Associated gas will drive North American gas production in the near term, positioning it to serve as a bridge fuel through the energy transition.

However, associated gas can be a mixed blessing, prompting operators to wrestle with choices on what to do about the additional production. Each choice has its pros and cons, and geopolitical uncertainty underlies major long-term investments that operators consider.

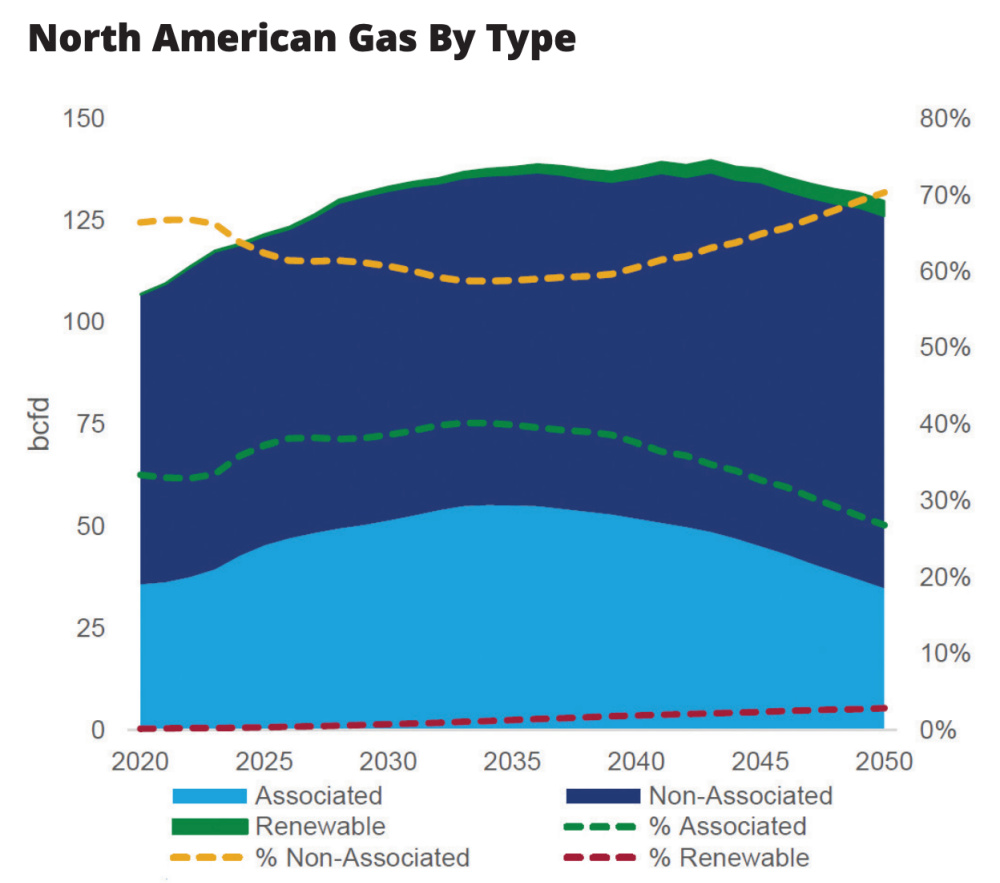

Wood Mackenzie defines gas production driven by oil economics to be associated gas and gas production driven by gas economics to be dry gas.

According to WoodMac, associated gas production in the Lower 48 is climbing, primarily due to increased gas production from the Permian Basin. Eugene Kim, research director for WoodMac’s North America gas team, said the “tremendous growth” in production of associated gas from the Permian dwarfs associated gas output from all the other basins.

“Associated gas runs off of the oil economy. It’s not totally free, but it’s the lowest cost option.”—Eugene Kim, Wood Mackenzie

While associated gas output in the Permian was hitting about 4 Bcf/d in 2015, the basin currently produces over 15 Bcf/d of associated gas and is expected to produce more than 19 Bcf/d by the end of 2024, Kim said. In fact, he expects Permian associated gas production to continue growing into the 2040s, while other Lower 48 areas will start to plateau or decline by 2030 or 2035.

Alaska, Kim said, is producing less than 1 Bcf/d of associated gas, with the majority of that coming from Prudhoe Bay.

In the Gulf of Mexico, associated gas is down to about 2 Bcf/d from its heyday with output of more than 14 Bcf/d of gas, he said. Some of it was dry gas, while some was associated gas.

Earlier this year, the Bureau of Offshore Energy Management released its 2022 to 2031 U.S. Outer Continental Shelf Gulf of Mexico region oil and gas production forecast, which predicts associated gas production in the Gulf of Mexico will remain fairly steady during the next decade.

Most of the associated gas in the Gulf of Mexico is from deepwater fields, where dry gas wells are generally uneconomic to develop.

North American gas market

Carol Johnston, vice president of energy, utilities and resources at IFS, said demand for natural gas is increasing because of its role as a backup energy source on the path of the energy transition.

