Source: Hart Energy

As M&A values have ticked upward in the Permian Basin in recent months, the prime real estate holders in the Midland and Delaware basins are being unusually low key—for major oil companies.

The majors have seemingly eschewed or merely dabbled in shale drilling. That much is clearly changing.

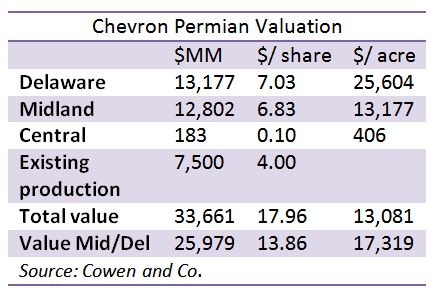

Chevron Corp. (NYSE: CVX) has built a 2 million acre empire in Texas and New Mexico—including 1.5 million acres in the Midland and Delaware basins, said Sam Margolin, an analyst at Cowen and Co., in an Aug. 31 report.

Chevron said in July that its potentially recoverable resources are about 9 billion barrels of oil equivalent (Bboe).

Margolin said Chevron, ExxonMobil Corp. (NYSE: XOM) and Royal Dutch Shell Plc. (NYSE: RDS.A) all have large, valuable positions in the Permian.

Chevron is among the most underappreciated Permian operators, he said. The company has assessed 30% of its operated acreage and estimates it has 1,300 current drilling locations with at least 10% returns at less than $40 oil.

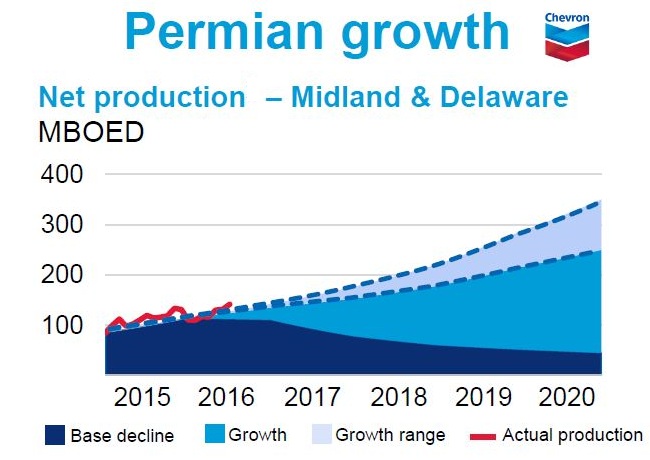

In its second-quarter earnings call, Chevron’s Executive Vice President Jay Johnson said shale and tight production increased by 50 Mbbl/d primarily due to growth in the Midland and Delaware basins in the Permian.

“We're making excellent progress in the Permian towards the growth we discussed at our analyst meeting in March,” he said. “Production this quarter was 21% or 24,000 barrels of oil equivalent per day [boe/d] higher than the second quarter of last year.”

Johnson added that Permian development costs per barrel dropped by about 30% since second-quarter 2015.

With so many recent sales tagging acreage in the upper $20,000 to $30,000 range, Chevron’s Permian asset could be worth $38 billion, Margolin said.

“While asset quality can vary widely by location, recent deal values have exceeded our expectations, implying a 12% premium over our DCF model” for Chevron, he said.

Nevertheless, Chevron’s shares haven’t seen much impact, while other E&Ps’ shares have rallied up by an average of 40% as Permian deals have been struck.

Nevertheless, Chevron’s shares haven’t seen much impact, while other E&Ps’ shares have rallied up by an average of 40% as Permian deals have been struck.

“Importantly, recent M&A in the play is likely a conservative comp for CVX's position given the fact that 85% of the company's drilling locations have no or low royalty expense,” Margolin said.

Permian properties have routinely shown royalty burdens of 23% to25%.

Chevron isn’t alone in its Permian largess.

