This year’s DUG Permian showcase opened with a midstream emphasis. The fi rst day of the Hart Energy conference and exhi-bition in Fort Worth, Texas, featured a pre-conference program focused on a wide range of topics related to gath-ering, processing, transportation and storage in the big play.

In his keynote presentation, former INGAA Foundation chairman and Sunland Construction CEO Craig Meier saluted the midstream sector for its can-do attitude.

“Our industry is very resourceful on how to get the necessary infrastructure built to get the oil and gas out,” he told a full house of attendees. However, that resourcefulness is being tested as the impact of lower oil and gas prices has created economic uncertainty moving forward, Meier noted.

INGAA Foundation study

The primary focus of the presentation was the results of the latest update of the INGAA Foundation’s regular infrastructure study, “North American Midstream Infrastructure Through 2035: Leaning into the Headwinds,” released in April.

“We do our infrastructure study every two to three years,” said Meier. “We started it in 1993 to look at natural gas and expanded it over the years to look at oil, NGL and other products, and not just the Lower 48, but all of North America.”

The study, he explained, is “basi-cally a model of the market and supply, showing where assets need to go and at what quantities, based on assumptions.” The lower commodity prices cur-rently facing the industry prompted the foundation to take an approach different from the one it utilized in earlier versions.

“Typically, we do the most probable case when we do the study,” he said, “but this year, with the commodity prices in flux, we decided that it would be best to bookend the study with an optimistic case and less optimistic case—a high and a low case.”

General conclusions from the study are promising.

“Future infrastructure development is significant, but down from the last five years,” he said. “Key uncertainties are eco-nomic activity and commodity prices.”

Projected total capex for midstream infrastructure over the 20-year period covered will be approximately $450 billion in the low case to $600 billion in the high case, according to the report.

The largest share of gas-related capex of the projected $353 billion for new infrastructure over the next 20 years in the high case would occur in the southwest region (Texas, New Mexico, Oklahoma, Louisiana and Arkansas), which includes the Permian. It is expected to total $112 billion throughout the projection period, with $54 billion being spent for LNG export projects, according to the report.

Oil infrastructure

The region also is expected to see the largest share of crude oil-related capex, projected at $190 billion, for new infrastructure in the high case to total $96 billion, with $82 billion being spent for lease equipment, according to the report.

“New gas transportation capabilities, the miles of natural gas interstate pipeline, are somewhere over 1,000 miles a year,” Meier said. “You add in midstream, NGL, oil and gathering, you get 11,000 miles to 14,000 miles of pipe to be installed. As for horsepower, the study projects 650,000 horsepower per year to 930,000 horsepower per year needs to be installed.

“Doing some quick math, assuming somewhere around 8,000 horsepower a station … we’ve got to install an excess of 100 compressor stations annually across the United States. It’s a little easier when they are 1,000 horsepower units, but a lot more challenging in expertise when you are building 20,000 horsepower or 40,000 horsepower compressors.”

Fixer uppers

In his opening presentation, Bryan Neskora, COO and founding partner of Navitas Midstream Partners, told attendees his firm is not afraid of taking on fixer-upper projects if they are in the right neighborhood—and the Permian is definitely the right neighborhood. “A lot of people are starting to look at the potential of the Permian Basin not in terms of years but in terms of generations,” Neskora said. “If we see a significant increase in commodity prices, I think you’ll see even more activity return.”

Poised to grow along with partners such as Encana Corp. and Apache Corp., the midstream sector is better preparing itself for what heads its way. For Navitas, opportunities lie in greenfield sites and acquisitions, even if the assets are in need of repair.

The two-year-old company last year acquired gas gathering and processing assets—including about 1,000 miles of low- and high-pressure gas lines and two cryogenic processing plants with a combined capacity of 65 million cubic feet per day (MMcf/d) serving Spraberry producers.

Neskora likened Navitas’ Midland Basin Spraberry system, which serves Texas’ Martin, Midland and Glasscock counties, to a fixer-upper house in a good neighborhood. “We’re replacing and doing engine swings on all of our compressor stations,” Neskora said, not-ing the company added 11,000 horse-power of new compression at its existing stations, plus a new station in northeast Martin County.

