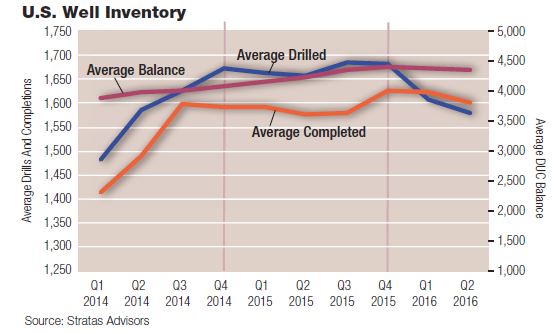

The North American shale landscape has transformed over the past several years as the industry has ridden the waves of price volatility, hitting its first major downcycle. The number of wells drilled dropped dramatically after the price of oil fell in late 2014, and although activity seemed poised to pick up in mid- 2015, instead it slid considerably further. Completions, on the other hand, didn’t really rally until late 2015, when producers began building a relatively healthy balance of drilled but uncompleted (DUC) wells.

Given the drop in commodity prices, production has declined from the historic gains U.S. producers posted during the “shale gale.” While natural gas basins have not declined as significantly, several oil and liquids-rich areas have taken big hits, with reports of production declining by more than 80% in a few of the smaller plays. This has been coupled with operators declaring bankruptcy or selling out of their producing assets altogether, as seen in the Panhandle and other regions of North Texas and Oklahoma.

The average balance of DUCs per quarter for the U.S. industry has held relatively steady this year, while the average number of completions and wells drilled has declined.

Notwithstanding the drop in production, “shale resiliency” is often referenced when considering global oil and gas markets post-price collapse. While reported figures have shown a clear turn for the worse, especially in certain plays, the consolidated impact is markedly less catastrophic than the dire predictions for which many in the industry had been bracing. Total production in 2016 is expected to close out approximately 5% lower than 2015 levels. Compared to the massive increases to which the world had grown accustomed, this drop is indeed material.

In recent quarters, the industry has focused on completions: how operators are completing wells, and how changing strategies have translated into improved recovery rates.

Over the past couple of years, the majority of capital investment has gravitated toward liquids-rich basins because of low natural gas prices. The Appalachian Basin remains competitive, despite infrastructure constraints, but operators have increasingly turned their attention to high-grading the more oily plays.

Within these oily sub-basins, Texas basins and Oklahoma’s Scoop/Stack region have generated some of the highest IP rates and EURs, based on posted well results. The Midland and Delaware basins have generated EURs above 300,000 barrels of oil equivalent (Mboe), followed closely by the Eagle Ford and Bakken. The Scoop/Stack region’s EURs are similar to those of the Eagle Ford, and its IP rates top 700 boe/d.

Valuing these results requires taking into consideration the amount of capital required to drill. One method is to normalize results to lateral lengths. Using the normalized figures, the Delaware and the Eagle Ford provide some of the largest recoveries per 1,000 feet of lateral.

The Stack shows the largest year-overyear increase in overall lateral length, but this accomplishment has not yet translated into higher recovery per foot when compared to the older and more established sub-basins like the Delaware and Eagle Ford. This year a number of operators announced plans to continue increasing lateral lengths within the Permian and Scoop/Stack areas.

With respect to oil plays, it’s not surprising that the best economic results show up in the Permian, Eagle Ford and Bakken. The Delaware, Eagle Ford and Bakken all require less than $40 per barrel to break even; the Midland Basin and portions of the Rockies fare well below $50.

For primarily gas plays, weighted average results support current drilling activity in the Appalachian Basin, but until gas prices increase, operators will continue to seek better risk-adjusted returns in the oily plays. The Scoop/ Stack is listed as a gas play, but it boasts a meaningful amount of liquids, and its stacked structure helps to offset risks around well results.

Recommended Reading

International Battery Metals CEO Talks Direct Lithium Extraction

2025-03-18 - IBAT CEO Iris Jancik, who stepped into the role in August, shared her insight on market conditions, lessons learned and China.

E&Ps’ Subsurface Wizardry Transforming Geothermal, Lithium, Hydrogen

2025-02-12 - Exploration, drilling and other synergies have brought together the worlds of subsurface oil drilling and renewable energies.

Standard Lithium, Equinor Win $225MM DOE Grant for Lithium Project

2025-01-16 - Equinor and Standard Lithium aim to reach a final investment decision on its South West Arkansas lithium project in the Smackover Formation by year-end 2025.

Energy Transition in Motion (Week of March 14, 2025)

2025-03-14 - Here is a look at some of this week’s renewable energy news, including a record-breaking year for solar capacity additions.

Smackover Lithium Derisks Direct Lithium Extraction Technology

2025-03-11 - With the completion of a final field test, the Smackover Lithium joint venture's direct lithium extraction technology moves toward commercialization, Standard Lithium says.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.