A few months prior to his retirement in May, Saudi oil minister Ali Al-Naimi said hedging had changed the oil-market game. “This is not the 1980s,” he told IHS CERAWeek attendees in Houston. “We are dealing with a challenging market that is much more sophisticated and complex. There are a lot of new players and financial instruments that simply didn’t exist 35 years ago.”

The view seemed to be one that would have been better regarded by Saudi Arabia 15 months earlier. Tudor, Pickering, Holt & Co. Inc. (TPH) analysts summarized at September- end that, among producers they cover, 39% of their oil production for the balance of 2016 is hedged, up 7% from June-end, at a $56 per barrel (bbl) strip. 2017 production is 16% hedged, up 6%, at $53. They expected 2017 hedges to increase further during this quarter.

Since then, the January-contract intra-day WTI trading price grew to more than $52 after OPEC members suggested on Sept. 28 that they would cut output after their Nov. 30 meeting. On the bump, U.S. producers took on more hedges, according to derivatives advisors.

U.S. producers hedging at higher prices is “a trend that’s likely to be viewed with concern from Saudi Arabia to Venezuela,” Bloomberg reported in early October. “The clamor (among U.S. producers) to hedge … could translate into higher U.S. oil production next year, offsetting an (OPEC cut).”

A long-time operator told Investor, “Yeah, it’s not working out for them. They underestimated the U.S. producer this time.” He suggested that the Thanksgiving Day 2014 decision may have made for a runaway train; U.S. producers may have wrested away control of global oil prices for the first time since 1971.

Back then, the Texas Railroad Commission lifted output restrictions to demonstrate producers’ ability to remediate another OPEC embargo. The wells didn’t respond; Texas had shown its cards.

Thomas Marchetti, energy strategist and a managing director for Jefferies LLC, wrote on Oct. 31, “Saudi (Arabia) has clearly moved ahead of its skis, thinking they (are) not only in control of OPEC, but could balance the markets. I’ve stated repeatedly that I don’t expect a broad agreement being reached by OPEC or non-OPEC producers.”

Enter unconventional oil

When OPEC didn’t curtail its production in 1998 in response to oversupply, WTI fell to $10/bbl by year-end. U.S. producers were limited by their lenders at the time to hedging only what they were producing. However, most U.S. production was from conventional formations in relatively small fields compared with nearly whole-basin fields such as in the Permian today where tens of thousands of wells remain to be drilled.

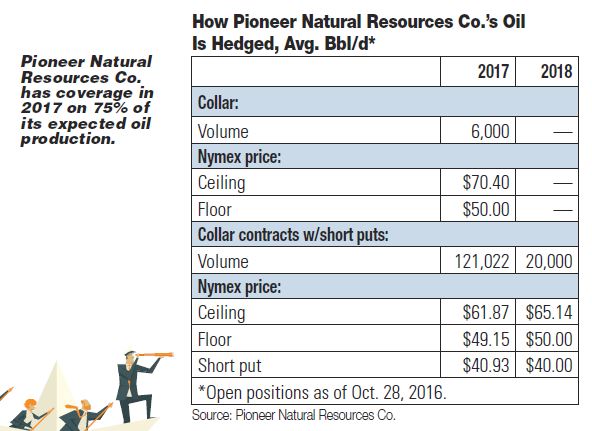

Pioneer Natural Resources Co. had 75% of its estimated 2017 oil production hedged at roughly $51 by October-end. Its second-quarter production costs were $8.36 per boe; lease operating expenses, $4.95.

Capital One Securities Inc. analysts’ covered producers have 21% of their oil hedged for 2017 on average, up from 16% in early 2016. Noble Energy Inc. increased its hedges for 2017 from 8% to 22%; Whiting Petroleum Corp., from 15% to 29%; and WPX Energy Inc., from 46% to 55%.

Have U.S. producers’ unconventional resource plays changed the game? “An emphatic ‘yes,’” Wayne Penello, president of Risked Revenue Energy Associates, told Investor. The shift has been from long-leadtime, expensive and super-risky projects, such as in the deepwater Gulf of Mexico, to producers being able to quickly bring on new wells from infill drilling onshore.

The producer with 50 DUCs (drilled but uncompleted wells) can hedge at $58 and bring them online. If the price falls to $48, more DUCs can be made, ready for the next upswing in the Nymex price.

“Now you have companies that have assets in the ground that,” Penello said, “if the price is right—and maybe not today, but the forward curve is right—‘I will just hedge that and have the confidence we will produce those volumes.’

“We don’t have a customer today that can’t hedge PUDs (proved, undeveloped reserves). Ten years ago, nobody could hedge PUDs; the banks wouldn’t let you. The U.S. E&P business has gone from a risky exploration business to a manufacturing business. It’s not like wildcatting.”

In March, Energen Corp. hedged 5.2 million 2016 barrels at $41.47 and 1.1 million 2017 barrels at $45.05. Clayton Williams Energy Inc. added hedges at between $41.18 and $44.30 on some 800,000 barrels.

