A version of this story appears in the November issue of Oil and Gas Investor magazine.

A revolution is building in the overpressured dry gas portion of the Eagle Ford Shale in South Texas.

As one of the top oil-producing basins in the U.S., it’s easy to understand the ongoing chatter about the Eagle Ford Shale. But there’s hardly any mention of its gas fairway. Some chalk it up to natural gas’ bad reputation, while others believe the region is simply being overlooked.

And yet, despite being overshadowed by the oil window, dry gas producers in the southern Eagle Ford are reporting economics that are competitive not only with other gas plays, but oil plays as well. This is being driven by its strategic location, premium pricing, low operating costs and implementation of new technology, according to a number of gas-focused operators at Hart Energy’s recent DUG Eagle Ford conference in San Antonio in September.

“There’s always been industry knowledge of the Eagle Ford gas window as containing a lot of hydrocarbons ready to produce,” Michael J. Wieland, president and CEO of Laredo Energy VI LP, told attendees at the conference.

Wieland was joined by William E. Deupree, founding partner, president and CEO of Escondido Resources II LLC, John Thaeler, president and CEO of Vitruvian Exploration LLC, and Gleeson Van Riet, CFO and executive vice president of SilverBow Resources Inc.

Wieland noted, however, that the industry has come full circle since Petrohawk Energy Corp.’s discovery of the Eagle Ford Shale in La Salle County, Texas, in 2008.”

Escondido’s Deupree, based in Houston, said his company was in the dry gas portion of the Eagle Ford even before its discovery. When Deupree formed Escondido II in 2007, with funding from Mountain Capital Partners, the company’s original targets were the Escondido and Olmos formations. Escondido later expanded its acreage to include the Eagle Ford following the company’s participation with Petrohawk on a number of Eagle Ford wells that Deupree said revealed its potential.

“In the early time frame—in 2008 to 2012, when gas was $4 and $5—it was a very economic play,” he said, adding, “and now it’s a very economic play again because technology has caught up.”

The story of the rise and fall of Eagle Ford gas begins, Wieland said, with the crash of gas prices after its discovery and then the industry’s transition from the Eagle Ford and the Haynesville to the Marcellus. In recent years, though, enhanced completion techniques have spurred renewed activity in the Haynesville, which in turn have led the industry back to Eagle Ford gas, he said.

Location, location, location

“If you’re going to produce gas in the United States, this is where you want to be,” said SilverBow’s Van Riet. “And why is that? The old real estate mantra is location, location, location. We are next to all the main growth drivers in gas demand—petrochemical complex, LNG exports, Mexico. We’ve got it all there.”

Wieland and Deupree echoed this point, noting the premium natural gas prices their companies are seeing compared to the Houston Ship Channel and Henry Hub benchmarks.

“Our realized prices are about 105% of Nymex right now; so we’re really in a great place for getting our gas to market,” Deupree said. According to Wieland, Laredo’s gas is also selling at a premium to Nymex, largely due to the company’s relative position to Mexican export pipelines, where, he said, “A lot of gas is leaving the country.

“Over 3.5 [billion cubic feet] a day is going to Mexico, which is what’s really leading to the strong basis in our area,” he said.

Wieland also said the location of Laredo’s position as the southernmost producing Eagle Ford asset gives the company the advantage of having the “first Eagle Ford molecule to Mexico” available via the Nueva Era pipeline system, which began commercial service this past summer.

Vitruvian’s Thaeler also said that the developing infrastructure and markets for natural gas are appealing draws for Eagle Ford gas exploration, noting three LNG export facilities planned or under construction on the Texas coast—Freeport LNG, Cheniere LNG and Rio Grande LNG—and expanding pipeline takeaway capacity with ample market outlets.

“I’m always asked, ‘Is gas good?’ In my mind, gas is really good if you can get it to market and sell it at a good price.”

Exit strategies

In addition to the premium pricing, Eagle Ford gas producers said operating costs are low on their acreage positions thanks in part to low water yields and no need to process the gas.

