The price of Brent crude ended the week at $82.63 after closing the previous week at $85.03. The price of WTI ended the week at $80.13 after closing the previous week at $82.21. The price of DME Oman crude ended the week at $81.88 after closing the previous week at $84.65. The price of Brent crude is now threatening to fall below its 200-day moving average with the price of Brent crude declining from $87.34 on July 3.

Last week’s price movement aligned with our expectations that disappointing economic news would put downward pressure on oil prices – and the economic news is not getting any better.

- With respect to the U.S., the Conference Board’s Leading Economic Index decreased by 0.2% in June, which follows a 0.4% decrease in May – and for the first half of 2024 by 1.9% after decreasing by 2.9% in the second half of last year. The main reasons for the decreases include lower consumer expectations, the decreasing level of new orders, and increasing unemployment claims. The June data is consistent with U.S. GDP growth of only around 1.0% in Q3 on an annualized basis.

- Last week, China’s Central Committee met for four days at the third plenum, which is held every five years. The resulting communique presented long-term goals for achieving technological self-sufficiency, improving social welfare, and reforming fiscal, taxation, and financial systems. The communique, however, did not address the short-term factors that are negatively affecting China’s economy, including weak domestic demand, and the debt-ridden property sector coupled with elevated provincial and municipal debt. The lack of any short-term policy announcements is disappointing, given that China’s economic growth slowed in Q2 from 5.3% in Q1 to 4.7%, which is the weakest growth since Q3 of 2023.

- With the U.S. Federal Reserve still not making an interest rate cut (and we do not expect that any rate cut will come before the U.S. presidential election), the European Central Bank is maintaining interest rates after an initial cut in June, even as the EU economy continues to have lagging growth.

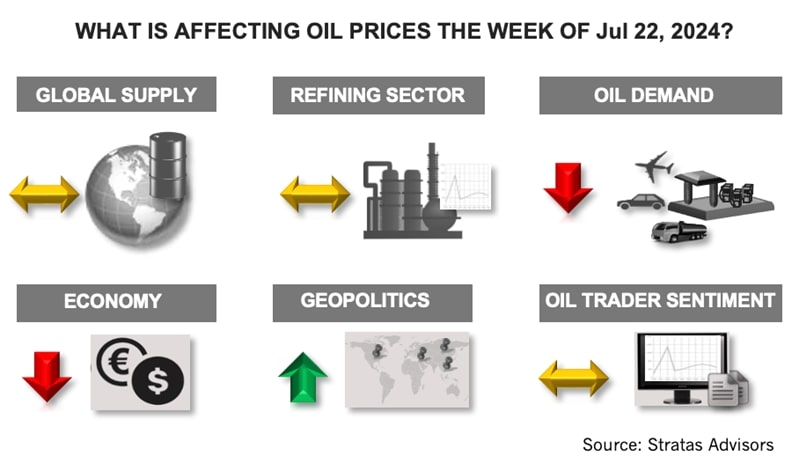

For the upcoming week, we are not expecting any developments that will change the recent price dynamics.

- We are not expecting any bullish news coming from the supply side with the market expecting that OPEC+ will maintain its current supply strategy. The same goes for the demand side, given the current performance of the major economies.

- With respect to geopolitics, the Russia-Ukraine conflict and the fighting in the Middle East is continuing – and with the U.S. now being led by a lame-duck president – the conflicts are likely to continue with the current dynamics and the associated risks. Additionally, geopolitics is being complicated by the political instability associated with many of the Western countries including the U.S. So far, however, the flow of oil is continuing, and the risk premium has remained low.

- While oil traders have been adding to their net long positions in recent weeks, the rate of increase has slowed. Last week, traders of WTI increased their net long positions by only 4.25% by increasing their long positions while decreasing their short positions, while traders of Brent crude decreased their net long positions by increasing their short positions.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Vision RNG Inks Landfill Gas Agreement in South Carolina

2024-12-03 - Vision RNG says it will produce either RNG or power from South Carolina landfill gas.

Vision RNG Secures $207MM to Convert Landfill Gas to RNG

2024-10-17 - Vision RNG has secured funding from climate investor HASI to convert landfill gas to RNG in Ohio.

Ameresco, Republic Services Begin Operations at Illinois RNG Plant

2024-12-09 - The plant, in Edwardsville, Illinois, uses previously flared landfill gas to create renewable natural gas that will displace fossil fuel in a nearby Energy Transfer natural gas pipeline, the companies said.

Energy Transition in Motion (Week of Oct. 18, 2024)

2024-10-18 - Here is a look at some of this week’s renewable energy news, including approval of a 2-gigawatt geothermal project in Utah.

Canada Awards EverGen’s GrowTEC $2MM for RNG Project

2024-10-15 - The funding will go towards the second phase of a project at the Grow the Energy Circle (GrowTEC) biogas facility to increase production capacity to up to 120,000 gigajoules annually.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.