Shell cites LNG in its takeover bid for BG Group

Shell and BG Group jointly announced a takeover bid of £47 billion (US$70 billion), with Shell paying a value of 1,370 pence per BG share, including 383 pence in cash and 0.4454 in its own B shares. The value represents a 52% premium on BG’s 90-day volume-weighted average trading price.

Shell listed LNG as one of the primary factors that led to the offer. Shell believes that it can benefit from the increased access to new markets and from the sheer scale of liquefaction capacity that the acquisition of BG will give it. Shell will increase its equity liquefaction capacity by about 80% from its 2014 position, and Shell would gain access to BG’s liquefaction operations in Egypt, Australia, Trinidad and Tobago and Nigeria.

In addition to its post-final investment decision projects that will be coming online through 2018, Shell, with the BG addition, will also gain access to tolling capacity with what will be the first U.S. liquefaction project, Sabine Pass LNG, and it gains a foothold in the attractive Lake Charles, La., and Tanzanian proposals.

Going forward, Shell said it would favor projects that are under its control, give it a diversity of LNG supply and have a lower capital cost per unit. While brownfield projects are attractive, it said sometimes a lack of ownership in a project would preclude their expansions.

Shell referred to its acquisition of Repsol LNG last year as a factor in what lends it confidence that this acquisition will come to represent a successful integration.

Analysts generally agreed with the strategy of the deal.

Wood Mackenzie noted, “Shell will have unrivaled flexibility and exposure to virtually every major LNG supply source and market globally, which means significant scope for portfolio optimization. The move re-ener- gizes Shell’s LNG development pipeline, adding a leading U.S. position, entry to East Africa, and new options to expand an already giant presence in Australia and Canada.”

Simmons and Co. thinks the deal “makes immense strategic sense for Shell, if one takes a long-term view on LNG markets and commodity prices. The acquisition will create an LNG behemoth with unmatched scale and flexibility.”

Tudor, Pickering and Holt wrote in a client note, “It [the deal] is a conscious decision to de-emphasize U.S. shale and to stick to its strengths (deepwater/LNG). It sets Shell apart from the other supermajors by ensuring long-term growth in upstream production but also in terms of LNG volumes. It gives Shell higher oil price gearing and makes it more of a bet on higher oil prices and LNG prices.”

--Brian Mothersole, Hart Energy

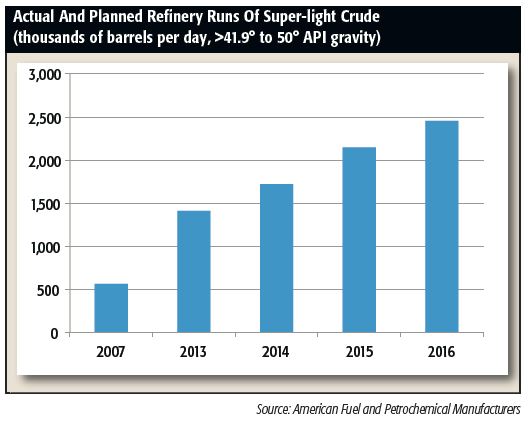

US refiners can absorb domestic output growth--survey

Most U.S. refiners will have ample capacity to process domestic “super light” crude, easily absorbing expected growth in U.S. oil production, a study from in- dustry trade group American Fuel and Petrochemical Manufacturers (AFPM) has found.

By 2016, refiners will be able to increase consumption of lighter U.S. crudes—between 42° API and 50° API gravity—by more than 730,000 barrels per day (bbl/d), according to the third- party survey of AFPM members. Improvements to domestic logistics would allow another 800,000 bbl/d of distillation, the group said.

The findings are the industry’s latest volley in its struggle to preserve the ban on U.S. crude oil exports. By maintaining access to lower-priced domestic crudes, many refiners insist the ban is essential for them to remain competitive in the global market. The AFPM-funded report received a response rate of 61%.

The organization rejects claims that the Obama administration and Congress must overturn a 42-year moratorium on U.S. crude exports because the nation's refineries are unable to process the growing glut of domestic light tight oil (LTO).

“We as the U.S. refining industry are not and should not be the excuse for lifting the crude export ban,” AFPM President Charles Drevna said in a prepared statement. “If it’s to be lifted, fine; but base it on facts and not fiction.”

In connecting the oil-export debate to a broader discussion linked to inadequate delivery infrastructure, Drevna added, “For the refiners, getting the crude oil has been a much bigger issue than refining it.”

With $5 billion in improvements planned to add 730,000 bbl/d of capacity by 2016, the AFPM study results “emphasize that U.S. refiners are not capacity-constrained in the next several years to use the growing super light production from U.S. tight oil formations.”

“The survey respondents will achieve their plans to increase use of this new crude production by continuing to reduce imported light- and medium-quality crude oils and by investing to better utilize this domestic resource,” the AFPM noted.

