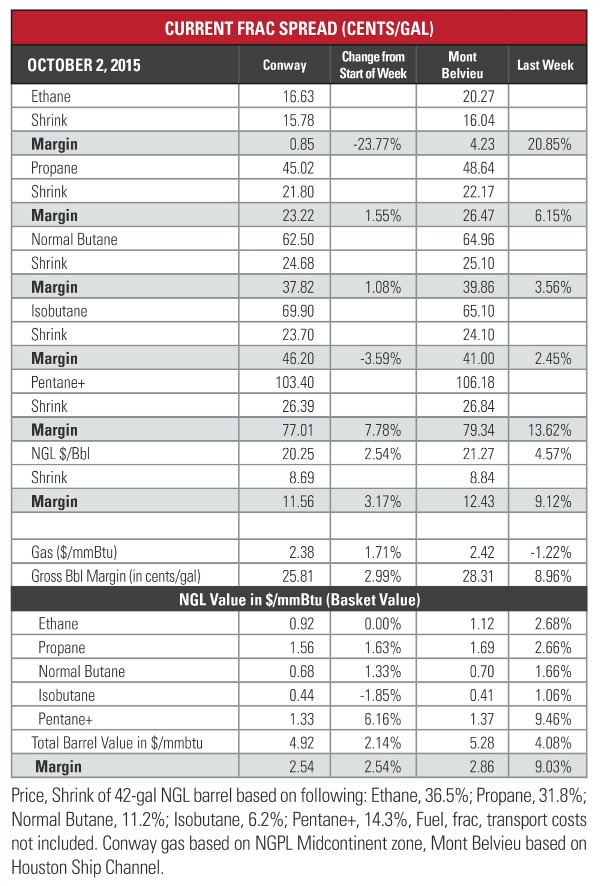

NGL prices benefitted from a near three-month high in West Texas Intermediate (WTI) crude and colder fall temperatures that increased heating demand. This resulted in the theoretical NGL barrel (bbl) improving 5% at Mont Belvieu and 3% at Conway.

However, several challenges to a price rally remain: WTI prices followed its run to more than $50/bbl by losing nearly $5/bbl in the next two days; and there is still an enormous supply overhang across the board for crude, liquids and gas.

This storage could get worked off pretty quickly with a cold winter, but like so much of the outlook for hydrocarbons this view is a motley mixture. Weather forecasts previously anticipated normalized winter temperatures, but the latest data is indicating a very strong El Niño this season.

Rather than provide clarity, this latest forecast further muddied the prognosis for winter heating demand as there is uncertainty of how the El Nino season will impact temperatures throughout the U.S. It is expected that the Northeast and Midwest will experience warmer-than-normal seasons, there could be heavier storms in each region if precipitation and cold air masses hit at the same time.

What is known is that this El Nino is expected to be the strongest since 1997. “Whether El Niño gets slightly stronger or a little weaker is not statistically significant now. This baby is too big to fail. Over North America, this winter will definitely not be normal. However, the climatic events of the past decade make normal difficult to define,” William Patzert, a research climatologist at NASA’s Jet Propulsion Laboratory, said in a news release.

While there is certainty that heating demand will increase once winter arrives, it is unknown how much demand there will be this season. Should major demand centers like the Northeast and Midwest experience colder-than-normal temperatures for a sustained period or if there a number of large storms that run through these regions, then gas and propane demand will increase. On the flip side, should temperatures be moderate with little storm activity then it is likely that demand will be more muted.

The biggest concern for the industry isn’t winter heating demand per se, but how much of a storage overhang will be left in the spring shoulder season following winter heating season. A large overhang will limit how large prices can rally while a smaller overhang could help create a price recovery.

This past week was definitely a good sign for the industry with NGL prices up at both hubs, but it also highlighted that WTI prices are still having a notable impact on liquids prices. This is obviously a positive when crude is trading at $80+/bbl, but decidedly less so when prices are under $50/bbl as they are now.