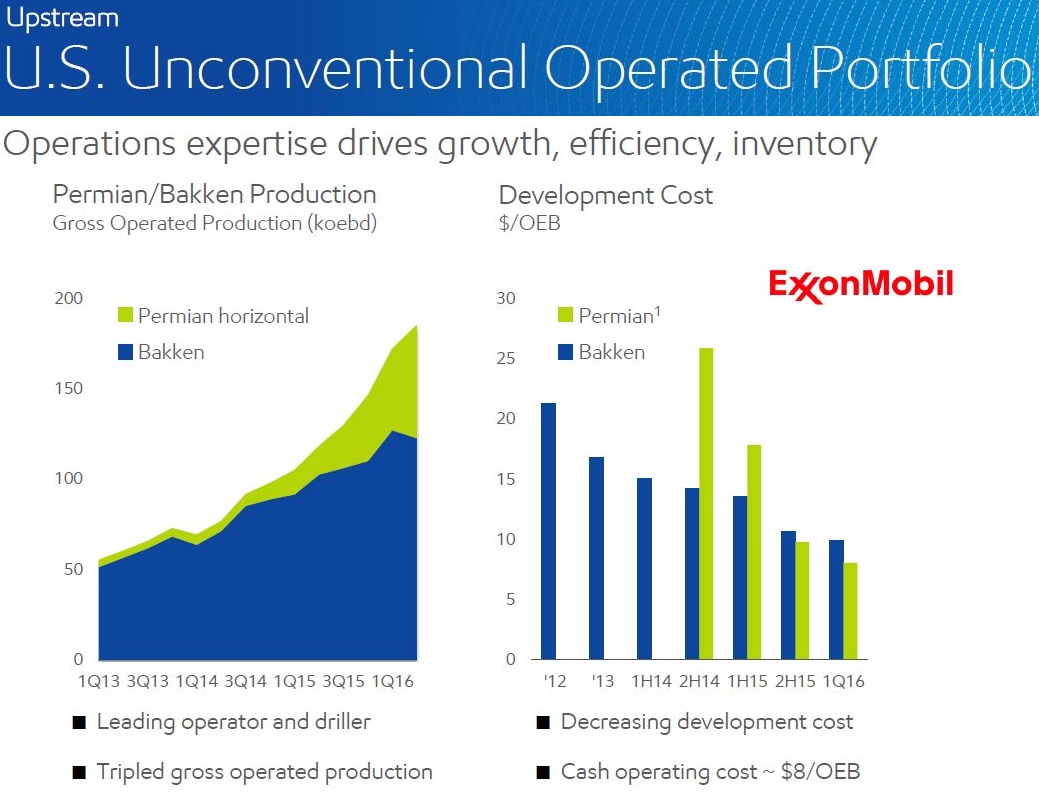

ExxonMobil has roughly 1.4 million acres and 1,000 drilling locations that offer 10% returns at less than $40/bbl.

After doubling its output in 2015, the company continues to grow production in the region despite reducing its rig count.

“The company has reduced development costs by more than 60% from more than $25/boe to less than $10/boe,” Margolin said. “Recent deal prices imply a value of $35 billion to XOM's Permian asset.”

Shell has also restructured its net asset management (NAM) portfolio over the last several years and built a sizable position in the Delaware. The company holds about 300,000 net acres with more than 5,000 future drilling locations and an estimated resource of 2 Bboe.

The company estimates that 75% of its acreage breaks even between $30/bbl to $50/bbl.

“While drilling activity is expected to remain muted in the near term, RDS plans for the asset to be a key growth contributor post-2020,” Margolin said. “Recent deal prices imply a value of $5 billion to RDS’ Permian asset.”

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

USD Completes Final Asset Sale of Hardisty Terminal

2025-04-11 - USD Partners was obligated to sell the Hardisty Terminal, in Alberta, Canada, after entering a forbearance agreement with its lenders on June 21 2024.

USEDC’s Plans for $1B in Capex, M&A on Track as Oil Prices Stumble

2025-04-11 - Volatility won’t affect Permian Basin-focused U.S. Energy Development Corp.’s day-to-day operations or its plans for deals, CEO Jordan Jayson told Hart Energy.

BP Forecasts Dip in First-Quarter Upstream Production

2025-04-11 - BP anticipates a quarter-over-quarter decline in upstream production when it reports earnings later this month.

The New Minerals Frontier Expands Beyond Oil, Gas

2025-04-09 - How to navigate the minerals sector in the era of competition, alternative investments and the AI-powered boom.

Q&A: Where There’s a Williams, There’s a Way for Gas

2025-04-09 - Midstream giant Williams Cos. leads the natural gas bulls on the great infrastructure buildout, President and CEO Alan Armstrong tells Hart Energy.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.