Results of the most recent Baird Energy Survey conducted in September, the sixth consecutive such quarterly survey, have provided some key takeaways for investors, E&Ps and the energy financing community. Baird asks recipients of one of its daily emails to participate in its survey. Of the 133 participants responding in full, 52 were buyside investors, 69 were energy industry contacts and 12 placed themselves in the “other” category. The survey includes 11 recurring questions focused on industry sentiment, commodity price expectations and investment preferences, with a handful of more topical questions about recent trends.

The respondents have minimal conviction in near-term commodity price movements. Recent trading volatility in crude and natural gas has left market participants decidedly mixed on future trends. This murky macro backdrop is acting as a headwind for the E&P group as a whole, with stock-picking based solely on company-specific fundamentals coupled with identifiable catalysts.

Key industry themes worth monitoring include new drilling and completion techniques, downspacing/interval drilling, political developments, oilfield services costs, and volatile basis differentials driven by infrastructure tightness.

Commodity headwinds

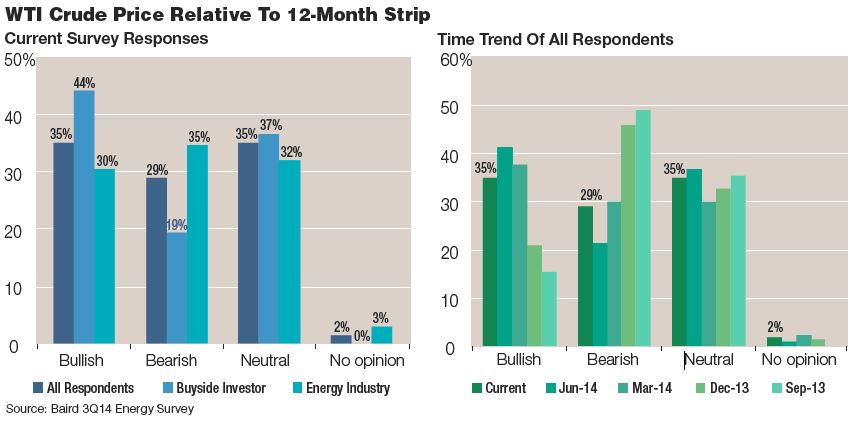

For crude oil, near-term trading trends are uncertain. Survey responses are increasingly mixed on the near-term outlook for crude as WTI breaks the $85 per barrel (bbl) psychological level and Brent trades in the sub-$90/bbl range, down 21% and 22%, respectively, from June highs.

Over the past year, crude prices ignored fundamental global supply/demand economics and remained elevated, due in large part to ongoing geopolitical rifts that injected an increased risk premium into the commodity. While geopolitical tensions remain high in key oil-producing regions (Middle East, North Africa), the muted impact on crude supply to date has the market refocusing its attention on the global oversupply dynamic driven by North American production growth and increasing OPEC output, coupled with relatively stagnant global demand.

Energy industry respondents are more bearish on crude near term, because they are keyed in on the increasing oversupply dynamic. Buyside investors are more optimistic on prices, potentially due to trading technicals and recent geopolitical sentiment trends. While this optimism could provide a near-term tailwind for E&P trading (yet to be seen), we are more bearish on the commodity long-term and think that the equilibrium prices will settle in the mid-$80/bbl range over the coming years as the supply/demand imbalance is exacerbated.

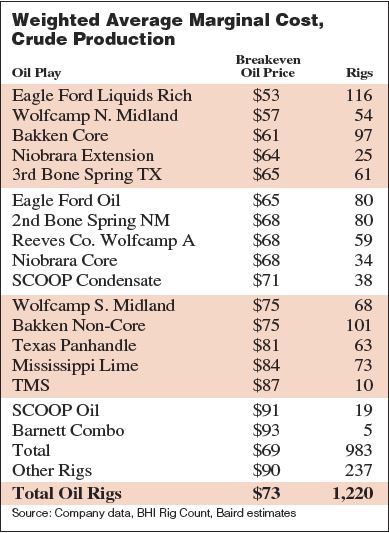

Crude’s marginal cost of production still points to solid returns. With recent crude price weakness, questions arise as to when producers will scale back drilling and reduce capital budgets. To provide a more quantitative answer, we looked at breakeven oil prices (20% IRR) across major onshore plays and compared them to current play/county rig allocation as provided by Baker Hughes. As highlighted in the table above, the weighted average marginal cost of crude production in the U.S. onshore is about $73/bbl currently, with core plays exhibiting a modestly lower marginal cost of some $70/bbl, consistent with our prior thinking.