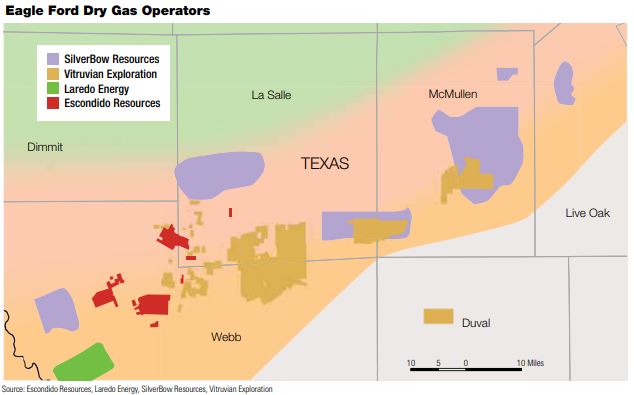

In South Texas, Laredo operates roughly 72,000 gross acres of contiguous leasehold in Webb County near the U.S.-Mexico border. The company, located in Houston and backed by Avista Capital Partners, holds about 70% working interest with gross production in August of 100 million cubic feet per day (MMcf/d) of gas.

“The acreage position is set up wonderfully for development in terms of long lateral development … economies of scale and efficient operations,” Wieland said.

Laredo has identified more than 300 potential drilling locations in the lower Eagle Ford on 1,000-foot spacing with average laterals of more than 9,300 feet. Wieland said Laredo is already seeing promising results from the three wells it brought online beginning in late 2017. Needmore 22H on a 7,277-foot lateral reached a peak 180-day cumulative rate of 1.5 Bcfe; Ellen C-12H on a 6,696-foot lateral peaked at 1.8 Bcfe; and the BFM B-1H achieved 2 Bcfe cumulative rate on a 6,291-foot lateral.

So far this year, Escondido has drilled 12 wells and completed 10 on its 81,000 net-effective-acre position in “the heart of the dry gas trend” in the Eagle Ford in Webb and La Salle counties, Deupree said.

The company has current net production of 100 MMcfe/d, of which 85% is producing from the Eagle Ford with the remaining 15% from the Escondido and Olmos formations. Deupree said Escondido is targeting multibench development of the lower Eagle Ford and upper Eagle Ford with a single-rig program.

“We went to a multibench approach mainly because we didn’t want to run the risk of parent-child relationship from top to bottom as well as side to side in the future,” he said.

According to Deupree, Escondido has a substantial undeveloped inventory of about 300 proven locations with a well-defined plan to develop its position. The company expects to grow net production to about 200 MMcfe/d by year-end 2020 while still running a single-rig program.

Deupree said the strategy for Escondido is to “just execute.”

As a result, the company will convert its proved undeveloped reserves (PUDs) to proved developed producing, probables to PUDs, and bring in another layer of possibles into the mix, which he said will ultimately lead to “a successful exit when the market is ready for us.”

Escondido’s neighbor, Laredo, might already be looking for the door, according to a report by Bloomberg on Oct. 2. Bloomberg reported that unnamed sources said Laredo is working with an adviser on an auction process and in recent weeks has opened a data room for a sale that could value the company at as much as $300 million. Though Wieland didn’t mention Laredo’s exit strategy during DUG Eagle Ford, he told attendees that the company has an asset it can grow “in a sustainable way for a decade and beyond.”

In the lower Eagle Ford, Laredo currently has three uncompleted wells, which it plans to bring online by year-end 2018. For 2019, the company will target a 12- to 15-well drilling program, Wieland said.

“We’ve got a lot to deal with in the lower Eagle Ford right now, and we’re going to stick there and continue to delineate and make the upper Eagle Ford co-development more of a 2019 question,” he said.

Laredo’s estimated net resource potential from the lower Eagle Ford is about 3 Tcfe. However, when the company adds in the upper Eagle Ford, Austin Chalk and shallow horizons, the total net resource potential for Laredo’s position grows to more than 10 Tcfe.

“We’re excited about the future, and I think we’ve only scratched the surface in terms of what the potential is in this asset in this area,” he said.

Still exploratory

“People always wonder why we are here,” said Thaeler. His response? “This is great rock.”

