The rapid pace of Permian Basin production growth is well known by now, as far as crude oil output and associated natural gas are concerned. But less light has been focused on the gas liquids component, even as the midstream industry along the Gulf Coast—and particularly the Mont Belvieu, Texas, processing and storage hub—ramps up activity levels and investments to meet growing demand from the petrochemical sector and export markets.

Emphasizing the important role played by the Gulf Coast, a recent Citi research report said the U.S. has become a “massive hydrocarbons hub.” As measured by the sum of gross imports and gross exports including crude, products and NGL, the U.S. holds a 12% position in total global oil liquids trade, outpacing China at about 8%, Saudi Arabia at 6% and Russia at 5%, according to the report.

Much of this achievement has its foundations in the key hub for NGL storage and fractionation found at Mont Belvieu, 31 miles east of Houston in Chambers County, Texas. The location is strategic because of favorable geology: It lies on top of a massive salt structure. Since the 1950s, oil industry players have carved out huge NGL storage caverns in the salt.

Scores of these caverns are run by the major Mont Belvieu players, which include Enterprise Products Partners LP, Targa Resources Corp., ONEOK Inc. and Lone Star LNG LLC, a subsidiary of Energy Transfer Partners LP. And there are many others.

Size matters

The sheer size of the NGL complex, with the largest location of underground storage capacity in the world, means Mont Belvieu is a pricing point for much of North American and global trading in NGL markets.

Strong growth in U.S. oil output—as well as a richer gas stream than expected in several basins, especially the Permian—has led to the go-ahead for several major new pipeline projects bringing mixed NGL, or Y-grade, to Mont Belvieu. By one estimate the projects will roughly double the combined capacity to transport NGL in the Permian.

Enterprise announced in April 2017 that it would build its Shin Oak NGL pipeline, expected to be in service in second-quarter 2019. The new pipeline was due to originate at Enterprise’s Hobbs NGL hub in Gaines County, Texas, on the Texas-New Mexico border and to run 571 miles to Mont Belvieu. Initial capacity of the pipeline at that time was designed to be 250,000 barrels per day (Mbbl/d), expandable to 600 Mbbl/d.

Shin Oak upsize

In May, following an agreement by Apache Corp. to commit all Alpine High NGL output to Enterprise, Shin Oak’s planned capacity was upsized to 550 Mbbl/d. A commitment was made for a minimum of 205 Mbbl/d from Apache, and the route was amended to run 658 miles from Reeves County, Texas, to Mont Belvieu. In-service is still set for the second quarter of next year.

As part of the latter long-term agreement, Apache has an option for a 33% equity stake in Shin Oak, which can be exercised after the in-service date. Of note, Apache has negotiated similar equity options on three other pipelines in the region, including an NGL pipeline to the Waha Hub in Texas

Waha serves as the major natural gas pipeline hub and price point in the Permian.

Targa announced its Grand Prix NGL pipeline in May 2017. The original plan was to transport volumes from the Permian Basin, as well as Targa’s North Texas system, to Mont Belvieu. An extension of the plan, connecting Targa’s southern Oklahoma system to Grand Prix, was added in March. Targa has held to the previously projected in-service date of second-quarter 2019.

Capacity of the Grand Prix Pipeline will vary by segment. The Permian-to-North Texas leg will be about300 Mbbl/d, expandable to 550 M bbl/d, according to Targa, with capacity of the next leg to Mont Belvieu set at about 450 M bbl/d, expandable to 950 Mbbl/d.

Targa has put the costs of increasing capacity at about 10% of the original build cost.

As for financing, Targa had struck a deal earlier in the year with Stonepeak Infrastructure Partners providing for three development joint ventures (JVs), including one for the Grand Prix Pipeline. The others covered the Gulf Coast Express Pipeline and Targa’s next fractionation train. The DevCo JV related to Grand Prix took a 20% interest in the project, with Stonepeak owning a 95% interest in the DevCo JV.

The DevCo JV gives Targa an option to buy back its interests from Stonepeak for four years beginning when all three projects begin commercial operations, or Jan. 1, 2020. The purchase price will be based on a predetermined fixed return or a multiple of invested capital, including distributions received by Stonepeak from the DevCo JV.