All in, economics are still robust, with WTI at $85/bbl. We expect producers to evaluate capital budgets if crude drops and stays below $85/bbl, with budget cuts and slowed activity likely coming on a sustained pullback in the sub-$80/bbl range. Not surprisingly, Bakken producers would be the first of the major plays to slow activity given it has the highest average marginal cost of production (noncore $70-$80/bbl), while the Permian and Eagle Ford are insulated a bit more with marginal costs of $60-$70/bbl.

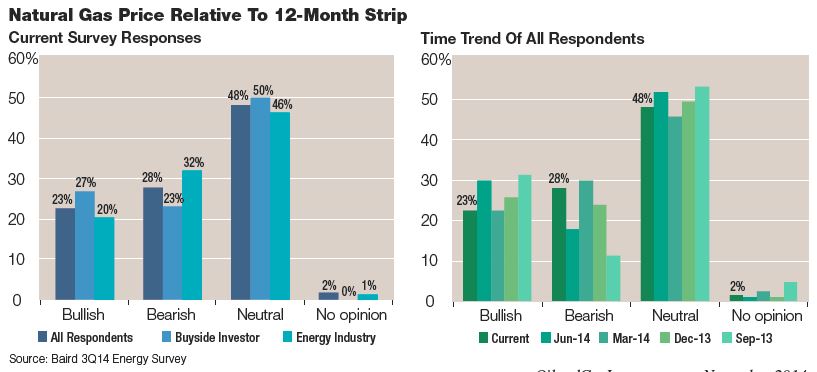

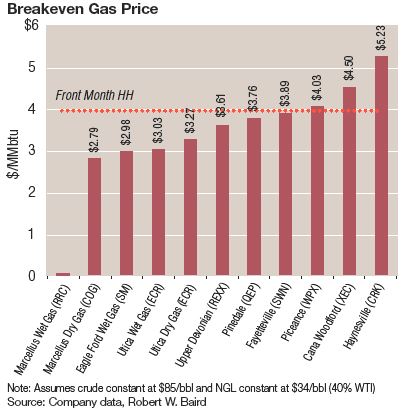

For natural gas, range-bound trading results in a neutral outlook. Not surprisingly, the outlook for natural gas remains neutral, driven in large part by range-bound trading from July through September in the $3.50 to $4/MMBtu range, coupled with minimal expected price appreciation over the longer term. Survey respondents peg the natural gas long-term (five-year) equilibrium price at $4 to $4.50/MMBtu, meaning limited upside from current levels. Until new natural gas demand outlets come to fruition, later this decade (meaningful LNG in 2018 and beyond), sustained price rallies are likely limited and driven by more transitory factors.

The industry is marginally more bearish than the buyside on natural gas, likely because of growing supply concerns as increased well productivity drives record output from Appalachia. Increasing prospective dry gas drilling inventory is also a concern, with the Utica gas window emerging as another prolific option. The combination of ample supply, steady/low demand growth and low marginal cost (Marcellus less than $3/MMBtu) continues to curb our attraction to natural gas.

However, we are more favorable on the commodity near term (three months) as seasonal demand tailwinds move to the forefront and natural gas storage withdrawals begin, the major driver in last year’s winter price rally from early November lows. Winter weather is the next major catalyst that could cause natural gas to break out of its trading range, both to the upside or downside, as evidenced by the move, albeit temporary, above $4/MMBtu in early October.

Energy industry respondents are more bearish on crude near term, because they are keyed in on the increasing oversupply dynamic.

Basin economics drive capex

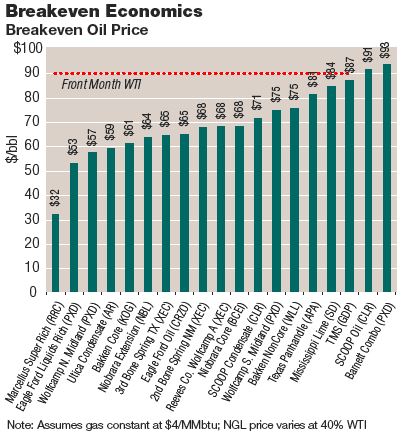

We updated our comprehensive well return and breakeven analysis (20% IRR) for revised type curves, well costs, price realizations and operating expenses. Our analysis covers 31 type curves spanning all of the major U.S. onshore plays, with each type curve based on corporate data but also generally representative of average returns for the area. As highlighted in the “Breakeven Economics” bar charts on this page, the results were generally consistent with expectations. Oilier plays offer higher returns at current commodity prices than gas, with the exception of the prolific Appalachian Basin. Top-returning basins include the Eagle Ford, Permian, Williston, Niobrara and Appalachia (both Marcellus and Utica), while less-prolific gas basins (Rockies, Haynesville, Barnett), high-cost plays (Mississippi Lime, Tuscaloosa Marine Shale) and more peripheral acreage in otherwise good basins rounded out the bottom of the return list.

