Notable basins throughout the U.S. have remained resilient through the shale industry’s first real downturn, such as the Permian Basin and Marcellus, but there have been drastic declines in other smaller basins such as the Panhandle area and the Rockies. Operators across the industry are turning to a strategy that is heavily weighted toward completions and are focusing on determining the best practices for increasing well recoveries while still making efforts to drive down costs.

Drilling activity

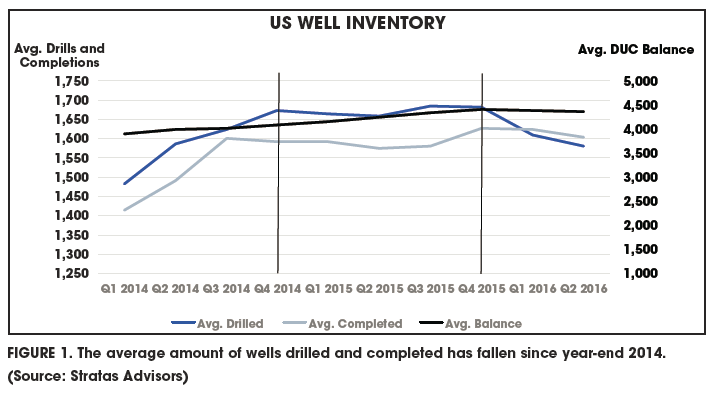

Figure 1 highlights the profiles of historical drilled and completed wells as reported by the Energy Information Administration. Clearly, the number of wells drilled dropped after the price of oil fell in late 2014. Things seemed to pick up a bit in mid-2015 before sliding considerably. Completions, on the other hand, reflected an immediate change in activity and really didn’t pick back up until late 2015, building a relatively healthy balance of uncompleted wells. In contrast to drilling, operators have maintained a relatively strong appetite for completing wells, reflecting a need to continue operating but doing so while spending far less. Between first-quarter 2014 and fourth-quarter 2015 the number of drilled but uncompleted wells (DUCs) increased about 13% across all basins.

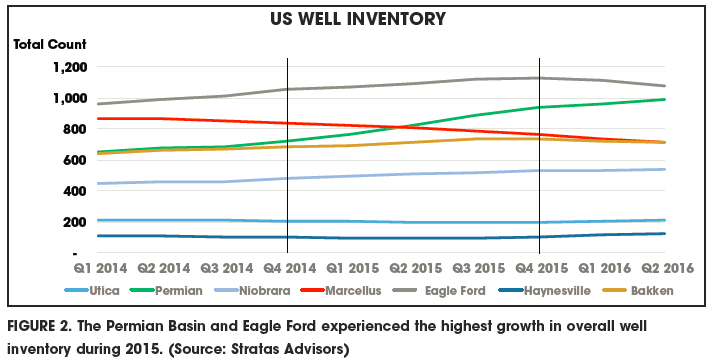

To gain an understanding of where this activity is located, Stratas Advisors analyzed the same information at a play level. Figure 2 illustrates that the highest increases were in the Eagle Ford and the Permian Basin. By the end of first-quarter 2015, DUC inventories in these areas posted year-over-year growth figures of 34% and 83%, respectively. The higher figure in the Permian Basin speaks to the huge draw from the Delaware and Midland basins, where operators were drilling their high-graded acreage in anticipation of a future rebound in prices. In contrast to the sustained activity in the southwestern Texas region, the DUC count in the Marcellus area dropped by about 16% over the same time period as drilling activity declined slightly in first-quarter 2015, but completions increased in an effort to continue filling the northeastern gas demand.

Production

Given the drop in commodity prices, the production has naturally been slowing down from the historic gains the U.S. was experiencing relating to the “shale gale.” While the natural gas basins have not declined quite as much, several notable oil and liquids-rich areas have taken bigger hits, with some reports noting declines in a few of the smaller plays at more than 80%. This often has been coupled with many of the existing operators declaring bankruptcy or selling out of their producing assets altogether, as seen within the Panhandle and other regions of north Texas and Oklahoma.