“New compression, keeping field pressures low and keeping compression on, is one of the key things that we’re trying to do to make our systems more reliable. In addition to that, we’re also replacing our high-pressure trunk lines. So we are really building a new spine on the Spraberry,” he said.

“We’re making a lot of hay get-ting ready for the return of drilling,” Neskora said.

Future growth

Navitas isn’t the only midstream oper-ator preparing for the future growth the INGAA Foundation study projects. EnLink Midstream is busy expanding compression options and improving infrastructure as it eyes producers’ suc-cesses in the field, said Andrew Deck, senior vice president, Permian Basin.

EnLink has invested more than $1.1 billion in the Permian Basin over the last 18 months, including acquiring mid-stream assets from producers. Among the latest was EnLink’s 2015 acquisition of Matador Resources’ gathering and processing assets in the Delaware Basin for about $143 million and acquisition of a 50% ownership interest in the Deadwood processing plant from a sub-sidiary of Apache for about $40 million.

As prices improve, the midstream sector must be prepared to handle growing production with infrastruc-ture investment, emphasized Deck. He referred to initial production rates of 800 to 1,600 barrels of oil equivalent per day, encouraging spacing tests, breakev-ens that have dropped from $80-$90 per barrel (bbl) to $30-$40/bbl, technology improvements and the inventory of drilled but uncompleted wells.

“Over the last 18-24 months, pro-ducers have drilled wells twice as fast, they drilled wells at half the cost and wells generally have about twice the reserves as they used to have,” Deck added. That’s about four times the reserves for the same capital investment.

“As the challenging conditions are showing signs of improvement, I’m confident we will emerge smarter and stronger,” he said. “The infrastruc-ture requirements are going to grow significantly, and this growth is best accomplished through partnering rela-tionships between midstream and pro-ducing companies.”

Stretched infrastructure

Deck recalled in 2011-2012 when the first wave of incremental production came on and outstretched existing infrastructure in the Permian.

“We all watched a lot of gas being flared, and we wondered if our plans associated with growing a successful business were going to be derailed by lag-ging midstream infrastructure,” he said.

“Planning and partnering are going to be essential for us to be successful,” Deck added. Takeaway capacity is not a major concern right now, but that is not the case with gathering infrastructure— primarily low-pressure piping and com-pression used to aggregate volumes.

“Timing is going to be essential going forward,” Deck said, adding mid-stream companies should think about tasks such as:

• When to order equity units in advance to get them in place on time;

• Leasing or contract service options; and

• Deciding whether to have fewer and larger stations available or more and smaller stations spread

across the producing area. EnLink’s interconnects on the low-

and high-pressure sides for greater reliability, he noted.

Setting a standard

Echoing that fewer-and-larger versus more-and-smaller conundrum, a panel of two gas processing experts asked: Do you go with an off-the-shelf design that’s cheaper to build but potentially less efficient—or do you custom design a facility, making it more costly to con-struct but more efficient?

“The question is, which battles do you choose to fight when you choose one or the other?” asked Chuck Laughter, vice president of engineering and operations for Joule Processing. And someone needs to define just what a standard design is, he noted.

“So what is a ‘standard’ facility? It’s the same as last time, except… ,” he added with a chuckle, his voice trailing off.

It’s important to remember that about one-third of any gas plant is standardized, Laughter said. The additional two-thirds of each design, however much it may or may not be customized, depends on a customer’s needs and wishes. Standardized designs can be applied to a plant’s major equip-ment kits, including incoming gas stabilization and treating. A plant may also have fairly standard processing and compression needs. Utility needs may be fairly common too.

Customization typically applies to site preparation and civil engineering that addresses such issues as drainage and soil composition and details for construction staging. The most tweak-ing, however, will involve inlet volumes and pressures, the composition of the inlet gas stream and potential fluctua-tions in inlet composition over time as the producing field matures. Also, the customer’s desire or need to fine-tune recovery of each of the gas liquids can make big differences.

Integration focus

Standardization provides the advantages of well-defined and proven equipment virtues that are offset by potential de-rating of plant efficiency and prod-uct specification. Standardization allows the designer and customer to focus easily on integrating the multiple pro-cessing packages that make up a plant, creating a seamless, smooth-running operation, Laughter said.