The weighted average marginal cost of crude production in the U.S. onshore is about $73/bbl currently, with core plays exhibiting a modestly lower marginal cost.

Play preferences focused on oil

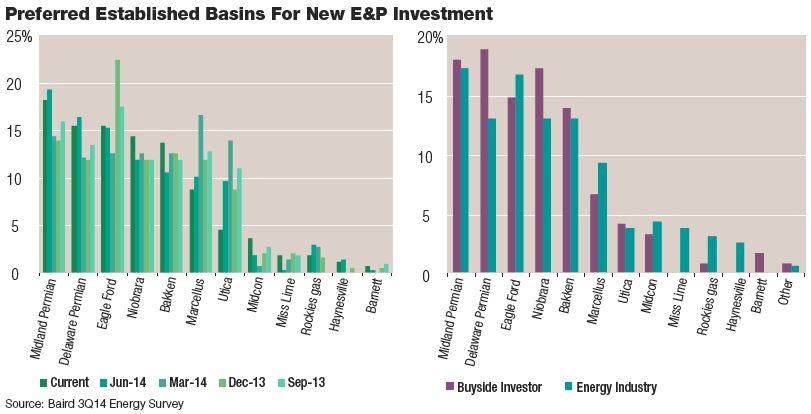

This breakeven analysis is consistent with play preferences and also corporate capital allocation decisions. The highest-returning basins are those where the majority of rigs are deployed and where E&P investment is occurring. According to the Baird Energy Survey, the Permian on the whole remains the preferred choice for E&P investment, though the buyside prefers the Delaware Basin, perhaps due to increased hype in conjunction with second-quarter 2014 earnings, while the industry prefers the more established Midland Basin. Eagle Ford preference remained relatively stable at No. 3 due to solid economics and lower relative breakeven price, while the Niobrara overtook the Bakken for No. 4 as crude softness weighed on Williston sentiment.

Constructive Niobrara well results and successful downspace/interval pilots are sentiment tailwinds currently, as well economics and the size of the play regularly ratchet higher. Marcellus and Utica attractiveness noticeably fell, probably due to persistent concerns surrounding Appalachian differentials as regional production continues to set records and outpace infrastructure additions.

Until new natural gas demand outlets come to fruition later this decade (meaningful LNG in 2018 and beyond), sustained price rallies are likely limited.

Near-term industry trends

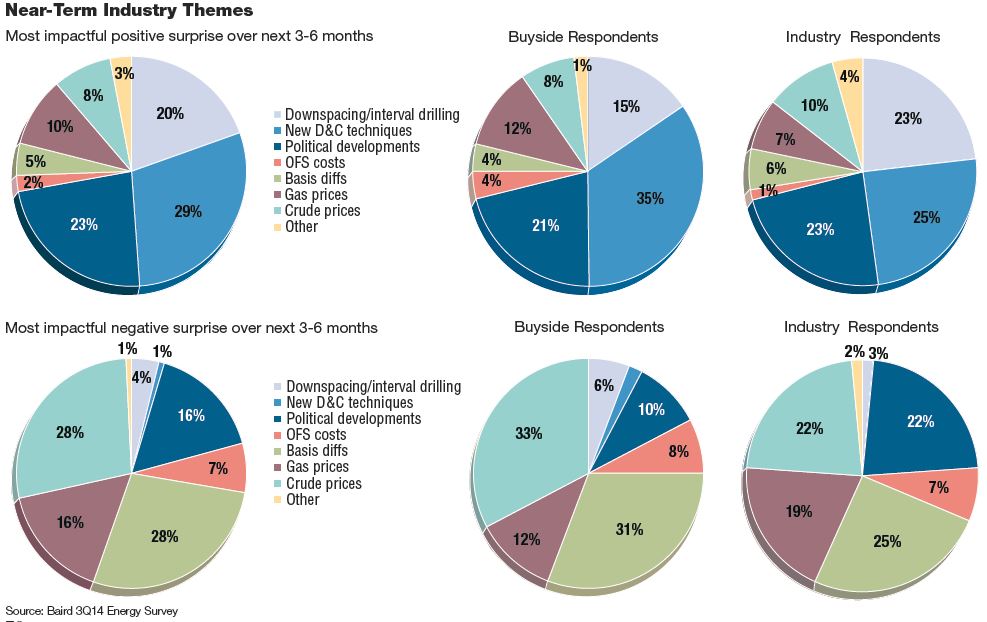

We asked survey respondents which current theme was likely to have the most impact, positive or negative, on the U.S. E&P industry over the next three to six months. As highlighted in the pie charts at the bottom of this page, no one item dominated responses. However, a few themes emerged: ongoing operating initiatives likely to provide positive news flow, uncertainty on the impact of potential political developments, and broad concern on commodity price realizations.

