The direction of commodity prices remained uncertain as the final month of 2015 began. Fears over potential supply disruptions as a result of terrorist attacks in France and the downing of a Russian jet in Syria have supported crude prices with West Texas Intermediate (WTI) crude trading slightly above $41 per barrel (/bbl).

It is possible that prices could grow further in the short-term, but the near-term outlook is still negative as prices are still challenged due to oversupply. En*Vantage Inc. noted that while it is likely crude will drop below the $40/bbl threshold in the next several weeks, such a price level is not sustainable. A drop to this level will result in production screeching to a halt and would require higher prices to support drilling to resume once the supply overhang is worked off a bit.

It is expected that OPEC will stick with its policy of all-out production, which is causing hedge funds and money managers to increase their short positions in WTI and Brent futures near a record high. It is likely that this would result in prices falling to the mid-$30/bbl level and result in a period of volatility in the market.

“Although the fundamentals are not supportive, the mere fact that there is a large concentration of short positions makes the oil markets extremely vulnerable to price volatility. Recent history has shown that oil prices can rapidly snap back when they go below $40/bbl…If this snap back rally occurs it will not change the overall fundamentals, unless the trigger causes a significant supply response. High inventories and excess supplies still need to be worked off. In the meantime, expect WTI prices to be volatile and trade anywhere between $30/bbl and $50/bbl through the first-quarter 2016,” En*Vantage said in its December 3 Weekly Energy Report.