Customization can complicate a project because it requires engineering optimization for a specific situation. That may require different vendors and dif-fering operating specifications. The aim of customization is to focus on potential operating expenditures and the expense of construction and design to provide a better return on investment for a build-to-suit facility, Laughter added.

“You’re probably going to have to work through some one-off issues” in a custom design, “a little different blend of issues,” he added.

John Mak, technical director-engineering and senior fellow for Fluor USA, then gave the audience several examples and a case study of when and how a customized design makes economic sense.

His examples compared a standardized cryogenic design to reflux (recirculating) or custom-cryogenic designs. He explained that customized designs may be worthwhile for plants built to treat rich-gas streams—where the plant’s fee gas stream can yield more than 6 gallons of gas liquids per thousand cubic feet—or there is a need for higher inlet stream pressures, greater than 1,000 psi.

His examples compared a standardized cryogenic design to reflux (recirculat-ing) or custom-cryogenic designs. He explained that customized designs may be worthwhile for plants built to treat rich-gas streams— where the plant’s fee gas stream can yield more than 6 gallons of gas liquids per thousand cubic feet—or there is a need for higher inlet stream pressures, greater than 1,000 psi.

Ethane

Mak discussed the attri-butes of Fluor’s Advanced Deep Dewpointing Process, which can increase propane recovery using an ethane reflux process at lower feed-gas pressures without a turboexpander. Or, it can increase ethane recovery using a methane reflux.

He provided a case study that cov-ered specifics of one Fluor customer’s “gas plant that has been operating quite well for 20 years” with a potential 95% ethane recovery, although Mak did not specify which plant due to confidentiality concerns.

Laughter closed the panel by noting that design and approval timing var-ies with the amount of customization a customer requires—an important cost component. A stan-dard, off-the-shelf design might take as little as nine to 10 months. But “it can take longer as you weave more and more prefer-ences, or company stan-dards and specifications, into the mix,” he added, and a fully cus-tomized plant might take 18 months to design due to additional review and approval steps.

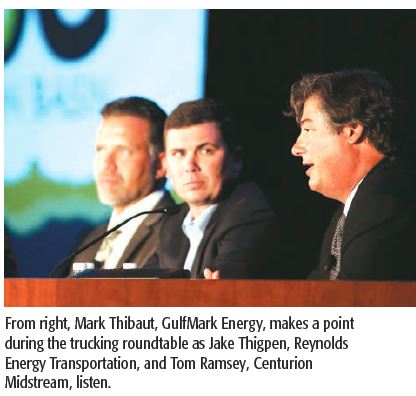

Keep on trucking

Trucking provides the first link in midstream’s value chain in most pro-ducing areas, including the Permian. Three transport industry executives discussed the play’s trucking needs for the conference.

“The supply of crude and the contin-ued supply out of the basin remains rel-atively strong compared to other basins,” said Tom Ramsey, CEO of Centurion Midstream LLC. “Obviously, driver demand is fairly high. The Permian’s been producing for so long we’ve got a long lineage of drivers; getting drivers in the new basins was somewhat difficult.”

“It’s kind of a no man’s land out there when you’re talking about the volume of just people—there’s not a lot out there to draw from,” added Jake Thigpen, general man-ager and COO of Reynolds Energy Transportation. “Your cost of doing business out there is so much higher, not only to get the employee out there, but the housing. Any costs that you have of doing business, period, are multiplied in the Permian for the fact that nobody lives there.”

And hiring a truck driver is not the same as adding an accountant to your team at the home office. “The thing about truck drivers is that they’re a rare breed,” Mark Thibaut, vice president of crude oil acquisitions at GulfMark Energy Inc., said. “They’re kind of loners and inde-pendent. A lot of them—it’s not that they have an unstable work history; it’s just that they shop around to see who’s got the best pay package.”

“That’s a really, really good thing for the Permian,” Thibaut said, citing EnLink and other midstream operators.

“They’re putting in stations that are close to the production, and that really helps with takeaway.”

Safe and secure

The energy business—like most sectors of society—faces significant security risks nowadays, according to a two-member panel that explored safety issues for midstream players. Suppose a company is going about its business.

Council, industry operators and mem-bers of the state legislature to get a bill passed to increase penalties for theft associated with oil- and gas-related equipment, specifically the theft of oil and condensate.