In fact, Thaeler said the rock quality in the Eagle Ford dry gas window is one of the leading factors that encouraged Vitruvian to explore for gas in the play. The area is highly overpressured with about 0.75 psi/foot to 0.99 psi/foot, and has organic rich mudstone and low clay content.

In March 2017, private-equity funder Quantum Energy Partners backed Vitruvian IV with a $450-million equity commitment, and The Woodlands, Texas-based E&P quickly entered the South Texas Eagle Ford trend. The three prior iterations of Vitruvian successfully exited positions in the Mississippi Lime and the Scoop and Stack plays.

As Vitruvian II and III were winding down, Thaeler said the team looked across the U.S. to identify the next opportunity based on three criteria: a greenfield region that offers contiguous leasehold; the ability to prove the resource; and a proven hydrocarbon system.

“Fortunately, the Eagle Ford was available,” he said. “Having worked previously in the Woodford Shale and the Anadarko Basin, we were favorably impressed with the rock qualities of the dry gas Eagle Ford.” And as far as scale is concerned? “It’s a very large area we’re saying grace over.”

Vitruvian IV now has more than 130,000 net acres in the Eagle Ford Shale dry gas window in Webb, La Salle and McMullen counties, with gross production of roughly 33 MMcf/d from four flowing wells to date. Prior to acquisition, no horizontal wells had been drilled on its acreage. Vitruvian currently has one rig running, delineating its vast acreage with two-well pads.

Its first four wells within its Althea Project straddling the La Salle and Webb county line were spaced at 880 feet and featured slickwater completions with 1,500 pounds of sand and 40 barrels of water per foot. The Ocho MDL A 1H and 2H flowed 9.1 and 8.3 MMcf/d on 24-hour IP, respectively, and its Nueces A 1H & 2H flowed 10.7 and 10 MMcf/d, respectively. All IPs are flowed back conservatively, he said.

“This is really an exploratory type play,” he said, with about 300 wells drilled to date. Vitruvian is at the very early stages of “a steep learning curve,” he said, in which he promised to “tear apart the resource and characterize the heck out of the reservoir.”

Technology catch-up

SilverBow is another operator that has pinned Eagle Ford gas as an overlooked opportunity. The company has about 100,000 acres mostly in the dry-wet gas window with acreage blocks stretching from Live Oak County and downtrend into Webb County. It expects to exit 2018 with roughly 230 MMcfe/d of production.

SilverBow is the reincarnation of the former Swift Energy following restructuring. Upon its emergence from bankruptcy, the company, based in Houston, reduced its portfolio and became an Eagle Ford gas pure play. The company has decreased its drilling cost per well by 58%, from $4,560 in 2013 to $1,933 in 2017. It has also decreased its completion well cost by 40%, from $4,533 in 2014 to $2,630 in 2017.

In addition, SilverBow increased its well count in the Eagle Ford dry gas window from 55 in 2016 to 72 in 2017. The company has increased its daily production from 154 MMcfe/d in first-quarter 2018 to 160 MMcfe/d in second-quarter 2018 and estimates a 40% growth in fourth-quarter 2018. The company has 335 producing wells in the area and plans further development.

Other operators have been drawn into the fairway within the last two years, including private-equity-backed Teal Natural Resources, Sierra Resources, Pursuit Oil & Gas and Verdun Oil Co. So why aren’t other operators talking about Eagle Ford gas? According to Van Riet, it’s because SilverBow is the only public pure play while the other operators focused on Eagle Ford gas are either private companies or are multibasin operators that haven’t published much information about their results in the region.

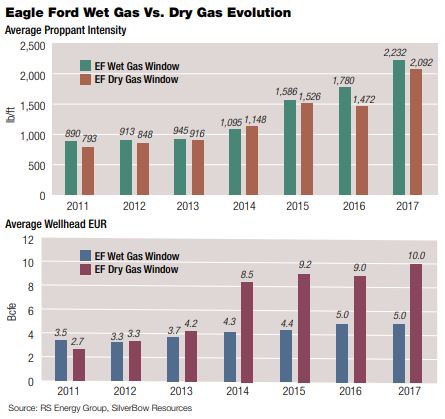

Today’s results are not yesterday’s dry gas Eagle Ford. The company is successfully applying Generation 5 technologies and utilizing modernized strategies.

