-09 - Quantent Energy Partners’ initial Haynesville Shale acquisition comes as Post Oak Energy Capital closes an equity commitment for the E&P.

Analyst: Is Jerry Jones Making a Run to Take Comstock Private?

2024-09-20 - After buying more than 13.4 million Comstock shares in August, analysts wonder if Dallas Cowboys owner Jerry Jones might split the tackles and run downhill toward a go-private buyout of the Haynesville Shale gas producer.

Aethon, Murphy Refinance Debt as Fed Slashes Interest Rates

2024-09-20 - The E&Ps expect to issue new notes toward redeeming a combined $1.6 billion of existing debt, while the debt-pricing guide—the Fed funds rate—was cut on Sept. 18 from 5.5% to 5%.

Dividends Declared Sept.16 through Sept. 26

2024-09-27 - Here is a compilation of dividends declared from select upstream, midstream and service and supply companies.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.