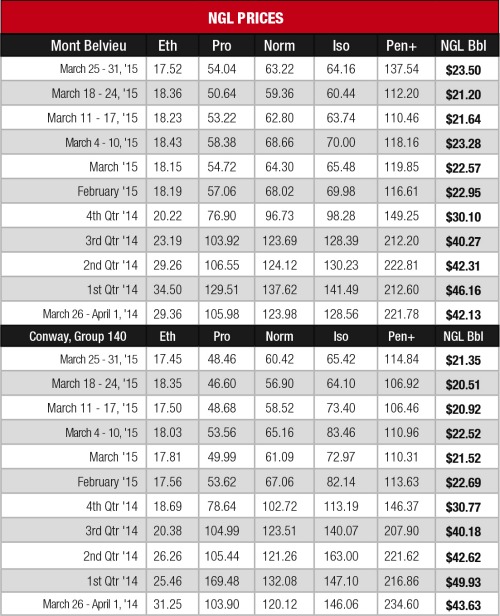

A shortage of pentanes-plus (C5+) along the Gulf Coast resulted in a Mont Belvieu price spike the final week of March due to increased demand from refiners ramping up summer-grade gasoline blending. Pentanes-plus prices also rose at Conway while butane prices rose at both hubs.

Mont Belvieu C5+ rose 23% to $1.38 per gallon (gal) its highest price since it was $1.41/gal the week of Nov. 26. This surge was largely responsible for the 11% gain in the theoretical NGL barrel (bbl) at the hub. The Conway price improved 7% to $1.15/gal, its highest price in a month.

While the NGL with the closest relationship to crude oil surged in value, West Texas Intermediate (WTI) crude continued to hover around $50/bbl, giving a clear indication that the movement on C5+ was market-based and not related to other markets.

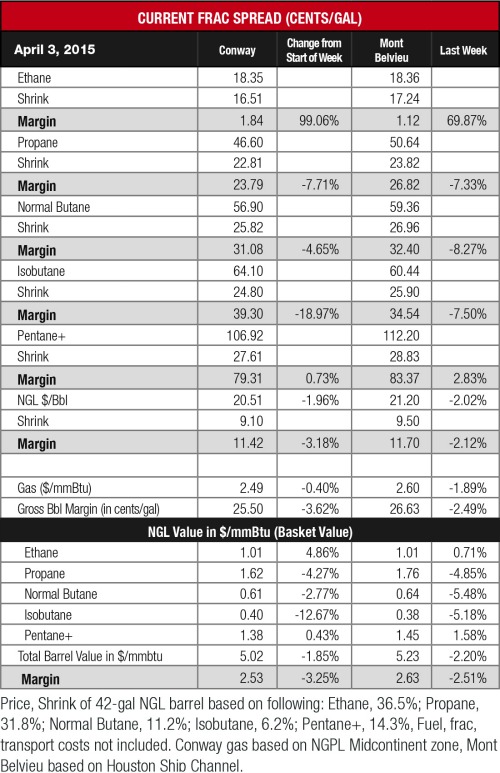

Indeed, the gains posted by butane and isobutane at both hubs were much more muted as they hit their highest level in about a month.

Crude prices are entering the weakest part of the year in the second quarter. This downturn is likely to operate as a headwind for heavy NGL prices. Barclays Capital noted in a March 31 research note that there were several factors that supported crude prices in the first quarter, which is a bit scary considering how far prices tumbled in the past six months. These factors include:

- Diesel and fuel oil demand increased this past winter due to colder-than-normal weather and natural gas infrastructure bottlenecks;

- Product margins for crude increased due to refinery strikes, unplanned outages in Latin America and the U.S. West Coast and the enforcement of low sulfur fuel oil use in Emission Control Areas;

- Production disruptions in Libya and Iraq;

- Stockbuilding in China at the end of 2014 and stockholding obligations in Europe; and

- A delayed oil price pass-through to LNG prices.

Despite the impact on crude demand, the market is expected to remain oversupplied by 2 million bbl/d in the second quarter. “New prices [expected] for Brent are unlikely and WTI is not expected to go below $40/bbl. Both prices are anchored by the back of the market and available storage capacity, even if it is floating,” PIRA Energy Group’s Weekly Oil Market Recap for the week ending March 29 said. “The magic is working to tighten oil markets but it takes time. Gasoline season looks healthy but new refinery capacity will pressure distillate. Political uncertainties are on the rise with the Nigerian elections, Saudi Arabia’s direct military involvement in Yemen and turmoil in Libya, among other things.”

Light NGL prices were a mixed bag as propane prices went up but ethane prices retreated very slightly. Interestingly, this occurred despite propane inventories increasing and was more likely due to prices having hit their floor the previous week. The Mont Belvieu propane prices rose 7% to 54 cents/gal, its highest price in a month, while the Conway price increased 4% to 49 cents/gal, its highest price in three weeks.

Frac spread margins were largely unchanged as gas prices fell with the advent of the spring shoulder season. The most profitable NGL to make at both hubs was C5+ at 79 cents/gal at Conway and 83 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 39 cents/gal at Conway and 35 cents/gal at Mont Belvieu; butane at 31 cents/gal at Conway and 32 cents/gal at Mont Belvieu; propane at 24 cents/gal at Conway and 27 cents/gal at Mont Belvieu; and ethane at 2 cents/gal at Conway and 1 cent/gal at Mont Belvieu.

There was a bit of a surprise as natural gas storage levels declined the week of March 27 with the U.S. Energy Information Administration reporting that storage declined by 18 billion cubic feet (Bcf) to 1.461 trillion cubic feet (Tcf) from 1.479 Tcf the previous week. This was 75% greater than the 833 Bcf posted last year at the same time and 12% lower than the five-year average of 1.651 Tcf.

Storage injections should return this coming week as heating demand will be very limited due to normal to warmer-than-normal temperatures expected around the country. This may result in limited cooling demand, but likely not enough to result in another withdrawal.

Contact the author, Frank Nieto, at fnieto@hartenergy.com.

Recommended Reading

Exxon Awards JGC, Technip Energies LNG FEED Contract

2024-09-26 - Technip Energies said Rovuma LNG, located in Mozambique, is expected to have a total production capacity of 18 million tonnes per annum.

Francine Closes, Restricts Oil Export Ports, Shuts in 42% of GoM Oil

2024-09-13 - In addition to hampering ports and refineries, an estimated 41.74% of Gulf of Mexico oil production, or 730,472 bbl/d, has been shut in.

US Oil Firms Evacuate Staff, Cut Drilling Ahead of Storm Francine

2024-09-09 - Francine is moving toward U.S. Gulf of Mexico waters and predicted to become the fourth hurricane of the Atlantic season.

Hurricane Francine Shuts in Quarter of GoM Oil, Gas Production

2024-09-11 - The Bureau of Safety and Environmental Enforcement reported that 130 platforms and several rigs were affected as the storm approached the Louisiana coast.

North American LNG Exports Surge: Texas Fuels Mexico’s Growth

2024-11-05 - Mexico is finally getting its feet off the ground with LNG exports, joining the U.S. to make North America an LNG exporting powerhouse.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.