“The big difference is well lateral lengths have gone up about 40%. Proppant intensity has gone up about 150%. EURs in the gas windows have gone up three times,” Van Riet said. “The difference is, there haven’t been as many wells drilled in the dry gas window.”

SilverBow’s strategy remains longer laterals and more proppant to equal higher EURs. “It’s worked in every basin in the U.S.; it works here in the gas window,” he said.

In its Fasken area close to the Mexico border, Van Riet said, returns compete with any gas play in the U.S.—124% IRR (based on $3 gas and $50 oil) and 14 Bcfe EUR. These wells, drilled on six-well pads for less than its $5 million AFE, pay out in less than a year.

“Of the top 50 wells in the dry gas window, defined as 12-month cumm’ed production, we’ve drilled 20 of those top 50. Our task is to extend that north and east of that position with Gen 5 completions that haven’t seen much [technology uplift] in the last five or six years.”

He added that the basin changes quite a bit not only in depth and pressure moving northeastward, but also in rock type.

“We are finding that different areas require different casing programs. They require different efforts to drill the curve, different types of drilling in the landing, drilling the horizontal,” he said. In its Oro Grande position in La Salle and McMullen counties, with well costs near $8 million, returns clock out at 60%.

SilverBow added a second rig to its program in March and hit 200 MMcf/d of production in August. It has another 700 gross undrilled locations remaining.

Economic disparity

In response to critics that report the region needs $4 gas to break even, Thaeler strikes back. “Do you think [we] would be in this area if $4 was the breakeven point for their gas?

Before entering the play, he said, his team stress tested results at $2.25/Mcf, “and we are happy to continue operations under $2.25. These are economic wells at today’s gas prices. If I had my pick of anywhere in the U.S. to be with natural gas, it would be in South Texas.”

Bottom line, he said, “we expect high returns on our capital during this development phase, or we wouldn’t be doing it. There is plenty of value in dry gas Eagle Ford.”

Thaeler suggests naysayers are confusing the economics by equating costs and completions in the oil window with those in the dry gas window. “These are different beasts,” he said. “And what you need in a really tight oil formation and how you fracture and stimulate that rock is different than what you need in gas.”

Both Vitruvian and SilverBow said they are in the beginning “innings” of their operations in the Eagle Ford gas fairway and are still learning from their own data and shared information from competitors.

The results of later innings may decide the debate over whether Eagle Ford gas is an overlooked opportunity.

“It has been neglected and forgotten about for a while,” Van Riet noted, “so it’s just now seeing the increased lateral lengths and proppant intensity you see elsewhere. And we’re getting a very high rate of change.”

Thaeler confirmed the shale’s potential: “I think there is enough data out there that clearly show these are economic wells at today’s gas prices. I’m confident that gas in South Texas is the right place to be.”

Recommended Reading

EIA Reports Smaller than Expected NatGas Withdrawal-Analysts

2025-03-06 - A mild end to February shows a surprising demand decrease for natural gas, according to analysts citing U.S. Energy Information Administration data.

Enbridge Plans $2B Upgrade for Mainline Crude Pipeline Network

2025-03-05 - New tariffs imposed by President Trump are unlikely to affect Enbridge’s Canadian and U.S. operations, CEO says.

Gas-Fired Power Plants Create More Demand for Haynesville Shale

2025-03-04 - Expansions and conversions of Gulf Coast power plants are taking advantage of the plentiful Haynesville Shale gas.

Reset Energy to Build a Nitrogen Rejection Unit for Permian Residue Gas

2025-03-04 - Reset Energy will install a nitrogen rejection unit at a large-scale facility in the Permian Basin to deliver a residue gas product for a midstream operator.

EIA Reports NatGas Rig Count Fall-Off in ’23, ’24

2025-03-04 - The U.S. Energy Information Administration’s report of a falling natural gas rig count backs up statements from producers in the Appalachian and Haynesville basins.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.