West Texas Intermediate (WTI) crude oil continued to improve the week of April 22 as its price was just under $60 per barrel (bbl). This was a result of storage declining at the Cushing, Okla., hub with increasing refinery runs that hit 95% last week.

This situation is expected to continue according to Global Hunter Securities. “Assuming refinery outages remain low and assuming Bakken and Canadian inflows are moderately lower, then Cushing should continue to signal gradually lower oil inventories,” the investment firm said in an April 30 research note.

Since Cushing plays such an important role in the U.S. crude market, working the big storage off at the hub would have a very positive impact on the market. However, there are still weak fundamentals at play that make a price recovery difficult.

Barclays Capital noted that given record high storage levels, low spare capacity won’t be able to have as positive an impact on prices as it did in 2007. Though Barclays is maintaining a more bearish outlook, the firm did raise its price deck by $8 based on unrest in the Middle East, new outages that are on par with levels last May when prices were $109/bbl and lower U.S. gas prices.

While prices aren’t far from meeting the level needed to hit Barclays’ demand scenario, volatility is still expected. “WTI must average in the mid-$60s next year in order for U.S. tight oil to show net growth sufficient to meet our demand forecast. In the meantime, we think the market is set to fluctuate between two poles: $75 and $55 Brent. In this environment, we expect the oil price to remain volatile and eventually gravitate towards $75/bbl by late 2016,” the investment firm said in an April 28 research note.

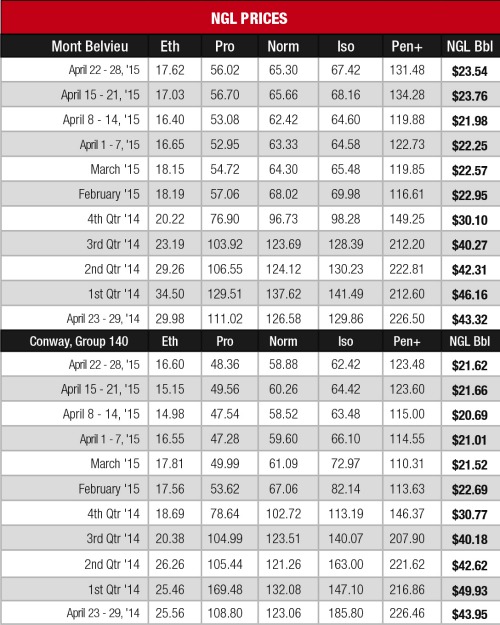

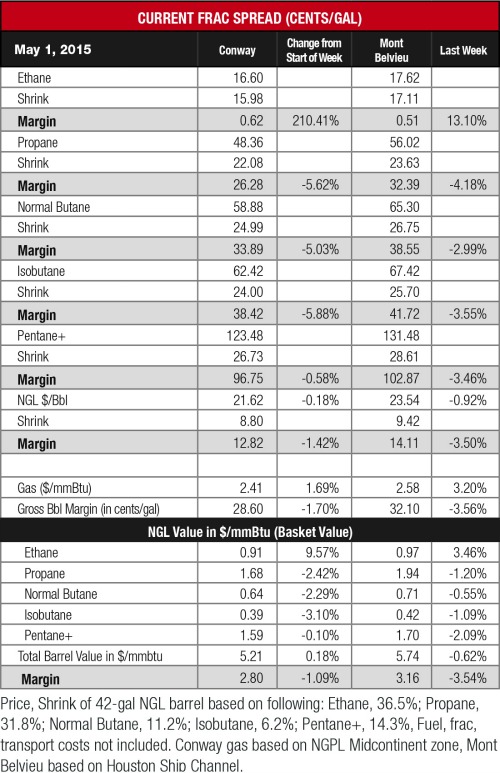

Surprisingly the uptick in WTI crude didn’t have a correlative effect on liquids prices as heavy NGL prices were down at both hubs as the market is well balanced after the large gains posted the previous week. Frac spread margins for heavy NGL was also down this week as gas prices posted gains while power generation demand is up this year with lower prices. The Conway price for natural gas rose 2% to $2.41 per million Btu (MMBtu) and the Mont Belvieu price improved 3% to $2.58/MMBtu.

Propane prices followed the lead of heavy NGL prices as they fell at both hubs due to storage levels remaining extremely high and growing as stocks rose by just under 2 MMbbl last week. According to PIRA Energy Group, propane storage levels are 57.5 MMbbl, or 31 MMbbl higher than last year at the same time.

Ethane was the lone bright spot for NGL prices this week as the product posted gains at both hubs. The Mont Belvieu price was up 3% to 18 cents per gallon (gal), its highest price since the week of March 18 when it was also 18 cents/gal. The Conway price rose 10% to 17 cents/gal, the hub’s highest price since it was 18 cents/gal the final week of March.

The theoretical NGL bbl price was down very slightly at Conway to $21.62/bbl with a 2% decline in margin to $12.82/bbl while the Mont Belvieu price fell 1% to $23.54/bbl with a 4% drop in margin to $14.11/bbl.

The most profitable NGL to make at both hubs was C5+ at 97 cents/gal at Conway and $1.03/gal at Mont Belvieu. This was followed, in order, by isobutane at 38 cents/gal at Conway and 42 cents/gal at Mont Belvieu; butane at 34 cents/gal at Conway and 39 cents/gal at Mont Belvieu; propane at 26 cents/gal at Conway and 32 cents/gal at Mont Belvieu; and ethane at 1 cent/gal at both hubs.

The U.S. Energy Information Administration reported that natural gas storage injections were 81 billion cubic feet (Bcf) to 1.71 trillion cubic feet (Tcf) the week of April 24 from 1.629 Tcf the previous week. This was 77% higher than the 969 Bcf posted last year at the same time and 4% lower than the five-year average of 1.785 Tcf.

Cooling demand should increase the first week of May as the National Weather Service is forecasting warmer-than-normal temperatures along both the East and West coasts as well as much of the Midwest and the Gulf Coast.

Contact the author, Frank Nieto, at fnieto@hartenergy.com.

Recommended Reading

Mach Natural Resources Closes Two Midcontinent Deals

2024-10-03 - Mach purchased assets in the Anadarko and Ardmore basins for a total consideration of $136 million.

Macquarie Buys Up to $1.73B Stake in D.E. Shaw Renewable Investments

2024-09-24 - Macquarie Asset Management is acquiring a minority stake in D.E. Shaw Renewable Investments in an equity investment of up to $1.73 billion.

SCF Partners Acquires Newpark Fluid Systems

2024-09-16 - SCF Partners acquired Newpark Fluid Systems, an oil and gas and geothermal fluids solution business, from Newpark Resources, for a base price of $127.5 million.

Blackstone in Talks to Buy US Pipeline Stakes from EQT for $3.5B, Sources Say

2024-10-28 - If the talks are successful, the deal would help natural gas producer EQT slash the debt pile it accumulated from its acquisition of pipeline operator Equitrans Midstream earlier this year.

Methanex to Buy OCI Global’s Methanol Business in $2.05B Deal

2024-09-10 - The agreement includes OCI Global’s stake in two methanol production facilities in Beaumont, Texas.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.