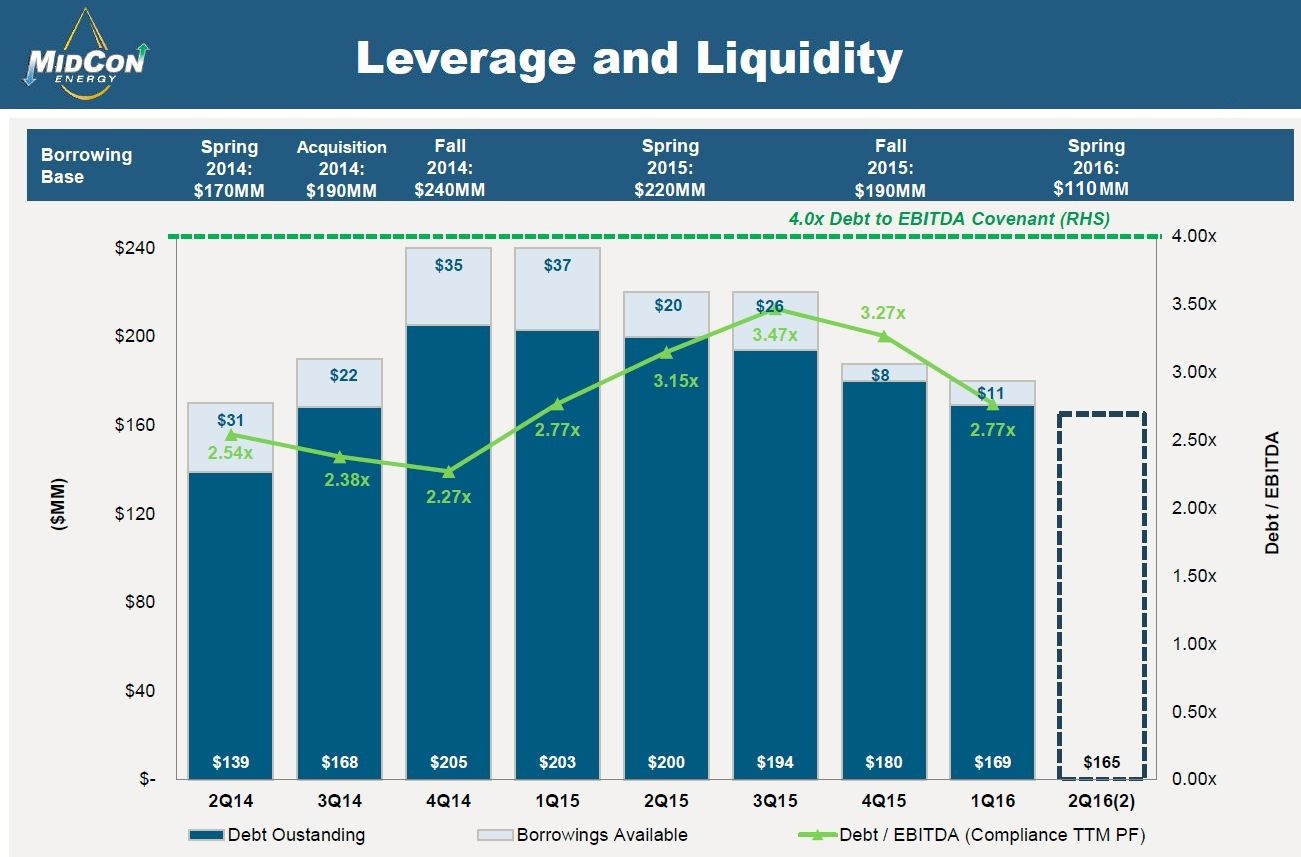

Mid-Con Energy Partners LP’s (NASDAQ: MCEP) borrowing base re-determination on June 1 allows the company a $53 million overage while it waits for its debt to be reduced by a sale of 15% of its proved reserves.