“That’s real money—a billion dollars out of our economy taken away from us by organized crime,” Ream said. “It’s a combination of American-based crim-inal organizations and Mexican cartels, as well as Russians and Chinese and a lot of different organizations, that are targeting the United States and target-ing our critical infrastructure for theft, fraud and misappropriation.”

“Because [these criminals are] not just stealing equipment; they’re trading in that equipment across the regions. You’ll have equipment stolen in the Permian Basin that shows up in the Bakken. You’ll have equipment that’s stolen in the Marcellus and resold in the Permian Basin or maybe even in the Eagle Ford. This is not single individuals taking advantage of circumstances. This is organized activity,” he added.

“In the world of SCADA control [and] distributable industrial control systems, the improvement in technology, The three panelists were proud of their companies’ ability to retain the bulk of their experienced driver workforce, thanks in part to compar-atively high pay, benefits and safety and signing bonuses.

Chuck Laughter, left, vice president of engineering and operations for Joule Processing, and John Mak, technical director and senior fellow with Fluor USA, discussed the pros and cons of off-the-shelf processing plant designs versus customization.

Lower turnover

“That’s on top of other incentives that we provide, so our turnover actually, in the last 18 to 24 months, has been quite low,” Thibaut said. “We’re very proud that we’ve been able to retain a lot of true professionals out there driving for us.”

Among the advantages that the Permian boasts is its longevity. For Thigpen, that means more experienced producers who know how to work with haulers. For Ramsey, it means more sta-tions and fewer long hauls.

All three panelists lauded how pipe-line locations in the Permian Basin have been moved closer to production fields, leading to shorter hauls and higher take-away of product.

Then suddenly, there is a blackout; all of its IT infrastructure has been hacked and corrupted. Elsewhere, an operator returns to the field and discovers equip-ment has been stolen.

Thank organized crime, which has been going on for a long time and con-tinues today, according to Robert Ream, chairman of the U.S. Energy Security Council, a partnership between state, local and federal law enforcement. “It’s a complicated activity. It’s complex, and it happens every day. Even with the downgrade in our commodity prices, the criminal activity remains.”

Ream, along with PetroCloud CEO Lance White, addressed how to combat criminal activity.

Ream added the industry needs to be speaking about resiliency rather than redundancy, saying the Texas energy industry lost $1 billion to theft

in 2014, according to the Texas attorney general’s office. He spent the last legis-lative session in Austin, Texas, working with colleagues at the Energy Security and specifically around communications, has enabled us to add systems to the field where previously they weren’t viable.

These systems allow us to improve our situational awareness,” Ream said.

The Internet of Things (IoT) is the next “big step forward,” according to White. IoT works to integrate multiple electronic systems and relies more heav-ily on software rather than hardware.

“We’re actually integrating all of these devices and all of these data at the field level. It’s kind of a paradigm shift,” he continued. “It opens up cross-func-tional access to data. We’ve got opera-tions centers, personnel, managers [and] we’ve got business functions like secu-rity, etc. that all have access to the same platform and various systems.

“Plunging us into darkness would be a catastrophic event,” Ream concluded. “Over the coming years as technology becomes more and more embedded

in how we live our lives and work our systems, you’ll see the impact of that become ever more present.”

Recommended Reading

Utica’s Encino Adds Former Marathon Director to Board

2024-12-16 - Brent J. Smolik, who most recently served on Marathon Oil’s board until its merger with ConocoPhillips, will join Encino Acquisition Partners as a director.

Ovintiv Names Terri King as Independent Board Member

2025-01-28 - Ovintiv Inc. has named former ConocoPhillips Chief Commercial Officer Terri King as a new independent member of its board of directors effective Jan. 31.

Utica Liftoff: Infinity Natural Resources’ Shares Jump 10% in IPO

2025-01-31 - Infinity Natural Resources CEO Zack Arnold told Hart Energy the newly IPO’ed company will stick with Ohio oil, Marcellus Shale gas.

Liberty Energy Appoints Arjun Murti to Board

2025-01-23 - Arjun Murti has over 30 years of experience as an equity research advisor.

Buying Time: Continuation Funds Easing Private Equity Exits

2025-01-31 - An emerging option to extend portfolio company deadlines is gaining momentum, eclipsing go-public strategies or M&A.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.