CEO Doug Lawler painted Chesapeake in Shakespearean terms as a once-dominant company that, after faltering under debt, is regaining its edge through efficiency and A&D, including a $500 million Midcontinent sale. (Image courtesy of NAPE Summit/713 Photography)

HOUSTON—Doug Lawler faced the lunchtime crowd at NAPE on Feb. 7 with an easy, just-the-facts demeanor, and perhaps a bit of confidence another deal gives the CEO of Chesapeake Energy Corp. (NYSE: CHK).

About 20 hours earlier, Chesapeake said it had sold nearly 240,000 noncore Midcontinent acres for $500 million.

Every half billion dollars helps.

Roughly five years into Lawler’s leadership, Chesapeake remains fixed on cutting away more debt—up to another $3 billion “as soon and as quickly as we can.”

“But in a low-price environment, we’re not going to just liquidate our assets. It needs to be accretive,” he told the attendees of the NAPE Summit global business conference.

Chesapeake’s strategy to divest at the right price continued Feb. 6, with the company saying it signed agreements in fourth-quarter 2017 and first-quarter 2018 for a trio of asset sales in the Midcontinent.

However, the company continues to face headwinds due to its highly leveraged balance sheet. Chesapeake shares fell about 7.5% on Feb. 7 despite fourth-quarter production that beat Wall Street estimates.

The divestitures include producing properties, undeveloped assets and business property and equipment in the company's Mississippian Lime operating area -- and an exit from play in the northern Anadarko Basin, Lawler said.

With other assets in central and western Oklahoma, Chesapeake is selling about 238,000 net acres, 3,000 producing wells and an average 23,000 barrels of oil equivalent per day (boe/d) net to Chesapeake. About 25% of production volumes are oil.

The buyers of the properties were not disclosed.

One of the divestitures closed in January and the remaining agreements are expected to close by the end of the second quarter.

Chesapeake will use the proceeds to reduce outstanding borrowings under its revolving credit facility in the first half of 2018 or to refinance to reduce interest expense on other debt, depending on market conditions.

On Wednesday, Lawler also touted the company’s decision to hold on to its stake in FTS International Inc. (NYSE: FTSI), a hydraulic service provider it has held a stake in since 2006.

On Feb. 6, following FTS International’s IPO, Chesapeake sold about 4.3 million shares to reap $78 million in proceeds. Chesapeake retains 22 million shares in the company.

FTS remains a “substantial source of value for the company,” Lawler said.

Despite a no-nonsense talk, Lawler said he sees echoes of Chesapeake in seemingly artistic terms. At times, he compared the process of transforming the company from a debt-laden misadventure (past investments such as a restaurant fell far outside of E&P norms) to Michelangelo’s sculpting of David from a slab or marble or an Elizabethan drama.

“Chesapeake is a very storied company, one with a very rich history,” Lawler said. “It’s almost Shakespearean in a way. Chesapeake has experienced so many great things over the past 25 years or so but also experience many great challenges.”

Lawler’s mission to put Chesapeake’s back on sound financial footing has been an unrelenting, detached commitment to selling what it doesn’t need and cutting costs.

Once the No. 2 driller in the country with 180 rigs—more rigs than all but Texas currently employs—the company’s $21.25 billion in leverage finally caught up with it in 2013, bringing activist investor Carl Icahn in to trim the company’s spending.

The effort, now in entering its fifth year, has reduced corporate debt in half to 11.2 billion. Chesapeake also stripped away 42% of its midstream commitments to $6.7 billion. And it eliminated 75% of debt maturing between 2018 and 2020—now down to $3.2 billion.

“The common theme you see across these past several years is billions and billions and billions of dollars in improvement in Chesapeake Energy,” Lawler said.

The recent Midcontinent sales also continue Chesapeake’s prolific A&D pace. During the past several years, the company has reduced its once leviathan 11-million net acre position to about 4.95 million acres. Between 2016 and 2017, the company divested sold $3 billion in assets.