Justin McCrann, president of Aegis Energy Risk, said, “Some producers can turn a profit in the low $40s; some of them break even in the high $30s.”

OFS-cost reflation

At a $58 oil price, there is risk that bringing those DUCs online will cost more than at $48, however, as other producers take the same tack. And making new DUCs will cost more to drill.

TPH analysts reported in late October that investors should pay attention to any earnings-call remarks about oilfield-service (OFS) costs. “A few operators have recently hinted in conversations that the pressure pumpers are testing the waters for a price increase,” they wrote.

“Further, we’ve already seen examples of sand pricing starting to move higher … and we expect demand to eclipse 2014 by the second half of 2017 and even bigger jumps might not be far off.”

They added, “With additional rig adds planned into year-end and corporates blowing down a large portion of their DUCs in 2017 … we think it is only a matter of time before the pricing dam breaks. As a reminder, from a macro-perspective, every 10% uptick in service cost raises breakevens by $5 a barrel; $60 may soon be the new $50.”

They estimate sand will cost some 3 cents a pound more next year in some areas. While that may seem like a small number, the analysts said, some wells are being completed with between 20- and 50 million pounds, so “this alone could add (some) $600,000 to $1.5 million to (well cost from sand alone).”

Simmons & Co. International Inc. managing director and head of E&P research Pearce Hammond reported that Pioneer and EOG Resources Inc. expect to grow their oil production through 2020 sizably at between $50 and $60. While neither has hedged its expected production growth, “one concern is that these plans incorporate insufficient oil-service- pricing relation,” Hammond wrote.

Subash Chandra, managing director and senior equity analyst for Guggenheim Securities LLC, said at Hart Energy’s DUG Midcontinent Conference in late October that 60% of operators’ cost reductions since 2014 are permanent via efficiency gains. If OFS prices reflate to the 2014 level, which he noted was an exceptional macro-environment, costs would be a net 30% below that of 2014.

Chris Croom, Aegis CEO, told Investor, “We’ve seen clients take into account the fact that service costs likely rise as the (oil-price) market rebounds. However, there should be some lag time in between. Most people we speak to aren’t expecting a dramatic increase in the short term. But we’ve heard some growing concerns in passing.”

Penello added that fears of higher OFS costs undoing hedge protection is “one of those great myths. Certainly, if oil prices go up, OFS costs will go up. But no one hedges 100%. The difference you’re making on your unhedged volumes will cover the increase in lifting costs. Rule No. 1, don’t over-hedge.”

Still, a producer who thinks his book is vulnerable could buy some of the upside back with out-of-the-money calls, he said. “Let’s say you like hedging at $43, but, if oil goes to $60, that hedge doesn’t work anymore. You have to embed into the structure perhaps a $55 call you paid $5 for and on a deferred-premium basis. If you have calls and prices are high, those calls should give you some relief.”

Penello also suggested trying to lock in OFS costs. “Why not address it at the contract level? Still, if you’re hedged correctly and your vendors don’t want to lock in a long-term rate, that issue goes away with calls.”

Bob DeMan, senior vice president, origination, for Arm Energy, said, “You’ve got to match the hedge to your production. At $50, you think you have a 20% rate of return, but, if the market goes to $60 and your service costs go up 10%, you don’t have a 20% rate of return anymore.”

All about the banks

Many banks are requiring minimum hedges of as much as 75% or more of PDP (proved, developed, producing) reserves to secure the mortgaged property. Croom said, “For years, all we ever dealt with were maximum hedge restrictions and very few instances of minimum requirements.”

Buddy Clark, Haynes and Boone LLP energy- practice chairman and author of Oil Capital, a history of financing U.S. oil and gas producers, said that, when hedging became available, “banks capped clients to no more than 85% of expected future production to prevent producers from being naked on their hedges.”

In this price cycle, “bankers and producers alike have seen the inherent value of hedging a floor on commodity prices. Unfortunately, the ‘lower for longer’ market has outlasted some of the hedge protections.”

While the Nymex price was in the $40s and low $50s in October, it was sub-$30 earlier this year. “Bankers know that prices could go even lower (than $40 again),” Clark said. As a result, they’re requiring minimum hedged volumes.

“Projected volumes from wells scheduled to be drilled—i.e., today’s PUDs—can be included in future hedge volumes,” he added. “So proven reserves are fair game, provided the producer has plans to actually drill and complete the projected volumes.”

Croom said that “in many deals we have seen, wherever the money is coming from—traditional lenders, mezz lenders, private equity— there are hedge minimums and many of them are significant. We’ve even seen 75%, 85%, 90% of PDP going out three to five years.”

Bankers have told him that, “‘We will never let what happened happen to us again. Period.’ For many of them, their primary concern is to make sure the economics work and they are highly secured to the downside.”

