The price of Brent crude ended the week at $88.06 after closing the previous week at $87.39. The price of WTI ended the week at $83.68 after closing the previous week at $83.24. The price of DME Oman crude ended the week at $89.99 after closing the previous week at $88.02.

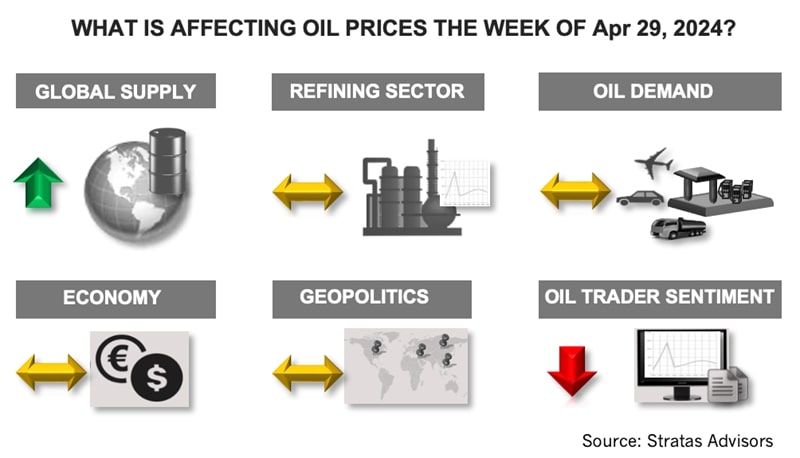

As we expected, the aftermath of the limited attack on Iran by Israel has resulted in reducing geopolitical tensions with Iran not responding with a counterattack. Also, the economic news of last week did not provide any additional support for oil prices.

- Last week, the U.S. Commerce Department released its report for U.S. GDP growth during Q1, and the report indicated that the U.S. GDP grew by only 1.6% on an annual basis for Q1, which is significantly less than during the Q4 of last year when the US economy grew at an annual rate of 3.4%. It is also the lowest quarterly growth since Q2 of 2022. The lower rate of growth during Q1 resulted from a slowdown in government spending, an increase in the trade deficit (from $918.5 billion in Q4 to $973.2 in Q1), and a drawdown in inventories. While consumer spending held up fairly well (2.5% growth in Q1 in comparison to 3.3% in Q4 2023), the positioning of consumers is weakening. According to the U.S. Bureau of Economic Analysis, the personal savings rate decreased to 3.2% in March, has been on a downward path since May 2023, and is heading to the lowest levels since 2007. In comparison during the period from 2010 through 2019, the personal savings rate averaged above 5.0%. Concurrently, credit card debt is at all-time highs and continuing to increase (by 143 billion in Q4) and consumer delinquencies are increasing. Additionally, the inflation rate is increasing again, as indicated by the personal consumption expenditure (PCE) price index (excluding food and energy), which increased by 3.7% in Q1 – well above the Federal Reserve’s targeted inflation rate of 2.0%.

- The news pertaining to China’s economy was also disappointing. Despite China reporting last week that its economy grew at 5.3% on an annual basis during Q1 and 1.6% in comparison to Q4 of 2023, there remain signs of weakness. Retail sales increased by only 4.7% from the previous year and in March by only 3.1%. China is attempting to increase consumption and recently announced a plan to provide buyers who are replacing old cars with new cars an incentive of around $1,400. Another sign of weakness is that China’s exports have been decreasing at the same time China is importing less. Furthermore, the Chinese National Bureau of Statistics reported over the weekend that the profitability of large Chinese industrial companies decreased by 3.5% in March.

Additionally, the sentiment of the oil traders became less bullish. The net long positions of WTI traders decreased last week for the second consecutive week, declining by nearly 25%. The net long position of Brent traders also decreased with traders reducing their long positions while slightly decreasing their short positions.

Consequently, even with the reported drawdown in U.S. crude inventories (decrease of 6.37 MMbbl) the price of Brent crude oil (as well as the price of WTI and DME Oman) remains below the upward channel that had been in place since January of this year. Crude inventories are lower than the level of the previous year (454 MMbbl vs. 461 MMbbl) and lower than in 2019 (454 MMbbl vs. 461 MMbbl).

The price of Brent crude, however, remains above the 200-day moving average. Additionally, crude supply is providing some support with supply in the U.S. stagnating and OPEC+ adhering to its supply cuts, which is helped by some members struggling to reach their production targets. For the upcoming week, we think that oil prices will move sideways.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paisie, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Oceaneering Acquires Global Design Innovation

2024-10-30 - Oceaneering purchased Global Design Innovation, the only provider certified by the United Kingdom Accreditation Service (UKAS) to perform remote visual inspection using point cloud data and photographic images.

ADNOC Contracts Flowserve to Supply Tech for CCS, EOR Project

2025-01-14 - Abu Dhabi National Oil Co. has contracted Flowserve Corp. for the supply of dry gas seal systems for EOR and a carbon capture project at its Habshan facility in the Middle East.

E&P Highlights: Nov. 18, 2024

2024-11-18 - Here’s a roundup of the latest E&P headlines, including new discoveries in the North Sea and governmental appointments.

ProPetro Agrees to Provide Electric Fracking Services to Permian Operator

2024-12-19 - ProPetro Holding Corp. now has four electric fleets on contract.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.