Oilier plays offer higher returns at current commodity prices than gas.

The Permian remains the preferred choice for E&P investment, although the buyside prefers the Delaware Basin.

E&Ps’ technology focus

Technology advancement is accelerating with state-of-the-art completion techniques evolving monthly as producers extend lateral lengths, increase fracturing stages and utilize more proppant. Ongoing declines in drilling times have enabled much of this incremental reinvestment in completion as producers accelerate and ultimately lift EURs. We increasingly see E&P firms referencing output from scanning electron microscopes and microseismic studies as data becomes increasingly paramount at both the field and well level. And, all this data is helping drive field- and well-specific completion planning, aided by tighter geosteering.

Downspacing and interval drilling still offer major upside potential in resource recoveries as all this technology brings more effective understanding, targeting and review of how best to pull hydrocarbons from many plays that hold stacked deposits.

Both political hope and angst are on the rise, as expectations simmer for material advancement in political negotiations to end, partially or wholly, the U.S. oil export ban after mid-term elections. At the same time, environmental regulations continue to grow as exemplified by the North Dakota Industrial Commission’s (NDIC) formal codification of flaring restrictions this summer. Still, participants are optimistic about their ability to navigate regulations, as illustrated by increasingly popular efforts to recycle and self-source water as a tool for both environmental stewardship and cost and risk management. Further, developments in the Ukraine over the summer underscore the geopolitical importance of the U.S.’ thriving upstream industry.

Expectations for foreign demand to bear profit-and-loss fruit are on the rise. With LNG exports closer to reality, gas shipments to Mexico set to ramp, and the prospects for removal of the U.S. export ban increasingly plausible, producers should see much of the intangible hype of international demand translated into increased realizations and volumes as 2015 progresses.

Respondents are watching operating initiatives likely to provide positive news flow, potential political developments and commodity price realizations.

Oilfield service costs

Oilfield cost increases are likely limited to rising input costs and logistical drivers. While survey respondents tended to lean toward increasing costs for oilfield services over the next three to six months, driven by the U.S. land stimulations market, we believe cost increases will be limited primarily to rising input costs and logistical drivers. We anticipate the emergence of underlying service capacity tailwinds over the next several quarters. It should come as no surprise that increases in sand usage per well, approaching 50% year-over-year, have resulted in supply chain frictions—immediately evident from a quick glance at the 75-plus rail cars worth of sand now required per job vs. the 20 rail cars just a year ago.

As we progress through contract rollovers in the coming months, the service companies will be keen to specify allowances for transport and raw material inflation, costs that had caught the group largely by surprise entering 2014. While the industry may see some relief as infrastructure investments across the major service providers reach critical mass, the potential for elevated logistical pressures remains through 2015, particularly on the escalation of West Texas sand intensities to levels of the more advanced plays driving the supply chain challenges today.

Horsepower additions likely provide cost tailwinds for E&Ps. At the same time, offsetting these challenges has been the characteristic nature of the services group as it relates to capital expansion, a dynamic we anticipate will likely emerge as an underlying service cost tailwind for the E&Ps. Upon the early hints of solidifying pressure pumping pricing exiting 2013, we began to see a trickle of horsepower capacity expansion announcements, initially limited to the small to mid-caps and smaller players but immediately joined by the large caps over first-half 2014.

By our count, the top 15 North American pressure pumping providers have announced nearly 2 million in incremental hydraulic horsepower additions for deployment in 2014-2015, with 2014 capacity rising by an estimated 8% year-over-year. Accordingly, we believe there are expectation risks for service providers and, in turn, potential for underlying tailwinds for E&Ps as these incremental fleets arrive, in the event that the forward trajectory of U.S. land drilling and completions activity falls below the pace of first-half 2014.

