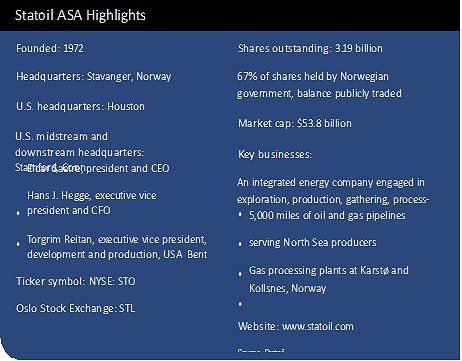

Publicly traded Statoil ASA, with a world player-sized enterprise value of $64 billion, is an integrated oil and gas firm with operations in 37 countries. That’s a far cry from the domestically focused, state-owned oil company Norway’s parliament founded in 1972 as the North Sea emerged as a major producing area. Those far-flung operations include a significant operating presence in three of North America’s biggest unconventional plays—the Bakken, Marcellus and Eagle Ford—with nearly 1 million net acres under lease and combined production of more than 200,000 barrels of oil equivalent per day. Statoil relies on sizeable in-house and third-party midstream assets to sustain its U.S. production.

Bent Pedersen, a Statoil veteran executive, had assignments around the world before transferring to North America. He currently oversees the firm’s U.S. midstream assets from Statoil’s U.S. office in Stamford, Conn. He discussed with Midstream Business how this nation’s midstream sector differs from foreign midstream operations and how Statoil’s long-term business values provide a key to its continuing success.

MIDSTREAM Your background gives you an international perspective on the oil and gas business. What roles did you hold at Statoil before assuming your current position in its North American operations?

PEDERSEN I think I could spend most of the interview on my career! I’ve been with Statoil for 35 years, and I have worked in all parts of our midstream and downstream businesses, everything from the retail consumer and industrial market, back through the value chain into refining, trading, shipping and logistics.

Basically, I would say what is important for holding a position in the North American midstream market is to have the commercial and logistics background—the value chain background, because I think that those are the two important elements, logistics and commercial.

MIDSTREAM Statoil has emerged as a leading Bakken producer—with significant midstream assets—following its 2011 acquisition of Brigham Exploration. How does your Williston Basin asset fit into the company’s worldwide development plan?

PEDERSEN Statoil started its international expansion quite some years back, acknowledging that the Norwegian continental shelf, at that point in time, was in decline. Since then, we have had some new projects in Norway and extended the lifetime of the Norwegian continental shelf. But we saw that we needed to go international to maintain our portfolio and the U.S. is, in that context, a very interesting market—including the Bakken area.

It’s a transparent market. It’s a market where you can compete on equal terms. Whereas in some other countries, the business conditions are more challenging; different regimes you operate in.

MIDSTREAM Your firm also holds acreage in the Eagle Ford and Marcellus. How do these unconventional plays differ for you from the Bakken from a midstream perspective?

PEDERSEN Our positions in the three plays are very different, they are very much legacy driven. When we bought into the Marcellus, we bought into a partnership with Chesapeake Energy in 2008. That was an already established play, so a lot of the midstream solutions we have there are legacy assets from back then.

In the Eagle Ford, likewise, we bought into a partnership with Talisman Energy. In the initial phase, Talisman was the operator and then we took over operatorship of 50% of the asset in 2013. That means our midstream position is very much based upon the legacy of these assets. To the same extent in the Bakken, we bought the Brigham Exploration assets, including an already established midstream portfolio.

In the Marcellus, our midstream is primarily based upon use of a third party for gathering and processing. In the Eagle Ford, we have our own gathering and processing—and also use third parties—and in the Bakken our midstream is primarily Statoil-owned and -operated assets.

MIDSTREAM Statoil has a growing role in the U.S. natural gas transportation business. How do you see the midstream changing as the gas market changes?

PEDERSEN Some of the areas we are in—and this applies not only to gas, it applies to oil as well—specifically Marcellus and Bakken, the resource, the gas and the oil, is not exactly in a demand center. So with the growth of these assets, we have seen that one of the big challenges is to get this production to market. That’s where our midstream organization plays a very important role. We have two roles—one is flow assurance, making sure that we don’t have to shut down production, that we can gather the gas and the oil. And the second role is to get the production to the best markets—the value uplift role—so we’re not just gathering it, but also ensuring that we get it to the most attractive market. And we have done both in the Marcellus, Bakken and in Eagle Ford.

