ONEOK currently owns NGL egress capacity out of the basin but does not own gas processing plants in the area. (Source: Shutterstock/ ONEOK)

ONEOK’s (OKE) latest billion-dollar move to strengthen itself as a Permian Basin midstream player fills in some market sector gaps, according to analysts. And executives pulled it off without damaging the company’s credit quality rating.

ONEOK announced an overall $5.9 billion deal for a controlling interest in midstream companies EnLink Midstream (ENLC) and Medallion Midstream on Aug. 28, giving the company a fully integrated Permian Basin platform that will secure traffic on its pipelines out of the country’s most productive play.

“The acquisition is an entry for OKE into the Permian, which investors have been asking about for some time now,” said Ajay Bakshani, director of midstream equity at East Daley Analytics (EDA).

On Aug. 27, the day before the deal was announced, EDA published an analysis that recommended ONEOK purchase EnLink to guarantee traffic on its NGL network. ONEOK currently owns NGL egress capacity out of the basin but does not own gas processing plants in the area.

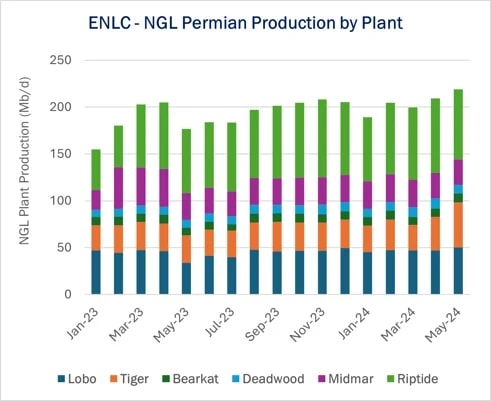

ONEOK is already expanding its NGL egress capacity out of the basin from 190,000 bbl/d to 380,000 bbl/d, in a project that could be completed by the end of the year, according to East Daley. EnLink’s Permian plants produced about 220,000 bbl/d of NGLs in May.

“Although OKE owns an NGL pipeline out of the basin (West TX NGL Pipeline), it never had a bigger presence and actively invested significant capital in America’s premier basin,” Bakshani said.

The strategy is not new. Most midstream merger activity over the last year resulted in large companies seeking to bolt-on gathering and processing (G&P) facilities in a shrinking and competitive Permian market.

ONEOK’s move stands out, however, as it involves all of EnLink’s assets in the south-central U.S. as well as Medallion, a crude-specific midstream company.

The Medallion acquisition shores up ONEOK’s position as a crude carrier in the Permian. Medallion is the largest privately owned crude midstream company in the region, with a footprint of more than 1,300 miles of pipeline and storage facilities, primarily in the Midland Basin.

In a conference call the day after the deal was announced, ONEOK President and CEO Pierce Norton described the Medallion deal as “feed and fill.”

“The feeding part gives us security of supply, and the fill part means that the capacity of our integrated assets would be full,” Norton said.

The company’s acquisition of EnLink’s entire system, which includes assets in north and southeast Texas, Louisiana and Oklahoma, fits into ONEOK’s network for the same reasons. The EnLink NGL network is already well connected to ONEOK.

“[EnLink’s] Anadarko G&P system primarily feeds OKE NGL pipelines already, but it is a more active system than OKE’s legacy Anadarko system,” Bakshani said. “ENLC also has a Y-grade pipe (Cajun Sibon) that connects Mont Belvieu [in Texas] to its Louisiana fractionation hub. OKE could leverage those assets and provide additional downstream connectivity, playing into.”

The Easton Energy acquisition, one of several deals over the last year, has made ONEOK into one of the fastest-growing midstream companies in the U.S.

In May 2023, ONEOK made an $18.8 billion deal to acquire Magellan Midstream Partners LP, one of the largest companies in the U.S. sector. Twelve months later, the company bought Easton’s NGL pipeline network in Southeast Texas for $280 million. In July, the company announced it was expanding a refined products pipeline to the greater Denver area in a $480 million project.

Financially, ONEOK’s credit rating from capital market company Fitch was left undamaged from the Aug. 28 deal announcement.

“Scale matters in the midstream sector, and OKE will be adding roughly $1 billion in annual EBITDA (based on OKE owning 43% of EnLink) to its existing roughly $6 billion in base EBITDA, based on Fitch’s calculation and existing assumptions,” the company wrote in an analysis of the deal. “Should OKE acquire 100% of EnLink, the EBITDA contribution could be closer to $1.75 billion.”

During the press conference, ONEOK executives said the company is planning to pursue the remainder of EnLink’s common units through a tax-free exchange for OKE’s shares.

The transaction will increase ONEOK’s leverage as the company takes on incremental debt and assumes EnLink’s unsecured debt. Fitch expects ONEOK’s leverage to increase to close to 4.0x, below Fitch’s negative leverage sensitivity of 4.7x.

“Fitch considers the diversification benefits, as well as increased scale and potential synergistic opportunities, to be offset by higher expected leverage,” the analysis said. “All of this leads to Fitch’s estimation that this transaction is neutral for OKE’s credit profile.”

Recommended Reading

ADNOC Explores $9B Acquisition of Aethon’s Haynesville Assets—Report

2025-04-11 - Abu Dhabi National Oil Co. (ADNOC) is evaluating an acquisition of natural gas assets from Aethon Energy Management valued at around $9 billion, Bloomberg reported April 11.

FTC May Reconsider Hess, Sheffield Bans on Holding Board Seats

2025-04-11 - The Federal Trade Commission has announced it is seeking comment on potentially rescinding bans on Pioneer Natural Resources’ Scott Sheffield and Hess Corp.’s John Hess from serving on the boards of companies that acquired their E&Ps.

CRTS Global Secures RAE Energy’s Coatings Business

2025-04-10 - Voyager Interests portfolio company CRTS Global is growing in the pipeline coatings market with its acquisition of RAE Coatings, a provider of protective external coatings for offshore pipelines.

Abu Dhabi’s Mubadala Buys Stake in Kimmeridge Shale Gas, LNG Ventures

2025-04-10 - Mubadala Energy, owned by Abu Dhabi’s sovereign wealth fund, is buying a stake in Kimmeridge Texas Gas (KTG) and Commonwealth LNG as the United Arab Emirates company makes an entry into U.S. shale.

SBM Offshore Signs $400MM Sale and Leaseback for FPSO Cidade de Paraty

2025-04-09 - SBM Offshore holds a 63.125% interest in FPSO Cidade de Paraty, located offshore Brazil.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.