The Internal Revenue Service enacted a temporary halt at the end of March in the issuance of MLP qualifying income private letter rulings (PLRs) until it conducts an internal committee review.

An MLP does not pay corporate taxes if at least 90% of its income is from qualifying sources as defined by the Internal Revenue Code 7704. Such sources include the exploration, development, mining or production, processing, refining, transportation or marketing of any mineral or natural resource. A company may request a letter from the IRS that clarifies the law according to the specific situation.

With a record 28 PLRs issued in 2013 (vs. 12 in 2012 and less than five per year between 2009 and 2011) and nine PLRs year to date, perhaps the IRS decided it was time for spring break.

Instead, Mary Lyman, executive director of the National Association of Publicly Traded Partnerships noted, “the IRS and the Treasury have been reviewing the PLR process in various areas, and MLPs are the current rotation. A similar pause and review occurred last year with Real Estate Investment Trusts.”

The internal committee review is expected to be completed within two to three months.

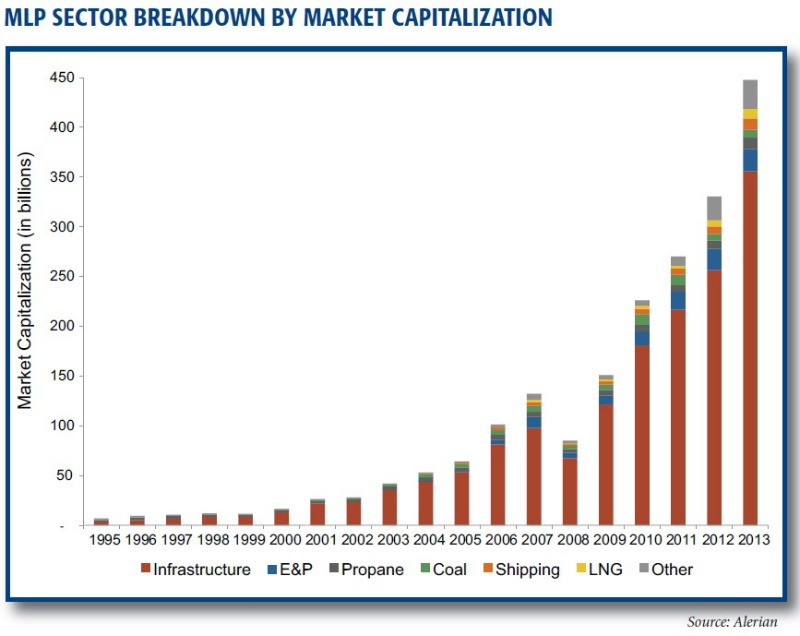

Non-traditional MLPs

Lyman’s reference to areas previously not considered refers to 2012 and 2013 PLRs interpreting qualifying income to include the disposal of fracking water and fluids and the marketing of sand and proppants. Such qualifying income interpretations led to the IPOs of various non-traditional MLPs. However, the vast majority of the $450 billion energy MLP sector—80% to be exact—is still engaged in infrastructure-related activities.

This pause in PLR issuance presents an opportune time to focus on how subsectors in the MLP asset class have evolved.

In earlier years (1995-1997), MLP market cap totaled $10 billion and only 50% of the sector was engaged in energy infrastructure. The two largest MLPs in 1995 were propane distributors, together comprising 30% of MLP market cap. During the late 1990s and early 2000s, names that are now large-cap core holdings in most MLP investors’ portfolios went public, such as Energy Transfer Partners, Enterprise Products Partners, Plains All American Pipeline and Magellan Midstream Partners. These names, as well as early infrastructure MLPs such as Kinder Morgan Energy Partners and Buckeye Partners, paved the way for the market cap to grow fivefold to $50 billion in 2004.

Almost every year since 2002, the energy infrastructure subsector has maintained an 80%+ weighting of total MLP market cap. When commodity prices improved in the early and mid-2000s, the marketplace saw the IPOs of upstream and shipping MLPs, which tend to trade with commodity prices. In 2007, at the peak of oil and gas prices, exploration and production MLPs comprised 9% of the sector. This was the one year energy infrastructure MLPs fell below the 80% sector market cap since 2002.

Now, variable distribution MLPs engaged in business such as fertilizer, chemicals and refining are emerging—a trend that analysts expect to continue given investor interest and PLR interpretation.

At the end of 2013, 57 of the total 111 energy MLPs were considered infrastructure companies. Of the 57, the Alerian MLP Infrastructure Index (AMZI) tracks the performance of the largest 25, or 65% of MLP market cap. More than $10 billion of the $16 billion in Alerian-linked products track the Alerian Index Series, which includes AMZI. This demonstrates that energy infrastructure is here to stay.

Recommended Reading

PotlatchDeltic Enters Lithium, Bromine Lease Agreement in Arkansas

2025-02-06 - PotlatchDeltic’s agreement with gives Tetra Brine Leaseco covers about 900 surface acres in Lafayette County, PotlatchDeltic says.

McDermott Completes Project Offshore East Malaysia Ahead of Schedule

2025-02-05 - McDermott International replaced a gas lift riser and installed new equipment in water depth of 1,400 m for Thailand national oil company PTTEP.

SLB: OneSubsea to Provide Equipment for Vår Energi Offshore Norway

2025-02-04 - The OneSubsea joint venture among SLB, Aker Solutions and Subsea7 will support multiple oil and gas projects on the Norwegian Continental Shelf for Vår Energi.

Resurrected Enron Hijinks Gets Serious with New Electric Business

2025-02-03 - After Enron returned as a seemingly elaborate hoax, Enron Energy Texas’ vice president told Hart Energy the company aims to deliver real electricity to consumers.

E&P Highlights: Feb. 3, 2025

2025-02-03 - Here’s a roundup of the latest E&P headlines, from a forecast of rising global land rig activity to new contracts.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.