MIDSTREAM What can North American’s midstream sector learn from overseas gathering, processing and transportation operators?

PEDERSEN That’s a very difficult question because the U.S. is so different, and I think that’s one learning experience we have had in trying to establish ourselves in the U.S. onshore. The difference between operating offshore and onshore is huge. The U.S. onshore is a very, very dynamic play. Look at the number of wells we drill during a year and compare that with what we drill offshore. We must be able to move quickly in such a dynamic environment. This has been a big learning experience for us. But we have—luckily—been a quick learner, a quick adapter.

What we primarily can learn from our operations and bring with us here is our approach to safety, our approach to sustainable, efficient operations, and adapt some of these procedures to the more dynamic U.S. onshore environment.

MIDSTREAM To turn that question around, what can foreign midstream operators learn from their counterparts in this nation?

PEDERSEN I think that the dynamics here, the speed at which you have to make decisions, are something that we could take with us back to our other operations. But we have to acknowledge, it is very different operation overseas. Here, we lay gathering pipelines every day. In the North Sea, you lay one pipe to market. So offshore vs. onshore is very different.

MIDSTREAM You touched on the importance of safety and sustainability, but overall, how would you view Statoil’s management style? How does your management style differ from, say, the typical U.S.-based energy firm?

PEDERSEN When we talk about management style, we have a philosophy of being a very open, hands-on company. We have a Norwegian heritage, meaning that we have a very open style—not only in theory. So I think that we don’t have the same hierarchy as you find in many other companies.

We have a very firm belief in safe operations; we don’t accept that we should have incidents. We have a zero-target philosophy when it comes to incidents and we want to learn. When incidents happen, one of the most important things is not to punish people but learn from the incident so we can avoid it happening again. As an example of our safety focus, we were an early mover on implementing the anticipated new DOT [U.S. Department of Transportation] rules for rail cars. We actually ordered this type of cars before the DOT issued their rule earlier this year.

When it comes to sustainability, we have very stringent targets on emissions and a high environmental consciousness. We try to deliver better on these targets than what, necessarily, the legislation requires.

MIDSTREAM What do you see as Statoil’s biggest challenge to doing business in the U.S?

PEDERSEN We are adapting to the dynamic environment and making sure that we have the governance in which to operate, to ensure that we can move swiftly and be agile. That has been our biggest challenge, and we can still improve in that area.

MIDSTREAM How would you describe Statoil’s long-term role in the North American midstream?

PEDERSEN I will highlight that we are not a traditional midstream company, we are not an independent midstream company. Our primary reason for being in midstream is to support our upstream operations. That has two dimensions—it’s the flow assurance, and it’s the value uplift.

When I talk about value uplift, I would like to give a couple examples of what we have done. We have secured transport capacity from the Marcellus area to New York City and we have secured transport capacity to Toronto in Canada. Our aim is securing the highest-possible value for our production.

Likewise, we were very early movers in the Bakken area in securing rail capacity, acknowledging that there was not sufficient pipeline capacity, again thereby securing that we could get our production to the best-paying markets. The advantage with rail—compared with pipe especially—is that if the market moves, you move with the market. You can’t do that with a pipeline—it goes only from A to B. Those are two examples of what we have been doing to strengthen Statoil’s total portfolio in the U.S. market.

Recommended Reading

PE Firm Hy24 Commits $50MM to StormFisher Hydrogen

2025-02-11 - The funding, made via Hy24’s Clean Hydrogen Infrastructure Fund, will go toward StormFisher Hydrogen’s efforts to produce clean fuel in North America.

Plug Power CEO Sees Hydrogen as Part of US Energy Dominance

2025-01-29 - Plug Power CEO Andy Marsh says the U.S., with renewable energy resources, should be the world’s leading exporter of hydrogen as it competes globally, including with China.

Baker Hughes CEO: Expect ‘Volatility, Noise’ Around Energy Transition

2025-03-12 - Baker Hughes and Linde executives spoke about lower carbon resources such as hydrogen and geothermal, which will be part of the energy mix but unlikely to displace natural gas.

Infinium, Summit Carbon Solutions Join Forces to Advance Efuels

2025-02-05 - Infinium will supply up to 670,000 metric tons of CO2 to Summit Carbon at a eFuels facility.

Energy Transition in Motion (Week of Feb. 14, 2025)

2025-02-14 - Here is a look at some of this week’s renewable energy news, including a geothermal drilling partnership.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.