The price of Brent crude ended the week at $82.79 after closing the previous week at $82.82. The price of WTI ended the week at $78.26 after closing the previous week at $77.98. The price of DME Oman crude ended the week at $83.53 after closing the previous week at $83.19.

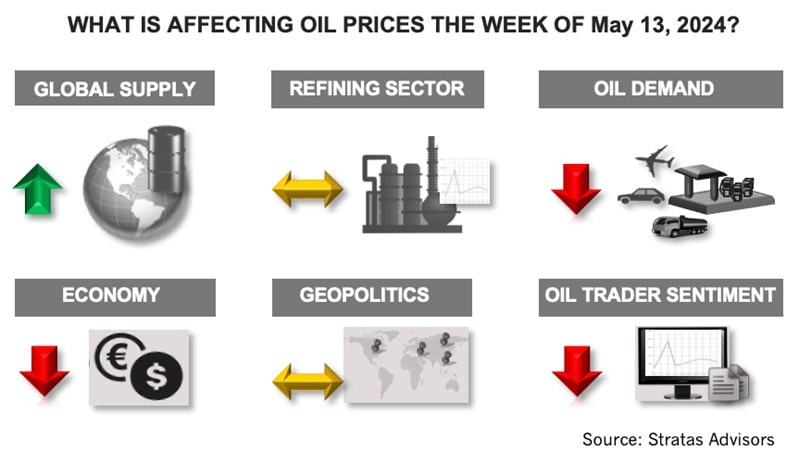

Most of the factors driving oil prices are becoming negative, including the sentiment of oil traders.

The net long positions of WTI traders decreased last week for the fourth consecutive week with traders reducing their long positions while increasing their short positions. During the last four weeks, the net long positions of WTI traders have declined by nearly 51%. The net long position of Brent traders also decreased last week with traders reducing their long positions while increasing their short positions. Additionally, recent economic news continues to be disappointing, including economic news for the U.S. The preliminary results for the May reading of the University of Michigan Consumer Sentiment came in at 67.4, which is a significant decrease from 77.2 in April, and is the lowest reading in six months. The decrease in sentiment was consistent across age, income and education groups and was the result of concerns about inflation, unemployment and interest rates.

- The expectations for inflation over the next year increased from 3.2% in April to 3.5%. The inflation expectations are well above the 2.3-3% range for the two years before the COVID-19 pandemic. The inflation expectations are also well above the 2% inflation target of the Federal Reserve.

- While the latest headline unemployment rate was 3.9%, the U6 unemployment rate (includes discouraged workers and part-time workers who desire to have full-time jobs) increased to 7.4%, which is the highest level since November 2021. Additionally, there has been no widespread rebound in the manufacturing sector and manufacturing jobs. The ISM manufacturing PMI for April decreased to 49.2 from 50.3 in March, which was the first reading above 50 (indicates expansion) since September 2022. The disappointing PMI for the manufacturing sector is consistent with only 8,000 manufacturing jobs being added in April and there have been essentially zero net manufacturing jobs added since October 2022.

- The U.S. 10-Year Treasury ended the week at 4.460, which is down from the previous week of 4.518%. While interest rates have recently drifted lower, interest rates remain high (with respect to the previous 25 years), including 30-year fixed mortgage rates. During the first week of May 2020, the 30-year fixed mortgage rate was 3.26%, which compares to 7.17% during the first week of May 2024, which effectively doubles the cost of buying a similarly priced house.

The one factor providing support for oil prices is the outlook for supply. We are maintaining our view, initially stated in early April, that OPEC+ will maintain its production cuts through the rest of the year. Over the weekend, it was reported by Reuters that Iraq’s oil minister stated that Iraq would not agree to any additional cuts at the upcoming OPEC+ meeting. While it was not clear if he was referring to extending the existing production cuts or further production cuts, we think the rationale for maintaining the cuts is too compelling – the drop in oil prices, the elevated breakeven fiscal oil price for oil producers, including Saudi Arabia, and the disappointing (from OPEC+’s perspective) oil demand growth so far this year. The next OPEC+ meeting is scheduled for the beginning of June.

Additionally, we are forecasting that growth in non-OPEC supply will increase by only 1.19 MMbbl/d in 2024, which is significantly lower than in 2023. The latest Energy Information Administration report indicated that U.S. oil production was 13.1 MMbbl/d, which is unchanged from the previous eight weeks. Last week, the number of operating oil rigs in the U.S. decreased by three and now stands at 496, which compares to the pre-COVID level of 683 that occurred during the week of March 13, 2020. One year ago, the U.S. oil rig count was 586. As part of the non-OPEC forecast, we are currently forecasting that U.S. oil production will average 13.5 MMbbl/d in 2024. This forecast has downside risk unless U.S. production picks up significantly during the rest of the year, as it did in 2023. At the beginning of 2023, U.S. production was 12.2 MMbbl/d and production remained flat through most of May. By the end of 2023, U.S. production, however, had reached 13.2 MMbbl/d. For 2024, increasing supply will be more challenging unless U.S. producers start ramping up their capex and drilling programs beyond their current plans.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paisie, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Exxon Seeks Permit for its Eighth Oil, Gas Project in Guyana as Output Rises

2025-02-12 - A consortium led by Exxon Mobil has requested environmental permits from Guyana for its eighth project, the first that will generate gas not linked to oil production.

US Drillers Cut Oil, Gas Rigs for First Time in Six Weeks

2025-01-10 - The oil and gas rig count fell by five to 584 in the week to Jan. 10, the lowest since November.

US Oil and Gas Rig Count Rises to Highest Since June, Says Baker Hughes

2025-02-21 - Despite this week's rig increase, Baker Hughes said the total count was still down 34, or 5% below this time last year.

US Drillers Cut Oil, Gas Rigs for First Time in Six Weeks

2025-03-07 - Baker Hughes said this week's decline puts the total rig count down 30, or 5% below this time last year.

US Drillers Cut Oil, Gas Rigs to Lowest Since December 2021, Baker Hughes Says

2025-01-17 - The oil and gas rig count fell by four to 580 in the week to Jan. 17.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.