Another greenfield NGL pipeline underway is EPIC NGL Pipeline, albeit with a different destination than Mont Belvieu. Anchored by BP Energy Co., the 700-mile project finished its first phase of construction, running 40 miles from Eddy County, N.M., to Reeves County, Texas, last spring. Plans call for completion of the second phase to Upton Co. this summer and the third to Corpus Christi, Texas, in Nueces County in the second half of 2019.

EPIC plans

Capacity of the EPIC NGL Pipeline, set to run side-by-side with EPIC’s crude line, is about 350 Mbbl/d. EPIC is building a fractionation complex in Corpus Christi and a purity product pipeline distribution system. The latter includes an ethane pipeline that will reach the Markham, Texas, area for storage needs and interconnects to other market centers including Mont Belvieu.

Markham lies within a major industrial complex in Matagorda County, Texas, midway between Houston and Corpus Christi.

In terms of expanding an existing pipeline, DCP Midstream said the next step in a series of expansions for its Sand Hills Pipeline across South Texas would be to add 85 Mbbl/d. Following a recent upgrade to 400 Mbbl/d, this would further expand capacity in two stages, by 25 Mbbl/d and 60 Mbbl/d in the third and fourth quarters of this year, respectively. Sand Hills carries Permian NGL to Mont Belvieu.

In addition, DCP and SemGroup Corp. in late May announced an open season for a project to transport NGL on the White Cliffs crude pipeline and Southern Hills NGL pipeline, which would move gas liquids south from the Denver-Julesburg (D-J) Basin and the Midcontinent Scoop/Stack plays. If successful, this would connect NGL coming from Weld County, Colo., in the heart of the D-J Basin, to Mont Belvieu.

How does all this shake out in terms of the overall demand/supply picture for NGL going forward? In the Permian, in particular, will the basin be overbuilt in terms of takeaway capacity, or will growing demand quickly translate into elevated utilization levels, given robust industry activity in the basin?

In terms of takeaway, current nameplate capacity of eight major pipelines flowing into Mont Belvieu totals about 1.83 million barrels per day (MMbbl/d), according to a recent report by RBN Energy’s Housley Carr. However, when adjustments are made for volumes preceding or following the Permian—inbound flows from the Rockies or downstream additions from the Eagle Ford—effective capacity is significantly lower.

Capacity growth

Incorporating these adjustments, effective takeaway capacity for pipelines in the Permian—easily the largest driver of NGL growth in the U.S.—is reduced to about 1.2 MMbbl/d, according to RBN Energy estimates. And obviously, absent new pipeline projects, this would substantially narrow the room to see NGL production grow before coming up against a ceiling on output.

However, major projects are in place and underway in the basin.

If midstream companies execute on their plans and meet timelines for expected in-service dates, the projection by RBN Energy is that the current effective NGL takeaway capacity of about 1.2 MMbbl/d in the Permian is likely to double within the next 18 months.

Even if recent rates of gas liquid production growth moderate, much of that added capacity may be needed over time.

As of late May, Permian NGL production was estimated to be running at about 1 MMbbl/d, a jump of as much as 25% in just eight months from a September 2017 level of 800 Mbbl/d, observed the RBN Energy report. Projections by RBN call for Permian NGL production to increase further to more than 1.1 MMbbl/d by the end of 2018, 1.3 MMbbl/d a year later and to 1.6 MMbbl/d by the early 2020s.

Note that the above capacity estimates include ethane that is typically rejected back into the residue gas flowing from processing plants into the nation’s natural gas transmission system.

What are some of the variables that could affect the outlook either way?

Ethane variables

In addition to the obvious issue of commodity price fluctuations—and the recent blowout in differentials between the Midland Hub and Houston and Brent—RBN Energy anticipates some variability in ethane demand and, in turn, the level of ethane rejection.