“That is creating more demand and market opportunity” but also causing prices to fluctuate, she said.

The overall North American gas market is set to expand quite a bit, including through export growth, and that associated gas is needed to support that, according to Kim.

“Look at how much new gas is required every year to come to the market … to make up for existing production declines and market expansion,” he said.

He projects needing 17 Bcf/d of new gas production on average during 2023 to 2025 to meet decline and expansion.

“That’s a tremendous amount of gas considering we’re now at 97 Bcf/d” of total gas output from the U.S., he said. “Every year, we need to drill enough to produce that 17 Bcf/d that the market will require.”

And of course, the mix of dry and associated gas that is added will affect the price of Henry Hub.

“Associated gas runs off of the oil economy. It’s not totally free, but it’s the lowest cost option,” Kim said. “The larger the amount of associated gas produced, the lower the price of Henry Hub will be.”

Johnston said two main factors constrain associated gas production. If the price is not high enough, companies may throttle back production. On the other hand, it can be an infrastructure issue, she said.

Further, she said some operators are reluctant to enter large multiyear projects due to geopolitical uncertainty or regulatory or permitting hurdles.

The Biden administration is pursuing renewable energy sources and moving away from fossil fuels.

The last offshore oil and gas lease sale was in November 2021, which a court vacated in January 2021 and then Congress most recently reinstated. No offshore oil and gas lease sales are being held in 2022, and there is the potential that only one offshore lease oil and gas sale will occur in 2023.

Offshore wind lease sales are happening, however, with sales in New York Bight and Carolina Long Bay earlier this year and plans for lease auctions in the Gulf of Mexico and offshore California.

Working around flaring reductions

In 2016, the U.S. endorsed the World Bank’s Zero Routine Flaring by 2030 initiative, and in 2020, U.S. regulators made it more difficult for operators to routinely flare associated gas production.

Historically, operators routinely flared associated gas as a safe method of disposal; however, flaring is determined to be wasteful and emits greenhouse gases.

“There is still sizable flaring going on in the U.S.,” Kim said.

Efforts to reduce flaring are helping, however.

According to the World Bank, in 2021, the top 10 flaring countries on an absolute volume basis accounted for 75% of all gas flaring and 50% of global oil production.

“The role of natural gas as a backup energy source ‘is creating more demand and market opportunity.’”—Carol Johnston, IFS

At No. 4 in terms of absolute volume flared, the U.S. has been in the top 10 list for the past decade. But it has a distinction from other long-term members of this list, such as Russia, Iraq, Iran, Venezuela, Algeria and Nigeria, in that it is the only country to have successfully reduced absolute flare volumes while increasing production over the past decade. The U.S. decreased its flaring intensity by 46% and achieved an 8% reduction in terms of absolute volume over the decade, according to the World Bank.

Although flaring is off the table as the primary means of associated gas disposal, operators do have other options.

Associated gas can be gathered, processed and delivered down the supply chain, or stored, Kim said, but these options require infrastructure. It can also be reinjected in the reservoir to maintain pressure, such as in some Alaskan fields, although this also requires infrastructure.

“That whole process takes money to do. You need appropriate production systems to recycle and reinject it into the reservoir, which is an added cost to the producer,” Kim said. “For a lot of new wells, we’re not seeing as much effort to recycle that gas.”

Associated gas can be used in the field for fuel purposes, he said, such as running compressors using associated gas instead of diesel or carrying out small-scale LNG liquefaction. And some producers are even talking about using excess gas to power gas turbines for bitcoin mining.

“There are some novel uses of excess gas production,” Kim said.

Recommended Reading

CEO: TotalEnergies to Expand US LNG Investment Over Next Decade

2025-02-06 - TotalEnergies' investments could include expansion projects at its Cameron LNG and Rio Grande LNG facilities on the Gulf of Mexico, CEO Patrick Pouyanne said.

Trump Axes Chevron's Venezuela Oil License, Citing Lack of Electoral Reforms

2025-02-26 - U.S. President Donald Trump on Feb. 26 said he was reversing a license given to Chevron to operate in Venezuela.

Paisie: Impact of Tariffs, Sanctions and ‘Drill, Baby, Drill’

2025-03-07 - The U.S. has the advantage with tariffs on Canada, but sanctions and pleas for increased oil supply are unlikely to be effective.

Congress Kills Biden Era Methane Fee on Oil, Gas Producers

2025-02-28 - The methane fee was mandated by the 2022 Inflation Reduction Act, which directed the EPA to set a charge on methane emissions for facilities that emit more than 25,000 tons per year of CO2e.

E&P Execs Level Scathing Criticism at Trump's Drill Baby Drill 'Myth'

2025-03-26 - E&P executives pushed back at the Trump administration’s “drill, baby, drill” mantra in a new Dallas Fed survey: “’Drill, baby, drill,’ does not work with [$50/bbl] oil,” one executive said.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.