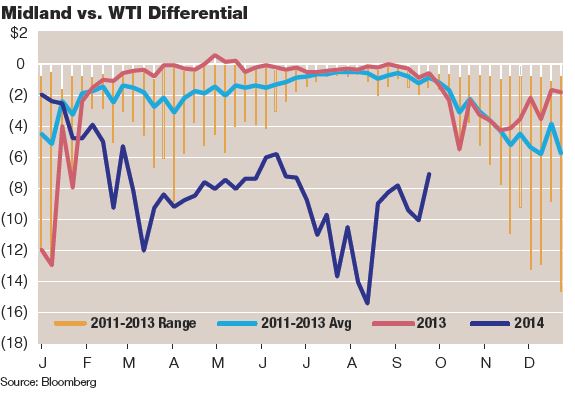

Permian differentials are also in focus as production out of the basin overwhelms takeaway capacity.

Midstream build-out, differentials

MLPs continue to benefit from the demand for yield products and strong equity fund inflows, which have grown at an 83% three-year CAGR. With equity financing costs nearing all-time lows and the Alerian MLP index hitting a 5.3% distribution yield, or 29% below the long-term average, MLPs are well equipped to fund oil and gas infrastructure, which should help reduce the volatility of oil and gas basis differentials over the long term. However, we expect realizations at these local price points to remain volatile over the coming quarters as MLPs try to keep pace with massive production growth out of the Permian, Bakken, Eagle Ford and Appalachia.

In the third quarter, the Bakken has been in the spotlight with Energy Transfer Partners, Enterprise Products Partners and ONEOK Partners announcing significant projects or expansions. In our view, the significant takeaway capacity expansion both via pipeline (40% CAGR in capacity through 2016) and rail (12% CAGR through 2016) should continue to reduce the correlation to the WTI/Brent spread and Bakken basis volatility.

Over time, we expect the spread to compress toward the regional transportation costs, given the ample takeaway capacity expectations relative to production levels. However, our discussions with crude-by-rail logistics providers lead us to believe that nameplate rail capacity likely overstates the actual effective capacity, given rail congestion problems. Hence, the continued utilization, expansion and construction of new rail terminals.

Permian differentials are also in focus as production out of the basin overwhelms takeaway capacity, resulting in a widening of differentials, which peaked at less than $21/bbl in mid-August. Differentials have compressed since then and are trading in the $7/bbl range vs. the 200-day moving average of about $8/bbl. We expect the production/infrastructure balance to remain tight over the coming years as drilling activity remains elevated, likely resulting in continued volatility in the Midland/WTI differential. Some short-term differential compression is likely, however, as BridgeTex Pipeline (300,000 bbl/d) volumes ramp from its late-September start-up.

Ethan H. Bellamy is senior research analyst, MLPs and U.S. royalty trusts, at Robert W. Baird & Co. Daniel Katzenberg is senior research analyst, E&P. Daniel R. Leben, CFA, is senior research analyst, oilfield services and equipment. Maggie Savage, CFA, is E&P research analyst. To receive Baird’s Daily Dirt energy e-mail and/or participate in future surveys, email CPlucinksi@rwbaird.com.

Robert W. Baird & Co. Inc. and/or its affiliates expect to receive or intend to seek investment banking related compensation from the company or companies mentioned in this article within the next three months. Baird may not be licensed to execute transactions in all foreign listed securities directly. Transactions in foreign listed securities may be prohibited for residents of the U.S. This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Baird prohibits analysts from owning stock in companies they cover. MLPs and energy stocks are susceptible to commodity price volatility, currency and geopolitical instability, environmental and regulatory compliance costs, seasonal weather, control of reserves by state-owned companies, geographic concentration, and technological competitiveness.

Recommended Reading

Analysts: DOE’s LNG Study Will Result in Few Policy Changes

2024-12-18 - However, the Department of Energy’s most recent report will likely be used in lawsuits against ongoing and future LNG export facilities.

Venture Global Asks FERC to Open Next Plaquemines LNG Block

2025-03-03 - The additional train start-up of Venture Global’s Plaquemines LNG facility would bring the overall project halfway to completion.

Trump Fires Off Energy Executive Orders on Alaska, LNG, EVs

2025-01-21 - President Donald Trump opened his term with a flurry of executive orders, many reversing the Biden administration’s policies on LNG permitting, the Paris Agreement and drilling in Alaska.

Dell: Folly of the Forecast—Why DOE’s LNG Study Will Invariably Be Wrong

2025-01-07 - Kimmeridge’s Ben Dell says the Department of Energy’s premise that increased LNG exports will raise domestic natural gas prices ignores a market full of surprises.

Report: Trump to Declare 'National Energy Emergency'

2025-01-20 - President-elect Donald Trump will also sign an executive order focused on Alaska, an incoming White House official said.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.