The company has also squeezed expenses while keeping production flat. Lease operating expenses have dropped to an estimated $800 million in 2017 from $1.4 billion in 2012.

“We’re operating on a capital efficiency of about one-seventh of what was spent four and five years ago,” he said.

Production remains about the same as 2012, though Chesapeake also hit a fourth-quarter goal of producing 100,000 barrels of oil.

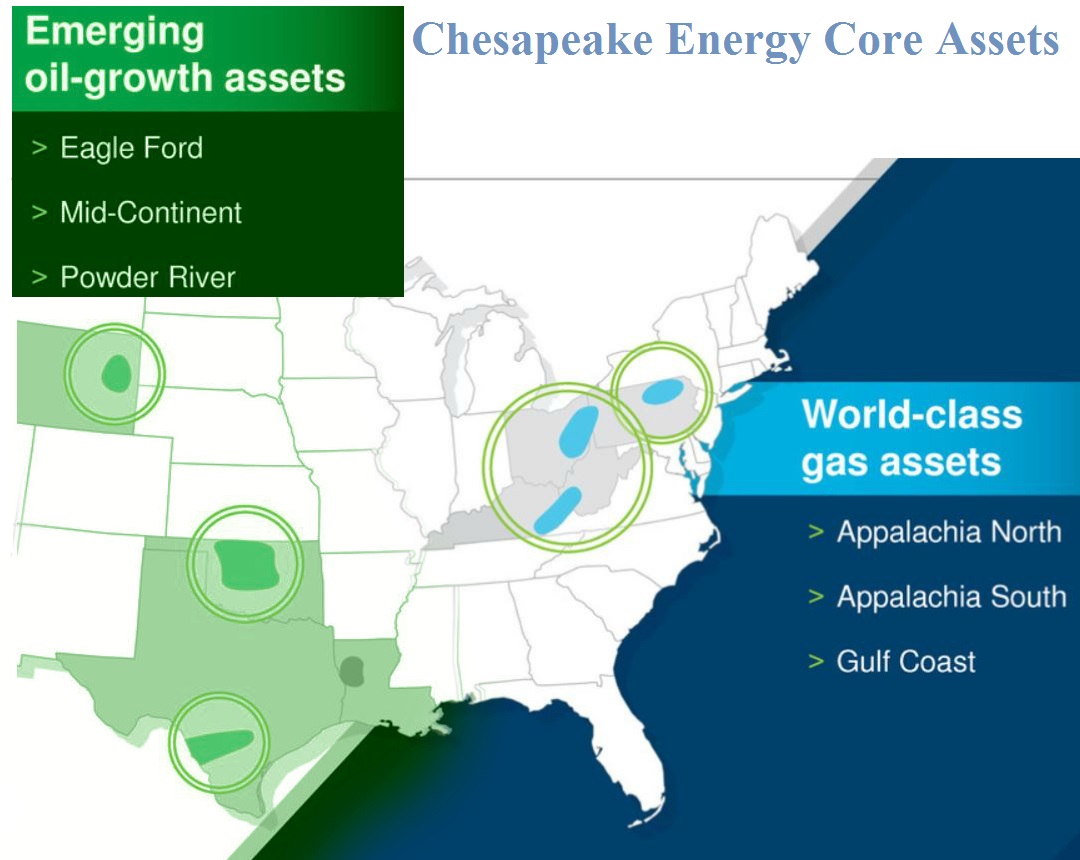

Lawler said the company expects to reach free cash flow neutrality this year while keeping its focus on its gas assets in the Appalachian Basin and Gulf Coast and its emerging oil production in the Eagle Ford, Midcontinent and Power River Basin.

Chesapeake could, of course, grow at a far stronger rate, Lawler noted. But the goal is to fund production in the most valuable way possible.

Success, at least for now, is not about producing one more barrel.

That was the past.

“We’re investing every dollar in the best location,” Lawler said, “not the next location.”

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.