Jeff Nichols, a partner with Haynes and Boone, told Bloomberg in an article this summer, “These hedges are a huge part of the economic value of these oil and gas companies. And they are exempt from the bankruptcy code.”

A privately held producer told Investor in October that his bank agreement didn’t require minimum hedging, but he expected the requirement during redetermination. Vanguard Natural Resources LLC paid its bankers $66.8 million from hedge monetizations to address a reduced borrowing base in its 11th credit-agreement amendment. Legacy Reserves LP’s amended agreement mortgaged 95% of its oil and gas assets and requires 75% of projected production to be hedged through 2018.

Arm’s DeMan said, “We’re seeing the same thing. We take all the fundamentals and make our recommendation. But, what the banks and the investors are bringing forth, we have to comply with. The banks wanting 80% is very difficult and, a lot of times, they just want swaps too.

“A lot of times they say you have to hedge 80% and you can’t do it with puts. The banks are running the show right now.”

New U.S. Office of the Comptroller of the Currency rules were issued to bankers in March, but none of this has to do with that, he said. “The banks got burned. If they think they need 80% coverage to guarantee payment of interest and principal, that’s what they’re going to do.”

While the 80% is on PDP, there are risks, he added. “If a bank wants 80% hedged for five years, it’s not like you can lock in your drilling costs for five years. You’re taking an enormous risk if you lock 80% in at $50 and oil goes to $100.”

Many of the U.S. producers that are encountering these hefty minimum-hedge requirements from their bankers are small or privately held, Croom added. For these, locking in 75% or more at $50 may mean locking out a tremendous amount of upside.

Yet, without other, affordable capital sources, they’re accepting the requirements. “You’re going to do what you have to do,” Croom said. “Historically, many oil and gas companies have not liked to hedge. That may be the result of hedging at the wrong time or not having a plan to develop the portfolio going forward.

“But for many oil and gas companies right now, it doesn’t matter. Whatever the money says to do is going to get done.”

As for private equity providers and mezzanine lenders, which earn equity on any upside, why are they requiring minimum hedges as well? Aegis’ McCrann said private equity investors figure they will get their return from a rising oil price that will increase the value of the investment, while the hedges protect the value against the downside.

“Their whole goal is to exit,” McCrann said. “If there is a run-up in the market, the asset appreciates and that’s going to be the payout.”

Penello agreed. “The goal is to prove up reserves and that’s where the value is.”

Croom added that some prospective private equity investors bought producers’ debt earlier this year, instead. In February, Chesapeake Energy Corp.’s notes due 2022 were trading at 11 cents; in late October, 86 cents. Croom said, “Private equity investors’ attitude was ‘We could get a better return just buying the bonds.’”

Political risk

And the producer’s ability to deliver the promised production? Investor visited with DeMan, Croom and Penello prior to the Nov. 8 election. DeMan said political risk “is massive.”

What if a producer has hedged expected production from completing DUCs or via new drilling “and fracking is banned?” Also, “the market’s going to rally because U.S. production has dropped. Your hedges are going to go underwater.”

In addition, new pipeline projects—from North Dakota to New England to Georgia— were encountering myriad regulatory and legislative impasses. “We just saw another one delayed in the Marcellus,” DeMan said.

Croom said the risk is mitigated if what is hedged is only PDP and takes declines into account.

Meanwhile, McCrann said, many producers remain reticent to hedge at $50. “There is emotional overhang present in the market right now because of (sub-$30) prices in the first quarter. Producers need to get past the panic and focus on what’s ahead of us when making decisions on the hedge portfolio.”

Penello said hedge protection in a low-price environment, although painful, is more essential than in a high-price environment. “At $80, you have a lot of room. If the price goes down $10, you’re not making the money you like, but you’re still making money.

“But, if your $50 goes down to $40, you might be underwater in your cost structure. Hedging is more important today than it has been at any time in the last five years.”

Recommended Reading

Entergy, KMI Agree to Supply Golden Pass LNG with NatGas

2025-02-12 - Gas utility company Entergy will tie into Kinder Morgan’s Trident pipeline project to supply LNG terminal Golden Pass LNG.

Trinity Gas Storage Adds Texas Greenfield Gas Storage Complex

2025-01-20 - Trinity Gas Storage has opened a 24-Bcf gas storage facility in Anderson County, Texas, to support the state’s power grid.

ONEOK, Enterprise Renew Agreements with Houston’s Intercontinental Exchange

2025-01-29 - ONEOK and Enterprise Product Partners chose to continue their agreements to transfer and price crude oil with Houston-based Intercontinental Exchange.

Tidewater Sells Canadian Roadway Network for CA$24MM

2025-03-06 - Canadian midstream company Tidewater Midstream and Infrastructure plans to use proceeds to pay down debt.

WaterBridge Starts Open Season for Produced Water Pipeline

2025-04-01 - Water midstream company WaterBridge plans to develop transport capacity out of the Delaware Basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.