Venezuelan President Nicolás Maduro cuts diplomatic ties with the U.S. as unrest develops in the country after opposition leader Juan Guaidó swore himself in as president. (Source: Shutterstock, PDVSA)

Those wondering what a complete meltdown of Venezuela would mean to global markets might soon find out.

On Jan. 23, opposition leader Juan Guaidó, president of the National Assembly, swore himself in as president of the country, defying sitting President Nicolás Maduro and immediately gaining recognition by the U.S., Argentina, Brazil, Canada, Chile, Colombia, Costa Rica, Paraguay, Peru and the Organization of American States. Maduro showed no inclination of stepping aside, blamed the U.S. for a coup attempt and severed diplomatic relations with Washington.

Assuming a stalemate in the short term, U.S. sanctions against Venezuela will deprive Gulf Coast refineries of affordable heavy crude. The country sold an average of 500,000 barrels per day (bbl/d) to the U.S. in 2018, and replacing that volume with supplies from Canada and Mexico is more costly.

Assuming a stalemate in the short term, U.S. sanctions against Venezuela will deprive Gulf Coast refineries of affordable heavy crude. The country sold an average of 500,000 barrels per day (bbl/d) to the U.S. in 2018, and replacing that volume with supplies from Canada and Mexico is more costly.

The long-term scenario could be much brighter, with a stable government led by Guaidó enjoying friendly relations throughout the hemisphere and the likelihood of restoring much of the 67% of oil production lost since President Hugo Chávez took power in 1999, James Williams, energy economist at WTRG Economics, told MarketWatch. That could lead to lucrative opportunities for U.S. companies to assist Petróleos de Venezuela S.A. (PDVSA) in rebuilding its energy infrastructure.

But the sunny outlook is not a sure thing. Fast-moving developments have put Guaido’s life at risk, Williams said, and war is not out of the question.

But the sunny outlook is not a sure thing. Fast-moving developments have put Guaido’s life at risk, Williams said, and war is not out of the question.

The immediate impact on oil prices was muted. Global benchmark Brent dropped 35 cents per barrel (bbl) on Jan. 23 and U.S. benchmark West Texas Intermediate (WTI) was down 39 cents/bbl. Venezuela’s shipments to the U.S. have declined in recent years and PDVSA has pivoted to markets in Asia.

However, it is the wobbling Asian economies, notably China and Japan, that worry traders. Both of those countries announced fiscal stimulus programs to bolster their slowing economies and the prospect of economic doldrums in Asia far outweighed the loss of Venezuelan crude, as far as the markets were concerned.

