An OPEC ‘shock and awe’ campaign of production cuts could also jar the market back into balance, analysts say. (Source: Hart Energy)

It may be time for OPEC and U.S. shale producers to pump the brakes.

Despite a large weekly drop in crude inventories, banks continue to mark down oil prices. Barring a sharp cut by OPEC or a visible slowdown of U.S. shale activity, oil prices are likely to continue to fall.

Goldman Sachs analysts said in a July 10 report that oil prices could dip below $40 per barrel (bbl) as the “market tests OPEC’s and shale’s reaction.”

Prices aren’t expected to be driven by storage concerns but “the ongoing search for a new equilibrium,” the report by Goldman’s Damien Courvalin said.

U.S. commercial crude oil inventories decreased by 6.3 million barrels (MMbbl) the previous week, the Energy Information Administration reported July 6. At 502.9MMbbl, U.S. crude oil inventories are in the upper half of the average range for this time of year.

“We believe that sustained trends in inventory draws and U.S. rig count declines or evidence of further OPEC actions will be required for prices to rally,” Goldman Sachs said in the report.

Andrew Fletcher, senior vice president of commodity derivatives at KeyBank National Association, said Goldman’s report was unfortunately timed as Saudi Arabia announced its production for June was higher than the 9.88 MMbbl/d allowed for under OPEC’s agreement.

“This from the country who has said it will do what it takes to support the price,” Fletcher said in a July 11 commentary. “It is also fair to assume it will be much more difficult for the market to rally much beyond the mid $50s since the level from which we have to rally is much lower than a couple of months ago.”

Earnings season for U.S. E&Ps may be a bellwether for the markets to assess shale operators’ response to lower prices and the magnitude of ongoing efficiency gains, Goldman said.

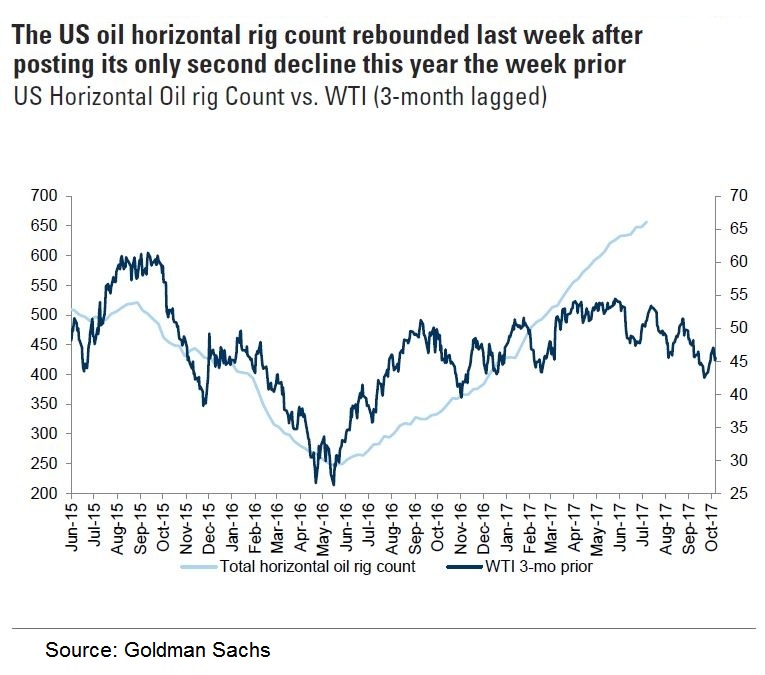

The U.S. oil horizontal rig count rebounded last week after posting only the second decline of the year, potentially due to end-of-quarter deferrals, Goldman said.

“The guts of the rig data show an only gradual deceleration in [hydraulic] producer rig count, with private producers rig count rebounding and [gas] producers continuing to ramp up strongly,” Goldman’s report said. “The coming month will be key to testing whether producers are responding to the signal of $45/bbl WTI prices.”

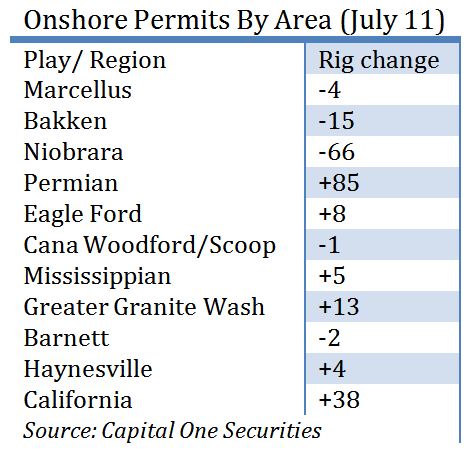

On July 11, Capital One Securities noted that U.S. land permits rose 218 week over week to 1,215 with the lion’s share of gains in the Permian, followed by California.

The global supply picture has been further muddied by sustained production from Libya and Nigeria, though both countries have been invited to participate in OPEC’s compliance committee meeting on July 24.

The global supply picture has been further muddied by sustained production from Libya and Nigeria, though both countries have been invited to participate in OPEC’s compliance committee meeting on July 24.

“We continue to believe that there is another opportunity for OPEC to increase the cuts, but that this should be done in a ‘shock and awe’ manner, with little public announcement. This requires further patience in assessing the group’s response to higher aggregate production and lower prices,” Goldman’s report said.

For now, the market appears to be out of patience for a large draw on oil inventories and is “increasingly concerned about next year’s balances,” Goldman’s report said.

“We believe that price upside will need to be front-end driven, coming from observable near-term physical tightness and signs of a U.S. shale activity slowdown on a sustained basis in coming weeks,” the report said.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Scout Taps Trades, Farm-Outs, M&A for Uinta Basin Growth

2024-11-27 - With M&A activity all around its Utah asset, private producer Scout Energy Partners aims to grow larger in the emerging Uinta horizontal play.

E&P Consolidation Ripples Through Energy Finance Providers

2024-11-27 - Panel: The pool of financial companies catering to oil and gas companies has shrunk along with the number of E&Ps.

Utica Oil E&P Infinity Natural Resources’ IPO Gains 7 More Bankers

2024-11-27 - Infinity Natural Resources’ IPO is expected to provide a first-look at the public market’s valuation of the Utica oil play.

Exclusive: Trump Poised to Scrap Most Biden Climate Policies

2024-11-27 - From methane regulations and the LNG pause to scuttling environmental justice considerations, President-elect Donald Trump is likely to roll back Biden era energy policies, said Stephanie Noble, partner at Vinson & Elkins.

FERC Gives KMI Approval on $72MM Gulf Coast Expansion Project

2024-11-27 - Kinder Morgan’s Texas-Louisiana upgrade will add 467 MMcf/d in natural gas capacity.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.