Before an asset class matures and stabilizes, it is labeled “emerging” and is characterized by exceptional growth and ineffi ciencies. For MLPs, many of the original causes of ineffi ciencies have been resolved by media attention and the creation of a plethora of investment products. Given that evolution, and since slowing or plateauing growth can be a characteristic of a maturing asset class, we examined distribution growth to determine whether MLPs remain an emerging class or have matured.

We measured annual distribution growth based on MLPs that pay a traditional distribution, have been trading for two full calendar years and are not general partners (GPs). Regrettably, this unavoidably introduced survivorship bias, as in hard times an MLP often will be acquired.

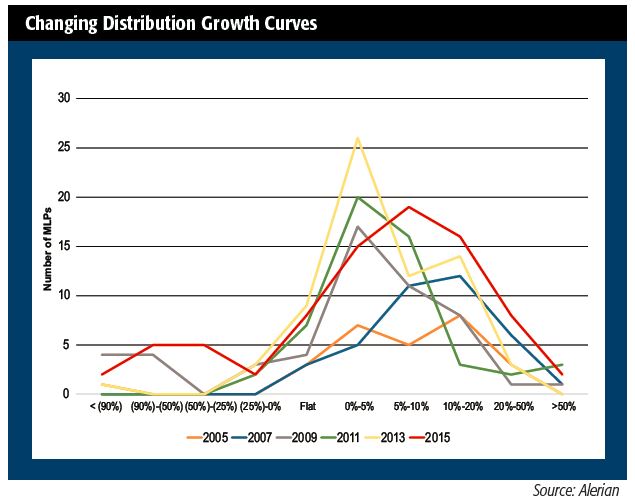

To explain a few of the accompanying histogram’s categories: A cut of 90% or more often represents a complete elimination of the distribution; 10% to 20% growth can occasionally be maintained for several years for a high-growth MLP; 20% to 50% growth generally results from a transformative transaction; and growth of more than 50% most often indicates an MLP reinstating a distribution, or it could be an exceptionally generous GP. For simplicity, the histogram only displays every other year.

In the early years, distribution cuts were exceptionally rare, and a plurality of MLPs grew their distributions in the 10% to 20% range. An MLP was considerably more likely to grow its distribution by upward of 20% than it was to cut it.

Starting with 2009, the majority of MLPs raised their distributions by less than 5% each year. Of course, the two most diffi cult years, 2009 and 2015, also saw the most cuts.

Around 2012, as the number of MLPs grew, the bell curve started to disappear. In 2012 and 2013, raising distributions by 5% or less, or by 10% to 20%, was common. The chart shows two peaks, and the bestfi t line actually looks like a great sledding hill. Some MLPs have matured and now grow distributions in the stately low single digits, while other, recently formed MLPs are still experiencing new, early and high growth.

By 2015, the tail risk is much fatter. In fact, as the number and variety of MLPs grows, so does the variety of distribution growth numbers.

Taken as a whole, the weighted average distribution growth has fallen, the histogram peak has shifted to the left, and the diversity of distribution growths all speak to an asset class that, at least in terms of its distribution growth, has been maturing.

With an emerging asset class, picking a winner is often as simple as a children’s balloon dart game at a carnival: Everyone wins! Investors may not be able to expect standard double-digit distribution growth from MLPs anymore (at least not without a strong GP or aggressive appetite for M&A). More and more MLPs are keeping distributions fl at, which doesn’t mean that it’s impossible to pick a winner, only that—unlike 10 years ago—it’s harder.

Recommended Reading

Norway's Massive Johan Sverdrup Oilfield Shut by Power Outage

2024-11-18 - Norway's Equinor has halted output from its Johan Sverdrup oilfield, western Europe's largest, due to an onshore power outage, the company said on Nov. 18.

Classic Rock, New Wells: Permian Conventional Zones Gain Momentum

2024-12-02 - Spurned or simply ignored by the big publics, the Permian Basin’s conventional zones—the Central Basin Platform, Northwest Shelf and Eastern Shelf—remain playgrounds for independent producers.

First Helium Plans Drilling of Two Oil Targets in Alberta

2024-11-29 - First Helium Inc. has identified 10 other sites in the Leduc formation.

DNO Discovers Oil in New Play Offshore Norway

2024-12-02 - DNO ASA estimated gross recoverable resources in the range of 27 MMboe to 57 MMboe.

Freshly Public New Era Touts Net-Zero NatGas Permian Data Centers

2024-12-11 - New Era Helium and Sharon AI have signed a letter of intent for a joint venture to develop and operate a 250-megawatt data center in the Permian Basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.