--Kristie Sotolongo

Hess builds on historic Bakken position

Few remember that it was Hess Corp. that discovered the prolific Bakken oil play—in 1951.

That first conventional well, drilled on the farm of namesake Henry Bakken, “flowed at the rate of 300 bbl/d for 42 hours, then went to zero,” Hess COO Greg Hill told Hart Energy’s recent DUG Bakken and Niobrara Conference and Exhibition

in Denver.

In one form or another, Hess has been in the Williston ever since and creative management techniques offer it strong returns in the future, he said. “We’re still learning a lot” about the Bakken and Three Rivers shales. “There are more opportunities and more excitement than ever in the Williston—we’re not done yet,” he said.

Hess holds 615,000 net acres in the Bakken/Three Forks plays and serves as operator for most of that acreage. A plus it enjoys is the bulk of that acreage lies in the core of the plays’ most-productive areas.

Hess has some 1,200 potential well locations identified. Net North Dakota production for this year should be 95,000 to 105,000 bbl/d, equivalent. The company’s target is 175,000 bbl/d, equivalent, by 2020, Hill said.

The Williston now accounts for 26% of production and 33% of proved reserves for the New York-based firm, he said.

Despite the potential of the Bakken, Hess must deal with the reality of current low crude prices. The producer has cut its 2015 capex to $1.8 billion in the play, down from $2.2 billion in 2014, according to Hill. It plans to place 210 wells on production this year, compared with 238 wells last year. It plans to reduce its Bakken rig count to eight during the second quarter, less than half of its peak of 17 active rigs last year.

Hess has invested considerable capital in the midstream infrastructure needed to handle that swelling production. Hill noted Hess has plans underway to make an IPO for a midstream MLP unit this year.

--Paul Hart

Midstream investing picks up where E&P leaves off

With the industry’s collective anxiety rising with every rig that is stacked, it might be time to recall that energy investing is not just about swimming upstream.

“We’re actually expecting to see an uptick in midstream M&A activity because it’s an asset class where there are a lot of E&P owners of their own midstream assets,” Duff & Phelps Managing Director Jim Rebello told Midstream Business during an interview with three of the financial advising firm’s senior executives. “They can get a better value for their midstream assets than they can for their exploration and production assets. So when you’re trying to decide on, ‘how am I going to rationalize this asset base?’ the pieces where you can get a better value will be those in the midstream space. E&P companies with controlled MLPs likely to complete an increasing number of dropdown transactions.”

“Absolutely,” agreed Jim Hanson, Duff & Phelps managing director specializing in transaction opinions, MLPs and private capital raising for companies in the energy sector.

“The last three years have all been active for dropdowns in the MLP world. This is a good source of growth if the sponsor is an E&P company or a bigger midstream company.

“It’s a great way to continue the growth trajectory of their MLPs,” he told Midstream Business. “I also think we’re going to probably see some bifurcation within the MLP sector, even in the midstream, where some companies that are closer to the wellhead or maybe a little less diversified could see some impact on volumes, whereas some of the more diversified, bigger companies that are more fee-based, will see a little less.”

There are a number of variables at play—swift drop in commodity prices, midstream buildout—but the relatively recent prolifer- ation of the retail investor into oil and gas stocks triggers a round of rattled nerves, as well.

“In the last three years, you’ve really seen the retail investor dictate the structure of the market,” Dave Herr, Duff & Phelps’ managing director and energy lead, financial reporting and valuation advisory services, told Midstream Business. “Retail investors are no longer buying the integrated oil and gas company at the same valuation that they ascribe to something that is a basin-specific E&P or gathering play. Retail investors put a premium value on the ability to invest exactly as much as they want in a specific basin.”

Oil’s reign of $100-plus/bbl might have made them see themselves as financial wizards. But how will these investors, new to the ebbs and flows of the energy business, react to $50/bbl oil? Especially if low prices persist as expected?

“That desire of the retail investors has actually created less financial stability in companies, particularly in some of the recent IPOs in the upstream space,” Herr said. Things can get dicey, he explained, when single-basin E&P players drop down their gathering systems in an MLP.

“Those captive MLPs are where you’re going to potentially see bifurcation,” Herr said.

“If you’re a single-basin play relying primarily on a single upstream company, that is now cutting back severely or totally ceasing drilling activities, the rate at which those commitments are going to be met and certainly the ability of that MLP to deliver the distributable cash-flow growth is severely diminished.”

Herr expects the downturn to result in a shakeout in the market.

“Where we saw a lot of the MLPs trading in a similar range, I think you’re going to see a separation of those that have a more sustainable long-term platform and those that were a function of the market dynamics of the last 36 months,” he said.

Rebello, Houston-based energy lead for mergers and acquisitions, stressed that the sky has not yet fallen and that the next couple of months, at least, appear to be manageable.

