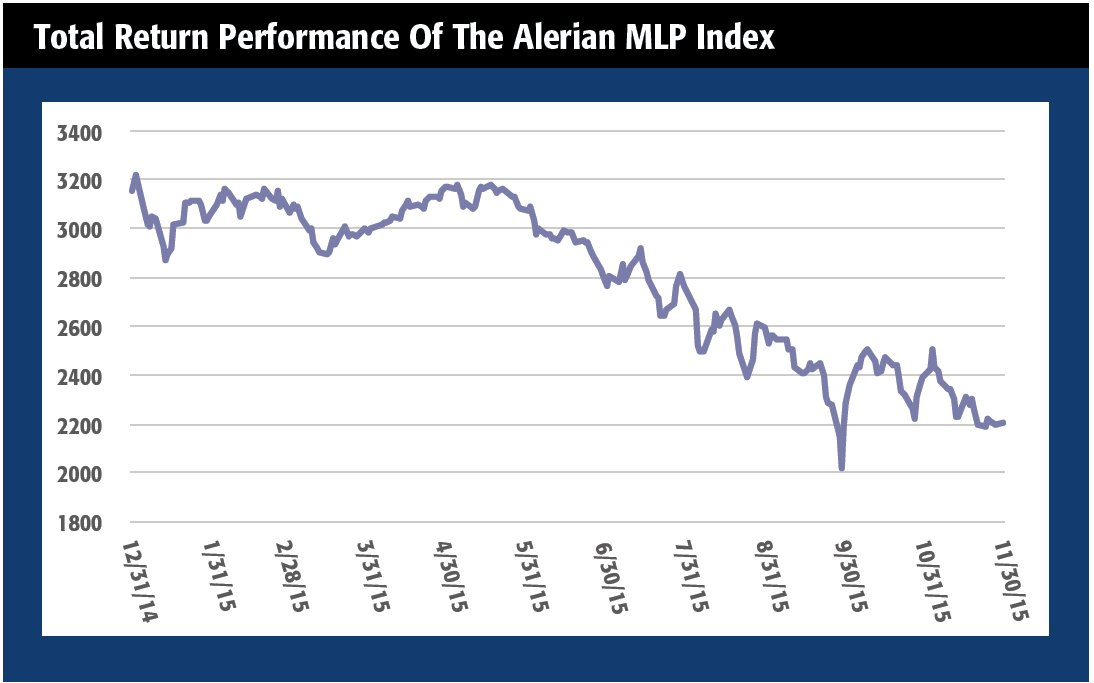

While this column went to print before the first of the year, I somehow doubt that MLPs have recovered their 30.2% year-to-date loss, as measured on a total return basis by the Alerian MLP Infrastructure Index (AMZI) as of the end of November. Here are three things that could extend the volatility in 2016:

1. A bellwether MLP cuts its distribution

It is highly unlikely that large-cap, investment-grade MLPs with reasonable leverage and distribution coverage as well as years of sequential quarterly distribution growth under their belts—Enterprise Products Partners and Magellan Midstream Partners, for example—would suddenly switch gears and cut their distributions. But there are others for which the possibility is less remote, especially in an environment where distribution growth, at least as the expense of higher leverage and lower distribution coverage, is not rewarded. Given the high percentage of retail ownership of MLPs, midstream distribution cuts would likely send some retail investors (the ones that are left, anyway) fleeing for the exits and prolong the choppy trading of 2015.

A distribution cut could be implemented not (necessarily) because current cash flows aren’t sufficient to support the distribution, but also because MLPs may need to fund projects with retained cash flow when the capital markets door is shut for many names. Traditionally, MLPs fund projects with 50:50 debt and equity, but management teams are reluctant to issue equity, privately or publicly, at prices this low. Also, with higher lever-age ratios, debt financing may be just as difficult or expensive.

2. Global demand destruction

Low commodity prices typically spur manufacturing and transportation, but should an event occur, like a recession in China or even a meaningful reduction in China’s growth rate, the demand free-fall would leave producers with very few outlets, as the market is already awash in supply.

3. Ceiling-less oil production

OPEC no longer has production targets, so market forces alone will determine the global supply. If Iran, previously under sanctions, has the relevant and up-to-date infrastructure to increase production to promised levels in the near term, the excess supply would lead to continued pricing uncertainty. Likewise, ongoing technological drilling breakthroughs and high-grading of wells contributes to incremental supply.

And it’s worth noting that while fundamentals are an important consideration, 2015 saw MLPs trade heavily on market perception as well. MLP recovery will be dependent not only on a fundamental recovery in commodity prices, but also the belief that the MLP financing model remains intact for the vast majority of names.

With no obvious near-term catalyst, those investors who are adding to positions today are able to stomach expected volatility and retesting of lows. They are also being paid rather handsomely to wait.

Recommended Reading

E&P Highlights: Feb. 10, 2025

2025-02-10 - Here’s a roundup of the latest E&P headlines, from a Beetaloo well stimulated in Australia to new oil production in China.

TGS Awarded Two More Streamer Contracts Offshore Norway

2025-02-10 - Data and intelligence TGS provider now has six contracts scheduled on the Norwegian Continental Shelf.

US Drillers Add Oil, Gas Rigs for Second Week in a Row, Baker Hughes Says

2025-02-07 - Despite this week's rig increase, Baker Hughes said the total count 6% below this time last year.

PotlatchDeltic Enters Lithium, Bromine Lease Agreement in Arkansas

2025-02-06 - PotlatchDeltic’s agreement with gives Tetra Brine Leaseco covers about 900 surface acres in Lafayette County, PotlatchDeltic says.

McDermott Completes Project Offshore East Malaysia Ahead of Schedule

2025-02-05 - McDermott International replaced a gas lift riser and installed new equipment in water depth of 1,400 m for Thailand national oil company PTTEP.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.