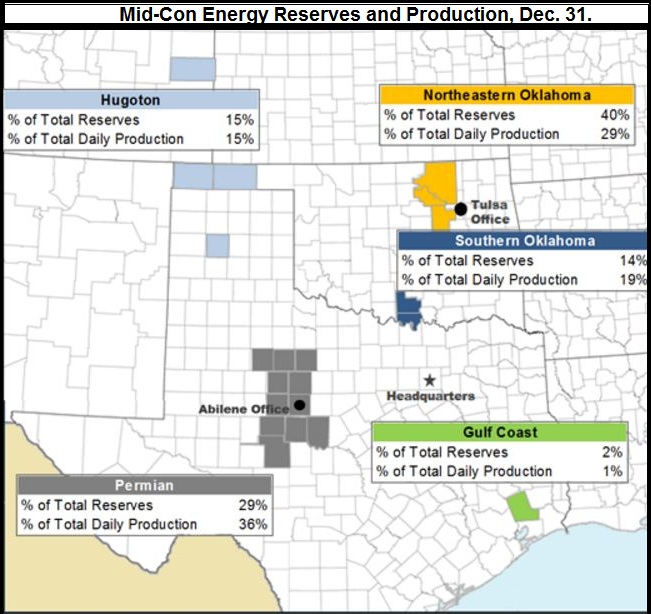

In late May, the Dallas-based MLP said it would sell all of its oil and natural gas assets within its Hugoton area to an undisclosed and unaffiliated buyer for $18 million. The position also produced about 15% of the company’s production as of December.

Upstream MLPs have been among the largest casualties of the downturn. In May, Linn Energy LLC and Breitburn Operating LP filed for Chapter 11 bankruptcy with collective debt of $10.7 billion.

Mid-Con has little wiggle room in its liquidity and will likely remain that way through 2016, said Kevin Smith, analyst at Raymond James & Associates.

“The announced transaction does little to relieve its current liquidity issues,” Smith said in a May 27 report. “The company will need to evaluate further divestitures, particular in light of the borrowing base redetermination.”

At the end of 2015, Mid-Con had 70 producing wells, 45 injection wells,five water supply wells, and 86 inactive wells in the play. Its total proved reserves were 3.2 million barrels of oil equivalent (MMboe) and average net production in December was 682 boe/d.

Mid-Con’s debt would fall to $145 million when proceeds from the sale are applied to its outstanding revolving credit facility. The company’s new borrowing base is comprised of the $53 million permitted overadvance and a $110 million conforming tranche.

As of May 31, Mid-Con had $163 million in outstanding debt. The divestiture is set to close by July 29.

Jeff Olmstead, Mid-Con president and CEO, said each asset in the company’s portfolio will be evaluated. Mid-Con is reducing leverage and improving operating efficiency, he said.

“Along with the cost reduction initiatives we've implemented since late 2014, the divestiture of the Hugoton area assets will help us continue to lower our per boe operating costs and position Mid-Con Energy to deliver positive cash margins, even in the current low oil price environment.”

Mid-Con acquired its Hugoton position in Texas and Oklahoma in February 2014 for $41 million. The transaction was primarily funded with borrowings.

Mid-Con's next scheduled bi-annual redetermination is expected to occur by Nov. 1.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Not Sweating DeepSeek: Exxon, Chevron Plow Ahead on Data Center Power

2025-02-02 - The launch of the energy-efficient DeepSeek chatbot roiled tech and power markets in late January. But supermajors Exxon Mobil and Chevron continue to field intense demand for data-center power supply, driven by AI technology customers.

Oil, Gas and M&A: Banks ‘Hungry’ to Put Capital to Work

2025-01-29 - U.S. energy bankers see capital, generalist investors and even an appetite for IPOs returning to the upstream space.

The Private Equity Puzzle: Rebuilding Portfolios After M&A Craze

2025-01-28 - In the Haynesville, Delaware and Utica, Post Oak Energy Capital is supporting companies determined to make a profitable footprint.

Riverstone’s Leuschen Plans to IPO Methane-Mitigation-Focused SPAC

2025-01-21 - The SPAC will be Riverstone Holdings co-founder David Leuschen’s eighth, following the Permian Basin’s Centennial Resources, the Anadarko’s Alta Mesa Holdings and the Montney’s Hammerhead Resources.

Artificial Lift Firm Flowco Seeks ~$2B Valuation with IPO

2025-01-07 - U.S. artificial lift services provider Flowco Holdings is planning an IPO that could value the company at about $2 billion, according to regulatory filings.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.