“Timing is an important part of this,” he said. “Volumes are expected to grow—most analysts are saying at least through mid- year, maybe into the third quarter. A lot of these MLPs in single basins won’t feel the effects until the rig count in those basins be- gins to fall. The difference is drilled wells vs. completed wells. There’s a big inventory of uncompleted wells. I don’t want to be all gloom and doom and say this is all going to come apart between March and June. Every company is going to be different, and it’s going to be a slow bleed as the decline curves begin to play themselves out.”

--Joseph Markman

Director: asset optimization gives needed boost

With low oil and gas prices squeezing profits, companies are searching for smart savings opportunities. Dale St. Denis, director for midstream of Sapient Global Markets, told Midstream Business that when times are tight, turning to a consultant who can look objectively at your business and advise you how to best utilize your assets can be a worthwhile investment for midstream providers.

Sapient Global Markets offers business advisory and technology evaluation services, St. Denis said. When evaluating a company’s options, Sapient focuses on strategy—how the company plans to ex- pand or leverage its service offerings.

“We help them with their consolidation of assets, how they ought to reposition those assets … to better serve their shippers,” he said. “We also provide technology evaluation services to help them understand what their options are for expanding their IT, or information technology, infrastructure to support their shippers with the management of these hydrocarbons through their assets.”

From an IT standpoint, companies are generally focusing on safe and reliable performance from their assets, choosing data management options that keep them updated on the specific performance of those assets.

Particularly in a downturn, however, the most important consideration for compa- nies tends to be asset optimization, he said. To be successful in a tight commodity market, leadership needs to understand “ways in which they can better leverage those assets and combine them in more value-added services for their shippers,” St. Denis said.

--Caryn Livingston

'Utter collapse' of spending might cause production to falter

The downturn of 2015 has established that shale oil economics in the Lower 48 are solid enough to survive at $50 oil prices.

But behind that story is that E&P spending is continuing to be eviscerated in the U.S. As one analyst put it, 20% cutbacks have lost their shock value. By summer another surprise might be in store as companies cut what seemed in January to be invulnerable: production.

Ultimately, lower production will help balance out the oversupply that is depress- ing prices. Until then, shale success largely depends on where operators drill.

Three distinct sub-plays—Springer in the Midcontinent, Karnes Trough in the Eagle Ford and Nesson Anticline in the Bakken—generate at least a 10% internal rate of return (IRR) at a $50/bbl flat real West Texas Intermediate ( WTI ) price, according to a report by Wood Mackenzie.

E&Ps are continuing to trim spending as oil prices languish near $50/bbl. By the second half of the year, some companies won’t be able to maintain their current capex and production will start to descend, too, an analyst said.

U.S. producers appear to be bearing the brunt of capex cuts.

The Lower 48 “clearly stands out as an area where capital spending in 2015 is experiencing an utter collapse,” said Pavel Molchanov, analyst, Raymond James.

Worldwide, budget cuts have been staggering. A Raymond James survey of 34 top-tier U.S. and international companies found that all were cutting capex.

“Just these 34 companies wiped out $100 billion of 2015 spending,” Molchanov said.

Unconventional shale operators have shown they’re nimble enough to survive the freefall in oil prices. But the downturn has set spending levels back to 2010 levels.

--Darren Barbee

Ignore the light, focus on the tunnel

Industry veteran Jed DiPaolo, senior adviser to Duff & Phelps, underscored the down in downturn:

“This may be a three- to four-year issue. Make sure you have liquidity to 2018,” he advised the crowd at Duff & Phelps’ 7th An- nual Private Capital Conference in Houston. “You may just have to go to ’17, but I’m telling you—’15 and ’16—if you’ve got a balance sheet that is struggling, you need to do everything you can to get it repaired. And do it now because rates are low. If you can rework your deals, do it. As we get into the late ’15 and ’16, it’s going to be a lot harder to repair that balance sheet.

“Make sure you’re as conservative as you can be for as long as you can be and you’re going to make it through this, but don’t ex- pect it to end at the end of the year.”

The crowd’s stunned silence may have reflected discomfort with a forecast harsher than the consensus, at least so far in the oil price slump. But DiPaolo’s outlook, despite his blunt delivery, may not be that far from the mainstream approach.

John Kneiss, Washington-based director, government policy and legislative affairs for Stratas Advisors, a Hart Energy company, agreed with DiPaolo’s projection that the low price environment will likely persist for one to four years.

“It’s going to take a while for the overall global economy to grow sufficiently to take up the overhang on crude oil output. This should keep prices generally depressed, at least compared to recent markets of $100 plus,” he told Midstream Business.