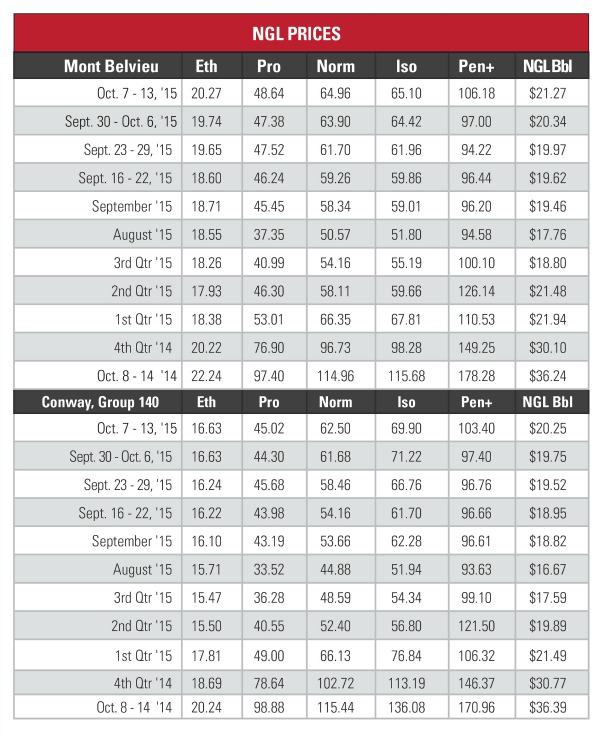

Interestingly, the biggest gains at Mont Belvieu were at the opposite ends of the NGL bbl with the lightest NGL, ethane, climbing to its highest price for the year while the heaviest NGL, C5+, rose to its highest level since mid-July. The situation was a bit different at the Conway hub as C5+ hit its highest price since late July, but ethane was flat as the Mid-Continent doesn’t have the same end-use market access as does Mont Belvieu. Frac spread margins were largely up at both hubs, with only Conway ethane and isobutane margins falling due to the increase in natural gas prices.

The most profitable NGL to make at both hubs was C5+ at 77 cents per gallon (/gal) at Conway and 79 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 46 cents/gal at Conway and 41 cents/gal at Mont Belvieu; butane at 38 cents/gal at Conway and 40 cents/gal at Mont Belvieu; propane at 23 cents/gal at Conway and 27 cents/gal at Mont Belvieu; and ethane at 1 cent/gal at Conway and 4 cents/gal at Mont Belvieu.

Natural gas storage injections were still high the week of Oct. 9, the most recent data available from the U.S. Energy Information Administration. The agency reported that storage increased by 100 billion cubic feet to 3.733 trillion cubic feet (Tcf) from 3.633 Tcf the previous week. This was 14% greater than the 3.286 Tcf posted last year at the same time and 5% greater than the five-year average of 3.565 Tcf.

Recommended Reading

E&P Consolidation Ripples Through Energy Finance Providers

2024-11-27 - Panel: The pool of financial companies catering to oil and gas companies has shrunk along with the number of E&Ps.

Utica Oil E&P Infinity Natural Resources’ IPO Gains 7 More Bankers

2024-11-27 - Infinity Natural Resources’ IPO is expected to provide a first-look at the public market’s valuation of the Utica oil play.

New Fortress Makes Headway on $2.7B Debt Refinancing

2024-11-26 - New Fortress Energy Inc. anticipates raising approximately $325 million in gross proceeds through the refinancing.

Equinor Exercises Option for Three Havila Vessels

2024-11-26 - Equinor ASA uses the vessels to support its North Atlantic, North Sea platforms.

California Resources Names Crespy as Executive VP, CFO

2024-11-26 - Clio C. Crespy has worked on some of California Resources’ “most significant” projects, including the Carbon TerraVault joint venture and the direct air capture hub at Elk Hills, said CEO Francisco Leon.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.