As more ethylene crackers come into service, ethane demand from the U.S. petchem sector is forecast to rise from roughly 1.1 MMbbl/d last year to 1.7 MMbbl/d in 2019 and 1.9 MMbbl/d in 2022-2023. With this increase in petrochemical demand, ethane rejection is expected to drop below 600 Mbbl/d in 2019, down from 790 Mbbl/d in 2017. But the trend will be fleeting after the surge in petchem demand levels out.

“U.S. natural gas production, especially gas with high ethane content, is growing so fast that ethane supply will continue to outstrip demand for the foreseeable future,” said RBN Energy.

Colton Bean, director of midstream research at Tudor Pickering Holt & Co., pointed to wet gas exceeding expectations in terms of liquids content as a factor in meeting future petchem demand.

Even in the downturn, with levels of crude and dry gas output slumping, the natural gas stream proved “much richer than historical precedent and richer than expectations,” he recalled. “The richness of the gas was offsetting the downturn in activity levels.”

This is expected to provide a steady feedstock to meet growing demand from the U.S. petchem sector.

“We’ve already skated through this first wave of petchem demand, and we haven’t seen any price spikes,” Bean said. “Even with the rise we see in petchem capacity coming online over the next few years, we really don’t see a scenario where the market is not oversupplied on ethane. You may see some week-to-week volatility, but we don’t think there will be any material price spikes.”

And Bean doesn’t expect the market will have to reach out far beyond the Gulf Coast to meet its needs.

Gas price parity

“You don’t have to pay that much more of a premium over natural gas pricing to incentivize the Gulf Coast-centric areas, like the Eagle Ford and Scoop/Stack, to flow to the Gulf Coast,” he said. “It’s somewhere in that high single-digit level, about the 7 cent-to-9 cent range. And as you project out to the early 2020s, you’re likely to see ethane pretty close to parity with natural gas on pricing.”

As for projected NGL pipeline takeaway, Bean was optimistic about the new capacity being needed.

“When the three big greenfield projects were announced (by Enterprise, Targa and EPIC), everyone immediately jumped to the conclusion that we would be overbuilt on Permian NGL takeaway, but that wasn’t our view,” he added. “As you get into the early part of the next decade, you’ll be using the fully expanded capacity of the pipelines. And we see a scenario in the not-too-distant future when we could need some more expansion.”

Energy Transfer’s Lone Star Express pipeline could be “a bit of a swing factor,” Bean said. “It’s a very large pipeline, and that’s one that can be expanded easily. As you start to fill up the new capacity, you’ll see some expansions either from the new pipes or from Lone Star Express. We don’t view takeaway as being materially overbuilt. We think there’s going to be a need for those pipes.”

What markets?