And Jim Rebello, Houston-based managing director and energy lead, mergers and acquisitions for Duff & Phelps, shared this outlook with Midstream Business for 2015: “Prices are probably choppy, but really, focus on hunkering down, prepare for the worst and hope for the best, and be aware that it will likely be a two-year window before what people would perceive as a full recovery. Most supply-oriented downturns typically take longer than a year, and right now, there is no reason to believe this will be any different than any other downturn from a timing standpoint.”

The approach to follow may depend on whether an investor accepts that energy commodity prices are exclusively driven by the laws of supply and demand. DiPaolo does not. A former senior executive at Halliburton, he spent years working for Dick Cheney when the former U.S. vice president ran that company. DiPaolo thinks oil is also influenced by geopolitics.

“We’ve had two major recent financial downturns. You see it after 9/11 and you see it again in 2008 to 2009,” DiPaolo said. “Both were devastating, but they were short-lived because they were financial. These weren’t geopolitically influenced.

“When the Saudis dropped the price of oil back in ’85, look how long it took for the price of oil to really come back again to that same level—almost 15 years,” he said. “Geopolitical things are longer term. It just doesn’t happen like these financial rebounds.”

DiPaolo drew parallels between the current price downturn and Saudi Arabia’s actions in 1985.

“We are starting to see a bifurcation in OPEC into the ‘haves’ and ‘have-nots,’” he said. “If this is a prolonged geopolitical price war over market share, I question whether OPEC survives as we know it today.”

Two significant political issues in Washington were referenced by DiPaolo:

• An effort to lift the ban on exporting U.S.-produced crude oil; and

• The current nuclear pact being negotiated with Iran.

Lifting the U.S. export ban, DiPaolo maintains, would further increase supply in an already oversupplied marketplace, potentially provoking an OPEC response. An agreement with Iran, per the Iranian government, may result in as much as 700,000 bbl/d entering the market in relatively short order.

--Joseph Markman

Upstream rides public equity, private capital through storm

It’s not all doom and gloom in the energy market, not by a long shot. In fact, public equity valuations are “astounding,” Joe Gladbach, managing director, Jefferies LLC, said at Hart Energy’s 8th annual Energy Capital Conference in Austin.

“Looking at next 12-month EBITDA, companies are being priced equivalent to $80 WTI, right now,” he said.

“If you price them at Nymex, their multiples would be way off the charts. Implicitly, and none of the analysts will tell you this, but their consensus pricing is showing $80 flat. That tells you that everyone in the industry believes that $80/bbl is going to happen next year—so watch out.”

The stars of the show have been the public equity and debt markets and private capital, which have been “extremely robust,” he said.

Prior to Gladbach’s speech, crude prices jumped some 5% to top $52/bbl after Saudi Arabia hiked prices for crude shipments to Asia.

Summing up the less-than cheery energy fundamentals, Gladbach said, “M&A sucks, oil is coming back, we have more natural gas than we can consume in our lifetimes, and gas prices will stay down for a long, long time.”

On the other hand, “Everyone with a dollar in their pocket thinks they can be an opportunistic oil and gas investor,” he said, to appreciative chuckles from the audience of upstream financiers, advisers and producers. “We’re screening those so we can get the legitimate investors to the table. The capital markets are doing well and, once again, are saving our bacon.”

Gladbach, a geological engineer, said he was impressed by how rapidly the upstream industry has responded to the current downturn, the fourth he’s seen. He called the response from a capital structure and operational standpoint “quick and thoughtful.”

Drilling and completion optimization and service cost reductions are helping producers live to fight another day and “making plays still highly economic, particularly in the tier 1 onshore acreage.”

--Susan Klann

Recommended Reading

Operators Look to the Haynesville on Forecasts for Another 30 Bcf/d in NatGas Demand

2025-03-01 - Futures are up, but extra Haynesville Bcfs are being kept in the ground for now, while operators wait to see the Henry Hub prices. A more than $3.50 strip is required, and as much as $5 is preferred.

Dividends Declared Week of Feb. 24

2025-03-02 - As 2024 year-end earnings wrap up, here is a compilation of dividends declared from select upstream and midstream companies.

KNOT Offshore Partners Conducts Shuttle Tanker Asset Swap

2025-03-02 - KNOT Offshore Partners LP subsidiary KNOT Shuttle Tanker AS is trading shuttle tanker assets with Knutsen NYK Offshore Tankers AS, the company said Feb. 27.

NextDecade Plans 3 More Trains at Rio Grande LNG

2025-02-28 - Houston-based NextDecade continues to build the Rio Grande LNG Center in Brownsville, Texas, as its permits filed with the Federal Energy Regulatory Commission continue to go through the legal process.

EOG Resources to Begin Persian Gulf Wildcatting Onshore Bahrain

2025-02-28 - Multi-decade U.S. shale producer EOG Resources said it is confident the tight-gas resource is there and first gas will come online beginning in 2026.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.