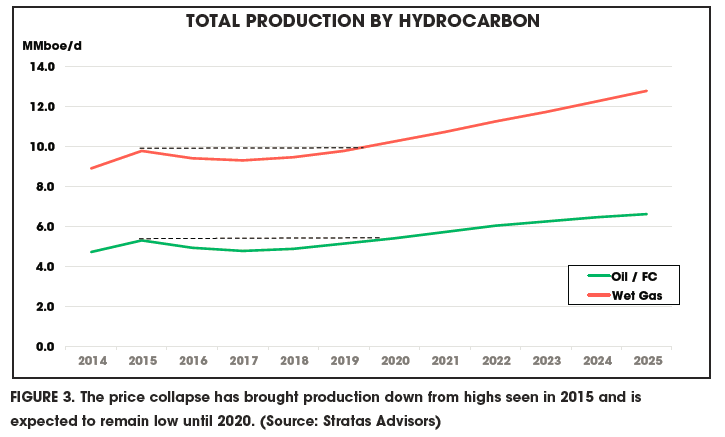

Notwithstanding the drop in production, “shale resiliency” often is referenced when considering global oil and gas markets post-price collapse. While reported figures have shown a clear turn for the worse, especially in certain plays, the consolidated impact is markedly less catastrophic than the dire predictions for which many in the industry had been bracing. As illustrated in Figure 3, total production in 2016 is expected to close out at about 5% lower than 2015 levels. Compared to the massive increases to which the world had grown accustomed, this drop is indeed material. However, given that prices have been cut in half, a decline of a mere 5% is something to respect, if not applaud.

With respect to prices, Stratas Advisors believes that global demand will support a gradually increasing price for West Texas Intermediate (WTI). Stratas Advisors believes the price of oil in Cushing will average between $48/bbl and $55/bbl in 2017 and will continue to slowly increase in real terms thereafter. At those prices there are several opportunities in shale for investors to capture value. Furthermore, operators are continuing to make impressive advancements in drilling techniques and methods, and they are making these improvements at continually declining costs.

The combination of a reasonably elevated price deck and a lower cost per extracted barrel provides sufficient support for a long-term production profile that is increasing. Stratas Advisors expects the rate of production to decline through the rest of 2016 and into first-half 2017. Stratas Advisors then expects it to reverse this pattern starting in mid-2017. At that time, Stratas Advisors forecasts WTI to be about $55/ bbl and forecasts total production to average slightly more than 14 MMboe/d. The rate of increase Stratas Advisors forecasts thereafter means production would not return to the peak rate that was experienced in 2015 until at least 2020.

Figure 3 illustrates how the price collapse is anticipated to take a toll on current and near-term production for oil and gas. The major crude oil- and condensate-bearing regions are estimated to produce about 4.9 MMbbl/d in 2016, which represents an 8% decrease from the 5.3 MMbbl/d recorded in 2015. Stratas Advisors expects crude and condensate production to decrease by another 2.9% in 2017 before starting to increase in the longer term. Declines in gas will prove to be notable but only about half of those in oil on an equivalent basis. Opening export options and improved well results should help push up gas production at a faster pace than oil over the long term.

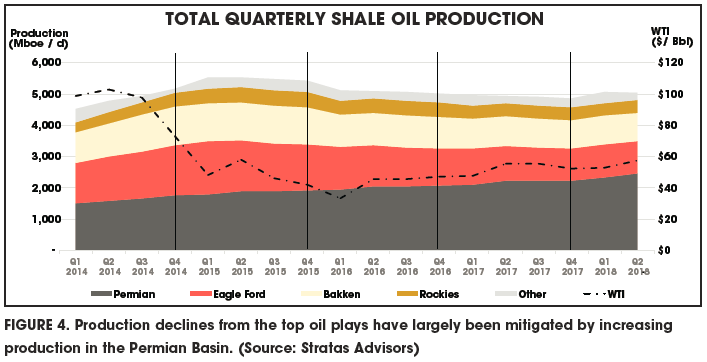

The Permian Basin continues to be the largest source of tight oil throughout the U.S., with production nearing 2 MMbbl/d, up by more than 7% relative to 2015 (Figure 4). Stratas Advisors believes the Permian Basin will continue to increase production as high-grading efforts in the area have remained strong during the downturn. Operators have continuously improved overall drilling metrics, yielding larger recoveries per well. Stratas Advisors forecasts the play to increase another 8% in 2017, posting an average rate of about 2.1 MMboe/d. The Bakken has decreased production by about 15% in 2016 to more than 1 MMbbl/d.