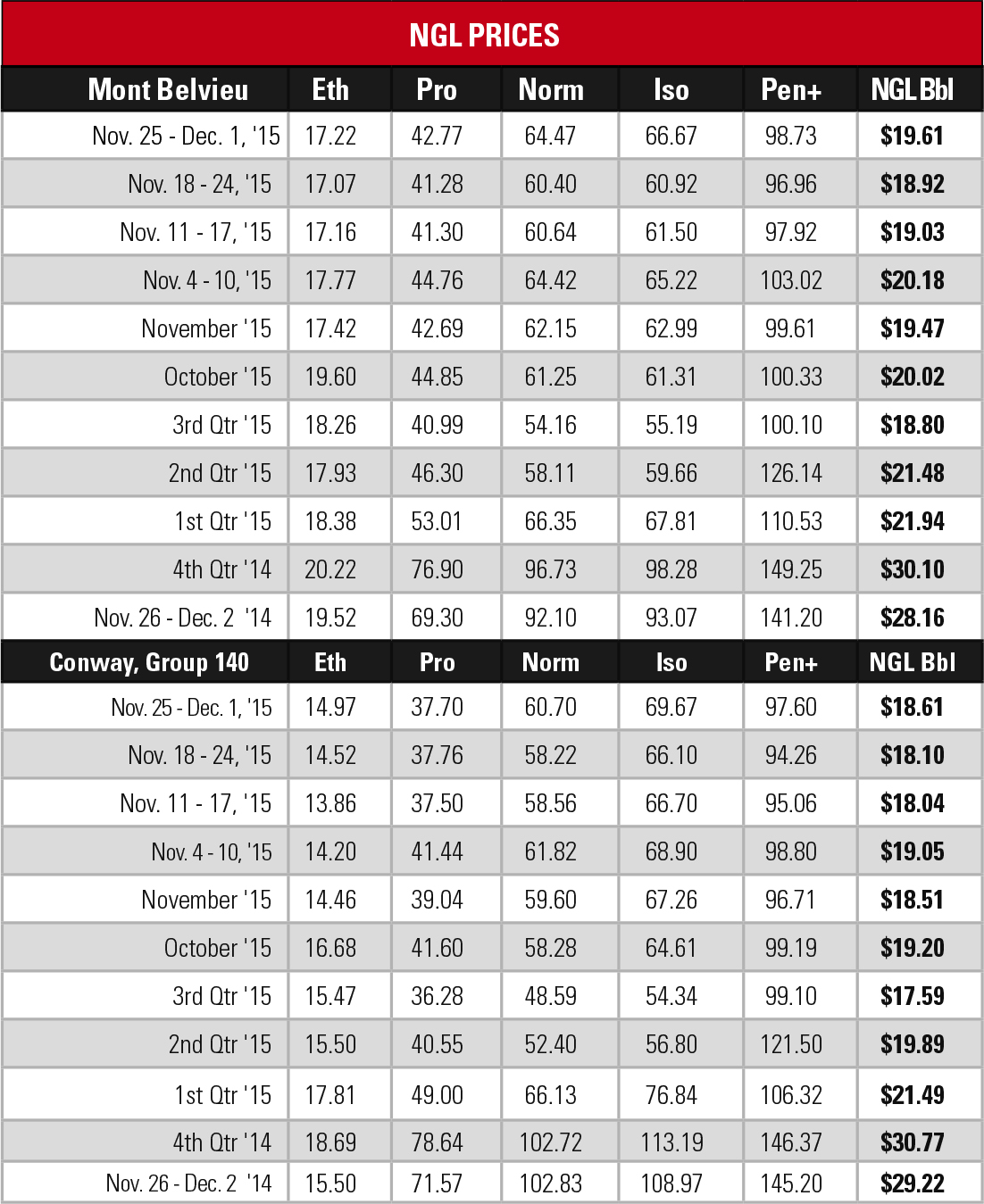

The situation with NGL prices is a bit more certain as the oversupplied market is capped to how much it can grow until the market is more balanced. Ethane has long been the NGL with the largest supply overhang, as it has been oversupplied for about three years despite steady rejection throughout the country.

The good news is that ethane cracking capacity is increasing in the coming months and the widespread rejection has begun to have a positive impact on supplies as storage levels are well below what they were last year at the same time. The bad news is that prices are still challenged at values under 20 cents per gallon (/gal) with thin margins at both Conway and Mont Belvieu.

These prices are also capped by propane, which has supplanted ethane as the most oversupplied NGL despite record high LPG exports. Lower prices put propane into direct competition with ethane as an ethylene feedstock, which lowers the ceiling for ethane prices to the level of propane’s floor price.

