Over the course of the last six years or so, U.S. shale production has drastically changed the landscape of how supply meets demand and what those dynamics must be to achieve global market equilibrium. When commodity prices increased dramatically in 2011, there was a rush to enter the domestic shale plays, where operators then began focusing on optimizing drilling techniques and establishing a large inventory of wells. Despite this rush, there was—and still is— a significant need to monitor and maintain the global supply and demand balance. Increased production from onshore shales combined with other lucrative supply sources, as well as the recovering global economy, all worked to widen the gap between the world’s supply and its consumption needs.

The Permian Basin is one of the oldest producing regions in the U.S. and is often regarded as the workhorse of the shale plays. With its first wells drilled in the 1920s, the basin has produced billions of barrels from legacy wells. It benefits from established infrastructure throughout the region, easy access to the Gulf Coast and multiple productive target zones. Within the Permian, three well-known formations contribute to its success: the Spraberry, Wolfcamp and Bone Spring.

Since 2009, it is estimated that 75% of the production increase within the basin can be attributed to these specific formations. Historically, the Midland sub-basin has been the more actively drilled area and most cost-competitive. However, operators have begun to move more heavily into the Delaware sub-basin, where they are garnering more productive well results and better economics.

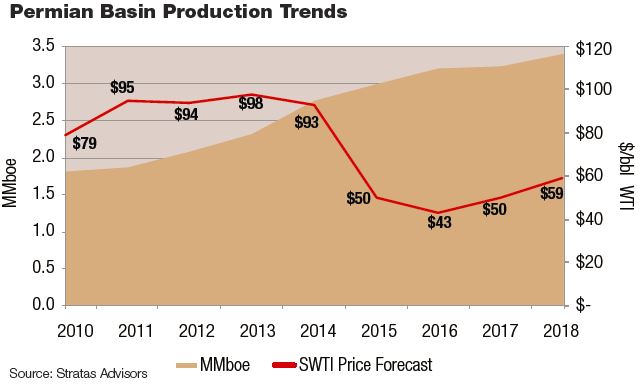

The Permian has weathered the initial downturn in market prices since the end of 2014 very well, beating many production estimates, and it continues to outpace other regions in terms of output. However, despite the overall production increases, the basin has begun to show minor month-over-month declines since April 2016. Even though these declines have begun only recently, Stratas Advisors projects that the basin will continue to show year-over-year growth from 2016 to 2017. We estimate that market prices will increase to average approximately $50/bbl WTI in 2017, with 2018 expected to recover further to average close to $60/bbl.

When we compare the median well-level economics from 6,800 wells across the basin and rank them by vintage, the median breakevens have continuously trended downward since 2012. Currently, the average breakeven across the basin ranges from about $54/bbl to $64/bbl. When focusing on the top 25% of these wells by economic and production performance, the median breakeven decreases to about $30 to $33/bbl. Under market conditions fluctuating between $40 and $48/bbl, the top 25% of wells drilled within the Permian remain economic.

Whether focusing on the Permian or other shale basins across the U.S., it is increasingly paramount to concentrate within the “core of the core” acreage in order to achieve economic returns and generous well results. The Permian offers unique opportunities for producers within the region, with the core counties producing a median breakeven below $40/bbl for the top 25% of wells drilled. As operators continue to drill more efficient wells with much larger returns, we expect to see the basin continue its production increase and lead the industry in its recovery.

Stratas Advisors projects that the Permian Basin will continue to show year-over-year production growth from 2016 to 2017.

Recommended Reading

Small Steps: The Continuous Journey of Drilling Automation

2024-12-26 - Incremental improvements in drilling technology lead to significant advancements.

Aris CEO Brock Foresees Consolidation as Need for Water Management Grows

2025-02-14 - As E&Ps get more efficient and operators drill longer laterals, the sheer amount of produced water continues to grow. Aris Water Solutions CEO Amanda Brock says consolidation is likely to handle the needed infrastructure expansions.

Momentum AI’s Neural Networks Find the Signal in All That Drilling Noise

2025-02-11 - Oklahoma-based Momentum AI says its model helps drillers avoid fracture-driven interactions.

Pair of Large Quakes Rattle Texas Oil Patch, Putting Spotlight on Water Disposal

2025-02-19 - Two large earthquakes that hit the Permian Basin, the top U.S. oilfield, this week have rattled the Texas oil industry and put a fresh spotlight on the water disposal practices that can lead to increases in seismic activity, industry consultants said on Feb. 18.

Microseismic Tech Breaks New Ground in CO2 Storage

2025-01-02 - Microseismic technology has proved its value in unconventional wells, and new applications could enable monitoring of sequestered CO2 and facilitate geothermal energy extraction.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.