The younger SCOOP/STACK region has propelled itself into one of the top regions of the U.S. Operators have focused within the SCOOP for the past several years and have recently begun shifting north into the STACK. In 2016 the SCOOP/STACK is estimated to produce at a rate of more than 430 Mboe/d, which given its relative size and the new interest yields an impressive 80% increase over the 2015 average. However, the area was not immune to the oil price declines, and Stratas Advisors expects production in 2017 will be about 2% lower. The region has not yet entered into full-scale development, and the majority of production is derived from a small number of operators. Assuming WTI increases over the next several years, Stratas Advisors believes the SCOOP/ STACK region could mimic the production increases that have been experienced in the Permian Basin. The SCOOP/ STACK might not yield the same volume; however, the basin does provide multiple stacked pay zones allowing further delineation to occur, which should support what would still be an impressive and wider asset base.

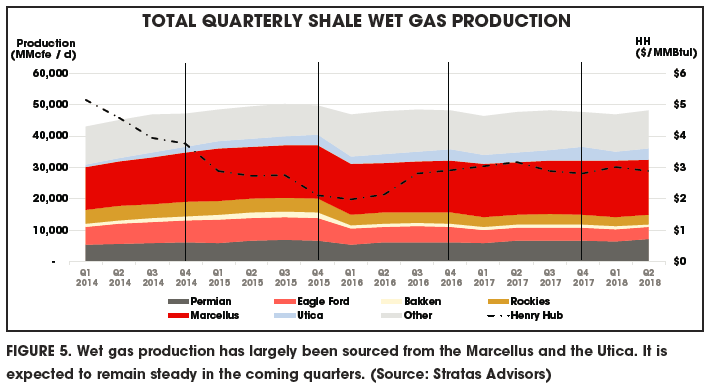

The Marcellus and the Utica have continuously produced the largest amount of natural gas since the inception of drilling in the Appalachian Basin (Figure 5). The Marcellus did marginally slow down over the past several quarters as operators were forced to reallocate resources to their best performing assets around the county. In 2015 operators in the Marcellus posted production increases of under 13%, averaging 436 MMcm/d (15.4 Bcf/d). In 2016 production in the Marcellus is expected to still post an increase, but the rate of growth has slowed considerably to only about 5% over 2015, ending the year with an overall average of 458.7 MMcm/d (16.2 Bcf/d). Production in the Utica, however, almost doubled in 2015 relative to 2014. This smaller area has received a great deal of attention, and operators continue to allocate precious capital to the region.

In a trend similar to the Marcellus, production is expected to show increases in 2016 at a lower but still impressive rate of growth. Stratas Advisors expects the Utica to post production growth this year of more than 30% to 84.9 MMcm/d (3 Bcf/d).

Recommended Reading

Trump Axes Chevron's Venezuela Oil License, Citing Lack of Electoral Reforms

2025-02-26 - U.S. President Donald Trump on Feb. 26 said he was reversing a license given to Chevron to operate in Venezuela.

Exxon CEO Darren Woods: Hydrogen Incentives ‘Critical’ for Now

2025-02-03 - Exxon Mobil CEO Darren Woods said the end goal for energy policy should be a system in which no fuel source remains dependent on government subsidies.

CEO: TotalEnergies to Expand US LNG Investment Over Next Decade

2025-02-06 - TotalEnergies' investments could include expansion projects at its Cameron LNG and Rio Grande LNG facilities on the Gulf of Mexico, CEO Patrick Pouyanne said.

Exclusive: Sheffield Says FTC Could Rescind His, John Hess’ Bans

2025-03-11 - Former Pioneer Natural Resources CEO Scott Sheffield told Hart Energy that his ban by the Federal Trade Commission from serving on Exxon Mobil’s board "was pretty much illegal. It's a baseless and illegal order that was done.”

Conoco, TotalEnergies CEOs Talk Methane Regs, Permian Vs. Senegal

2025-03-11 - ConocoPhillips CEO Ryan Lance and TotalEnergies’ Patrick Pouyanné briefly delved into a Permian Basin versus Senegal debate at CERAWeek by S&P Global.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.