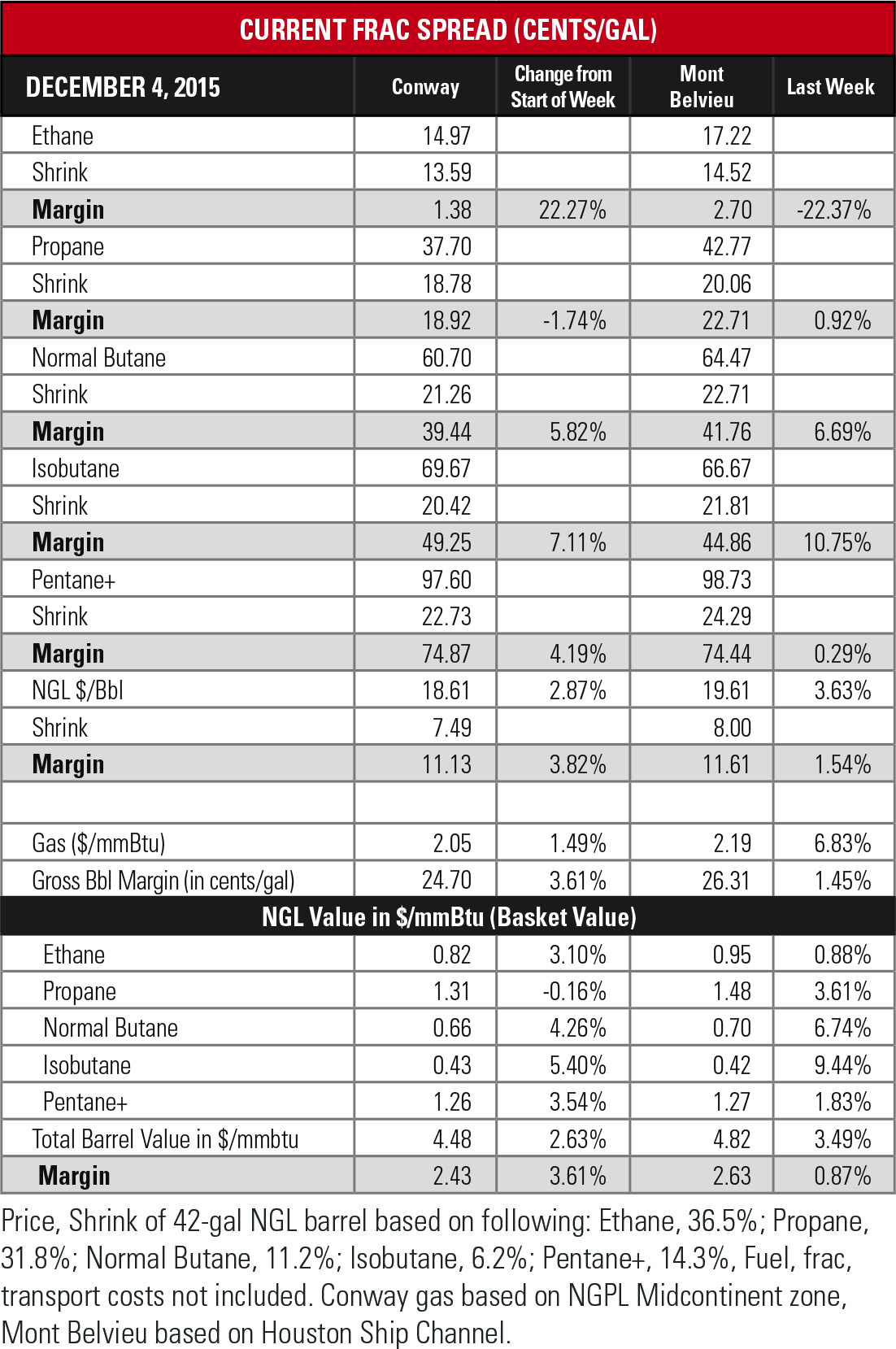

The overall theoretical NGL bbl price rose at both hubs with the Conway price improving 3% to $18.61/bbl with a 4% increase in margin to $11.13/bbl. The Mont Belvieu price rose 4% to $19.61/bbl with a 2% increase in margin to $11.61/bbl.

The most profitable NGL to make at both hubs remained C5+ at 75 cents/gal at Conway and 74 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 49 cents/gal at Conway and 45 cents/gal at Mont Belvieu; butane at 39 cents/gal at Conway and 42 cents/gal at Mont Belvieu; propane at 19 cents/gal at Conway and 23 cents/gal at Mont Belvieu; and ethane at 1 cent/gal at Conway and 3 cents/gal at Mont Belvieu.

Winter heating season formally began as the U.S. Energy Information Administration reported that natural gas storage levels fell by 53 billion cubic feet to 3.956 trillion cubic feet (Tcf) the week of November 27 from 4.009 Tcf the previous week. This was 16% greater than the 3.413 Tcf posted last year at the same time and 7% greater than the five-year average of 3.709 Tcf.

Recommended Reading

SLB Earnings Rise, But Weakened 4Q and 2025 Ahead Due to Oil Glut

2024-10-22 - SLB, like Liberty Energy, revised guidance lower for the coming months, analysts said, as oilfield service companies grapple with concerns over an oversupplied global oil market.

ConocoPhillips Hits Permian, Eagle Ford Records as Marathon Closing Nears

2024-11-01 - ConocoPhillips anticipates closing its $17.1 billion acquisition of Marathon Oil before year-end, adding assets in the Eagle Ford, the Bakken and the Permian Basin.

Woodside Reports Record Q3 Production, Narrows Guidance for 2024

2024-10-17 - Australia’s Woodside Energy reported record production of 577,000 boe/d in the third quarter of 2024, an 18% increase due to the start of the Sangomar project offshore Senegal. The Aussie company has narrowed its production guidance for 2024 as a result.

Dividends Declared in the Week of Sept. 2

2024-09-06 - Here is a compilation of dividends declared by select E&Ps for third-quarter 2024.

Record NGL Volumes Earn Targa $1.07B in Profits in 3Q

2024-11-06 - Targa Resources reported record NGL transportation and fractionation volumes in the Permian Basin, where associated natural gas production continues to rise.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.