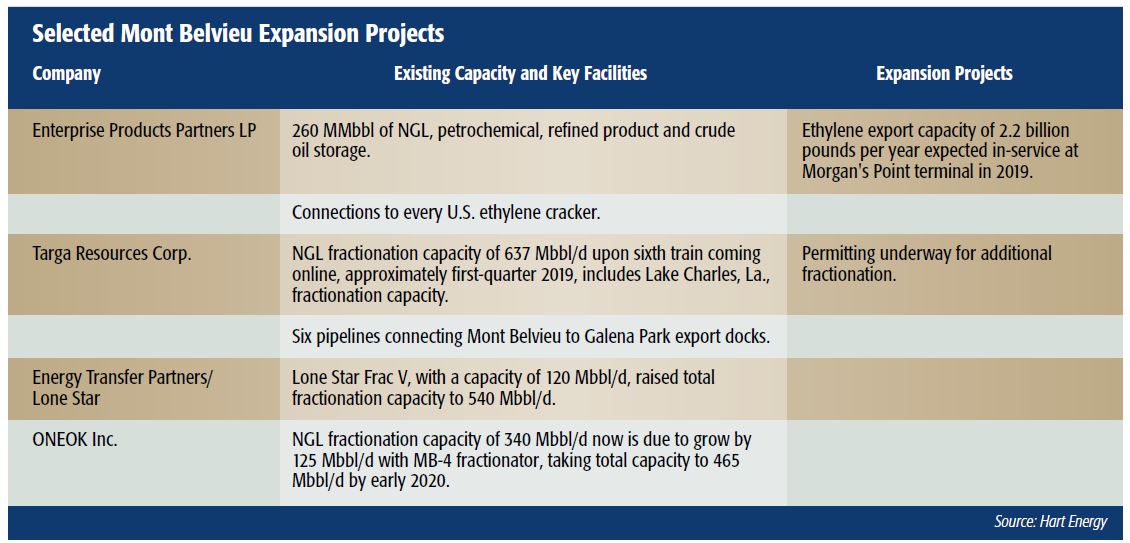

With drilling activity driven by a combination of attractive crude prices and liquids-rich gas, midstream players have been adding processing, pipelines and fractionation capacity, as indicated by the accompanying table. But that doesn’t address questions regarding markets for purity products coming out of the fractionator tailgates.

Away from domestic petchem demand, Bean sees overseas demand for LPG products—propane and the butanes—but only a very narrow range of potential foreign purchasers for ethane.

“As you look at ethane, it’s really more of a domestic market,” he explained. “Exporting ethane is not particularly easy or cheap. If we do have any growth in exports, it’s likely to be a facility that was already built to run ethane and needs a new source of supply, as with Ineos’s cracker in Grangemouth, Scotland. The other possibility is talk of ethane potentially supplying Chinese petchem demand.”

But transportation economics make it hard to argue against exporting polyethylene vs. ethane.

Plastic pellets

“When you get into polyethylene, you are basically talking about plastic pellets. You can load them onto a bulk carrier and the economics change dramatically,” Bean said. “The transportation costs are literally a fraction of what you’re paying on the ethane side.”

Bean sees greater potential demand but a deficit of investment in docks for exporting LPG.

“Right now, we don’t think dock capacity is sufficient for rising exports of LPGs,” he said. “Based on first-quarter data, it looks like we’re exporting about 1 MMbbl/d from the Gulf Coast docks vs. about 1.1 MMbbl/d of capacity for the docks we monitor, so we’re running at a pretty high capacity utilization on LPG exports.

“As you look forward, there’s a scenario where the Gulf Coast effectively runs out of dock capacity. Assuming propane and butane comprise 38%-40% of the liquids stream, the Permian Basin alone could generate over 500 Mbbl/d of LPG growth over the next few years. But we only have 100 M bbl/d of spare capacity today,” he added.

According to Bean, there is some brownfield dock capacity that can be built out, but it falls short of the likely requirements to avoid a steep discount in domestic LPG pricing vs. international pricing.

“It looks like we need some incremental investment in LPG exports to make sure we don’t go back to where we were a few years ago, when we were swamping the domestic market and you had this huge arbitrage between domestic and global pricing,” he said. “You need to see that investment happen to avoid a disconnect occurring again between U.S. and global markets.”

Chris Sheehan can be reached at csheehan@hartenergy.com or 303-800-4702.

Recommended Reading

BP Earns Approval to Redevelop Oil Fields in Northern Iraq

2025-03-27 - The agreement with Iraq’s government is for an initial phase that includes oil and gas production of more than 3 Bboe, BP stated.

E&P Highlights: March 31, 2025

2025-03-31 - Here’s a roundup of the latest E&P headlines, from a big CNOOC discovery in the South China Sea to Shell’s development offshore Brazil.

Oxy CEO: US Oil Production Likely to Peak Within Five Years

2025-03-11 - U.S. oil production will likely peak within the next five years or so, Oxy’s CEO Vicki Hollub said. But secondary and tertiary recovery methods, such as CO2 floods, could sustain U.S. output.

Black Gold, LGX Find Multiple Pay Zones in Western Indiana

2025-04-04 - Black Gold Exploration Corp. and LGX Energy Corp. are working to start production at the Fritz 2-30 oil and gas well in Indiana within 60 days.

E&Ps Pivot from the Pricey Permian

2025-02-01 - SM Energy, Ovintiv and Devon Energy were rumored to be hunting for Permian M&A—but they ultimately inked deals in cheaper basins. Experts say it’s a trend to watch as producers shrug off high Permian prices for runway in the Williston, Eagle Ford, the Uinta and the Montney.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.