For the first time in more than a year ethane can claim a positive margin at both Mont Belvieu and Conway. Granted, these positive margins are quite slim and once transportation fees are calculated, they are no longer positive, but it is a great sign for the market. This is especially true when you consider that there is still a great deal of storage to work off, which bodes very well for ethane’s long-term outlook when supplies tighten.

The improvement in crude oil prices helped support NGL values, but ethane prices held firm while other product prices plummeted. Since ethane makes up the bulk of the NGL barrel and is expected to post gains beginning later in the first quarter with cracking capacity at its peak level, it is a positive sign for NGL producers.

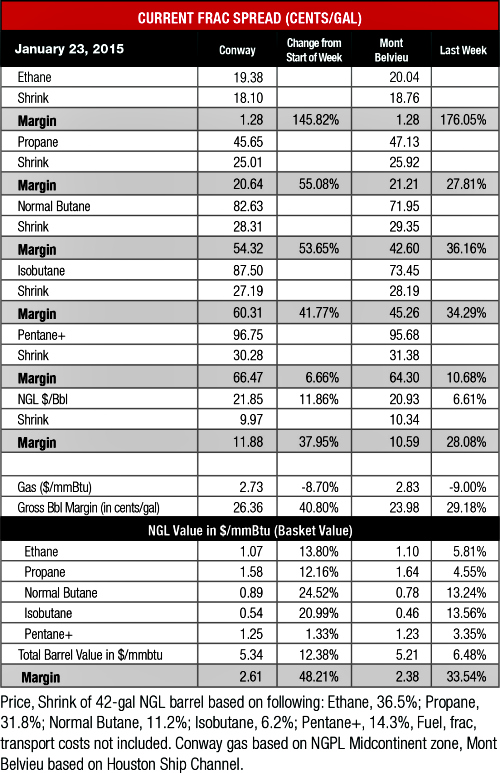

The price of ethane rose 14% to 19 cents per gallon (gal) at Conway. This was its highest price since it was 21 cents/gal the week of Nov. 12, 2014. The Mont Belvieu price improved 6% to 20 cents/gal, its highest price since it was 22 cents/gal the week of Nov. 12.

Heavy NGL prices posted the largest gains of any NGL thanks to their close relationship to crude as well as increased demand for gasoline. The gains posted by isobutane and butane were also a price correction as gasoline blending demand is ostensibly at its highest level in the winter.

Butane posted a 25% gain at Conway and a 13% gain at Mont Belvieu while isobutane rose 21% at Conway and 14% at Mont Belvieu. By comparison, C5+ prices were muted as they posted a 3% gain at Mont Belvieu and a 1% gain at Conway.

While these gains are a positive turn compared to the previous nine weeks when prices lost so much value, there is still a great deal of room for improvement when you compare current prices to the level they had last year at the same time. During this time heavy NGL prices lost more than 50% in value. With refinery turnarounds looming in February and March, crude prices could continue to stumble through the rest of this quarter.

Propane prices are the most likely NGL to have to wait for a turnaround despite sizable heating demand coming from the Northeast and Midwest. The main issue for propane has been a storage overhang and a weakening LPG export market as export arbs are negligible, though this could be improving. A sustained rally for LPG exports would go a long way towards balancing the propane market, though it is unlikely we’ll be experiencing the highs of last winter anytime soon.

Frac spread margins were also supported by a downturn in natural gas prices, which fell 9% in value at both hubs. This was despite the large storage withdrawal figures the last two weeks and the arrival of colder temperatures in much of the country. Prices at both hubs were below $3 per million Btu, partially due to new pipelines that bring increased production from the Marcellus and Utica shales to market.

“Cold temperatures have kept natural gas prices from falling further and freeze offs will also curb some output nationwide, but rapid production from newly connected pipelines is keeping growth rates robust. Since October, the start of 2.5 billion cubic feet (Bcf) per day of new Northeast pipelines in the Marcellus and the Utica formations has raised output and is mitigating the demand impact of the second harsh cold spell of the season,” Barclays Capital said in a Jan. 12 research note. It is unlikely that gas prices will fall much further, but their growth rate is capped by this production coming into the market.

The theoretical NGL barrel (bbl) price rose 12% at Conway to $21.85/bbl with a 38% gain in margin to $11.88/bbl while the Mont Belvieu price increased 7% to $20.93/bbl with a 28% gain in margin to $10.59/bbl.

The most profitable NGL to make at both hubs remained C5+ at 67 cents/gal at Conway and 64 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 60 cents/gal at Conway and 45 cents/gal at Mont Belvieu; butane at 54 cents/gal at Conway and 43 cents/gal at Mont Belvieu; propane at 21 cents/gal at both hubs; and ethane at 1 cent/gal at both hubs.

The U.S. Energy Information Administration reported that natural gas storage levels decreased by 216 Bcf to 2.637 trillion cubic feet (Tcf) the week of Jan. 16, down from 2.853 Tcf the previous week. This was 8% higher than the 2.438 Tcf posted last year at the same time and 6% below the five-year average of 2.79 Tcf.

Recommended Reading

Hurricane Francine Shuts in Quarter of GoM Oil, Gas Production

2024-09-11 - The Bureau of Safety and Environmental Enforcement reported that 130 platforms and several rigs were affected as the storm approached the Louisiana coast.

US Oil Firms Evacuate Staff, Cut Drilling Ahead of Storm Francine

2024-09-09 - Francine is moving toward U.S. Gulf of Mexico waters and predicted to become the fourth hurricane of the Atlantic season.

Oil Prices Jump 4% on Reports of Iran Preparing to Attack Israel

2024-10-01 - An Israeli attack on Iranian oil production or export facilities could cause a material disruption, potentially more than a 1 MMbbl/d.

EQT Plans to Reverse Some US Natgas Production Curtailments in Oct, CEO Says

2024-09-25 - EQT, the biggest U.S. natural gas producer, has along with other U.S. drillers curtailed output in 2024 after prices collapsed to multi-year lows in the spring following a mild winter that left a tremendous oversupply of fuel in storage.

Oil Falls as Swelling US Supply Counters Middle East and Hurricane Risks

2024-10-09 - Oil fell on rising U.S. crude inventories but the risk of supply disruption from the Middle East and Hurricane Milton curbed price declines.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.