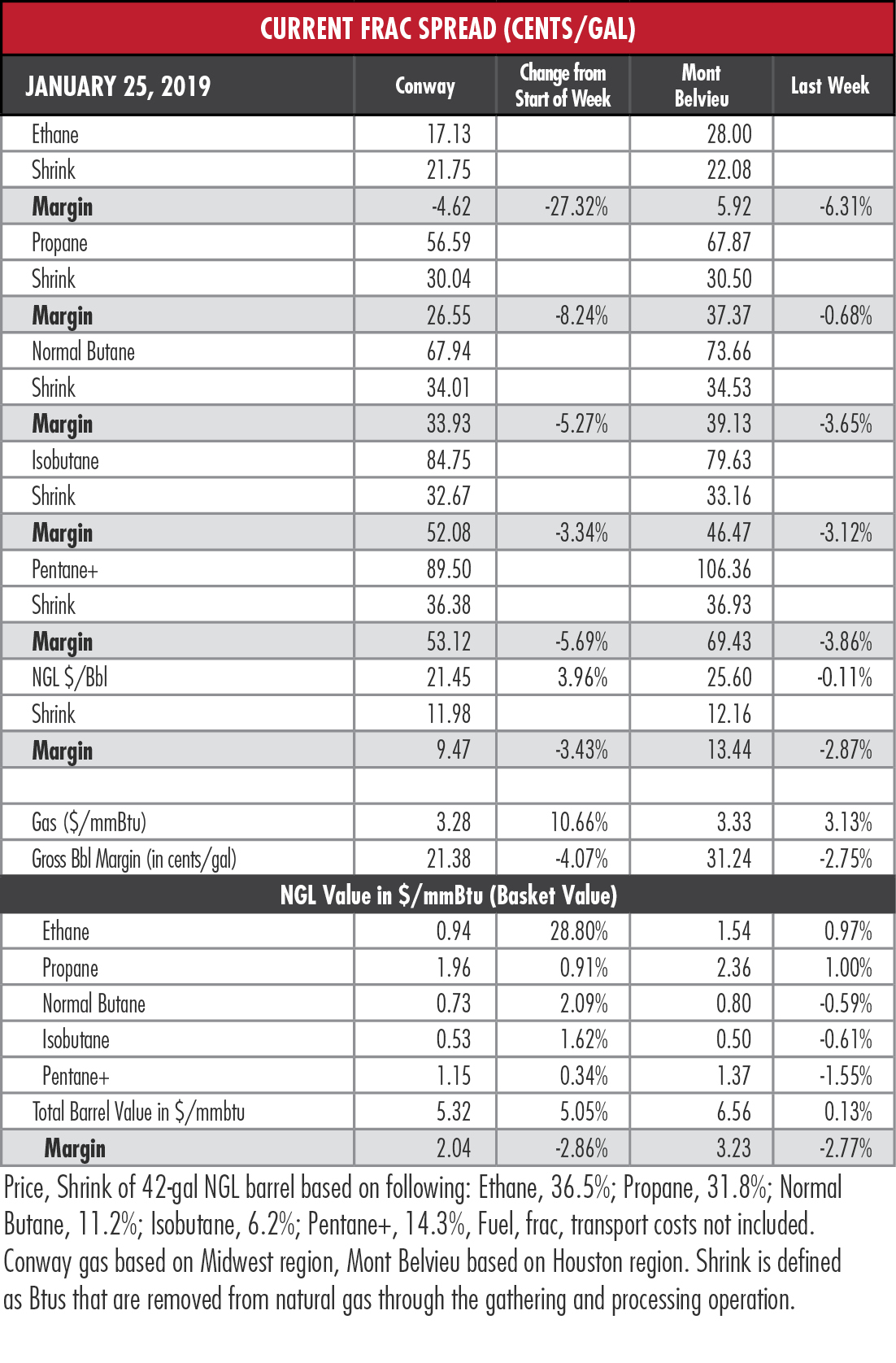

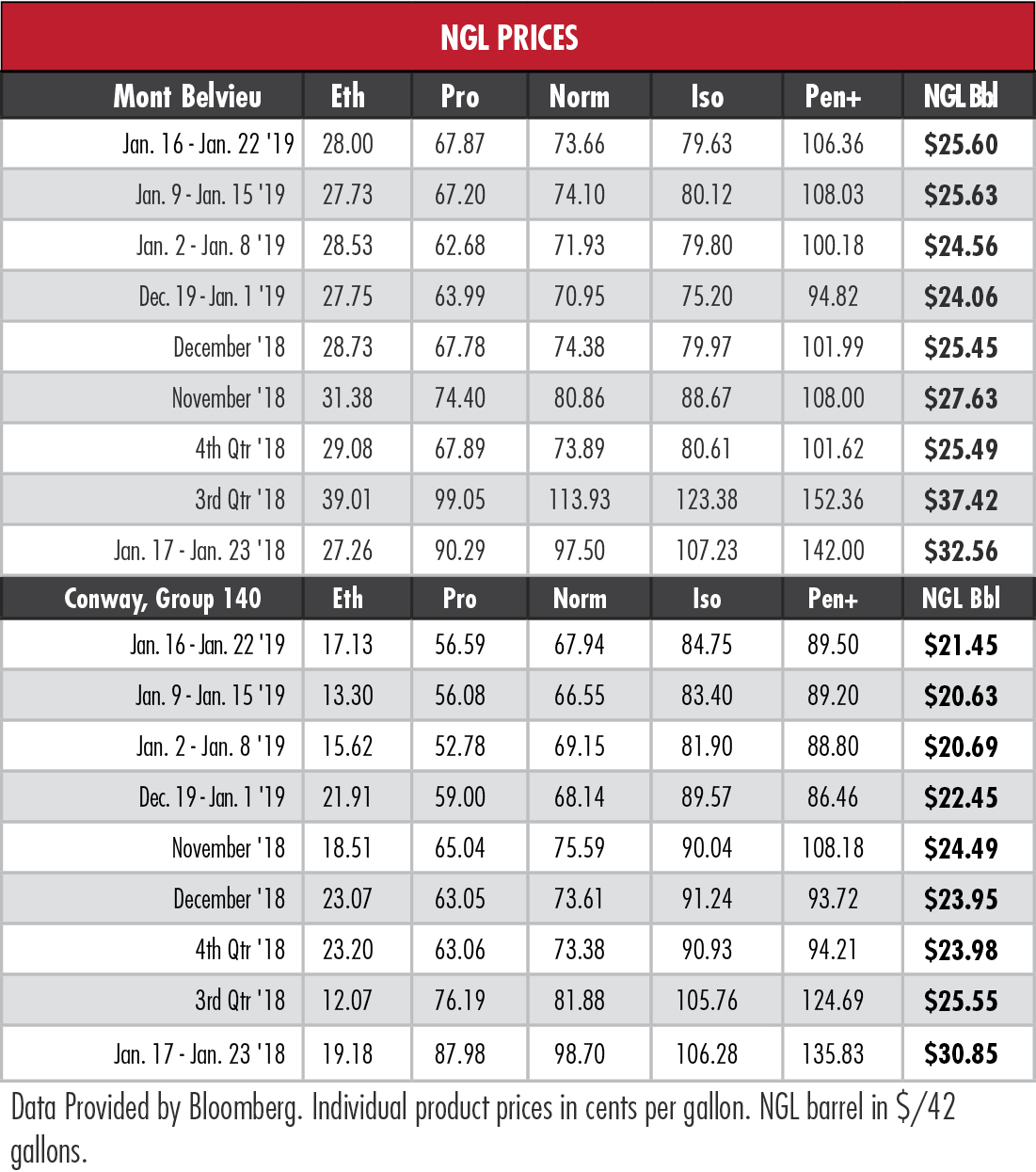

NGL prices held fairly steady but margins tightened across the board in the holiday-shortened four-day week. C5+ at Mont Belvieu, Texas, dipped by 1.67 cents per gallon (gal) but the rest of Mont Belvieu NGL stayed within a 1 cent/gal range and the hypothetical barrel lost only 3 cents.

In the week ended Jan. 18, storage of natural gas in the Lower 48 experienced a decrease of 163 billion cubic feet (Bcf), the U.S. Energy Information Administration reported. The figure resulted in a total of 2.37 trillion cubic feet (Tcf). That is 1.4% below the 2.337 Tcf figure at the same time in 2018 and 11.4% below the five-year average of 2.675 Tcf.

In the week ended Jan. 18, storage of natural gas in the Lower 48 experienced a decrease of 163 billion cubic feet (Bcf), the U.S. Energy Information Administration reported. The figure resulted in a total of 2.37 trillion cubic feet (Tcf). That is 1.4% below the 2.337 Tcf figure at the same time in 2018 and 11.4% below the five-year average of 2.675 Tcf.

Joseph Markman can be reached at jmarkman@hartenergy.com or @JHMarkman.

Recommended Reading

Nigeria Halts Shell Asset Sale, Approves Exxon-Seplat Deal

2024-10-21 - Nigeria blocked Shell's sale of its entire onshore and shallow-water oil operations.

Norway's Massive Johan Sverdrup Oilfield Shut by Power Outage

2024-11-18 - Norway's Equinor has halted output from its Johan Sverdrup oilfield, western Europe's largest, due to an onshore power outage, the company said on Nov. 18.

Wildcatting is Back: The New Lower 48 Oil Plays

2024-12-15 - Operators wanting to grow oil inventory organically are finding promising potential as modern drilling and completion costs have dropped while adding inventory via M&A is increasingly costly.

Baker Hughes: US Drillers Keep Oil, NatGas Rigs Unchanged for Second Week

2024-12-20 - U.S. energy firms this week kept the number of oil and natural gas rigs unchanged for the second week in a row.

Baker Hughes: US Oil, Gas Rig Count Steady This Week, Down Two in October

2024-10-25 - U.S. energy firms kept the number of oil and natural gas rigs unchanged this week.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.