Scott Smith’s Louisiana-based crude hauling company, Falco Energy Transportation LLC, had been in business for about two years when he realized that some obscure place known as the Bakken Shale was on the verge of producing prodigious volumes of oil. So Smith did what he does—he set up shop in that cold, remote climate, hamstrung by limited pipeline presence and started transporting crude.

Hauling crude oil by truck is in Smith’s DNA. His dad, Clair S. Smith, was president and CEO of Shreveport, La.-based Falco Inc. and father and son had been involved in numerous iterations of transportation and trading companies bearing the Falco name since the early 1970s.

As crude production surged, Falco expanded into the Eagle Ford and Smith began shopping for an investor to help grow the business. This being the golden age of midstream investing, there were billions out there for the taking.

But Smith didn’t need billions for Falco, and he certainly had no need for an investor constantly peering over his shoulder. He needed a more modest amount from a financial partner able to engage at the appropriate level and allow his company to continue to ramp up operations, compete for more lucrative contracts and reduce its debt.

In the energy business, that kind of specific need requires you to know somebody, and Smith did: Carl Thomson, an industry veteran with long experience in the energy and transportation markets. Thomason knew somebody, too: Tony Annunziato, co-founder of EIV Capital, a private equity fund focused on the lower middle market.

“I met with multiple private equity firms,” Smith told Midstream Business. “I just had a high comfort level [with EIV] because of the friendships and primarily, at the time their shop was a $50 million shop and I could get quite a bit of attention from Patti and the crew.”

Finding its niche

Patti is Patricia Melcher, managing partner of EIV and one of the few women running an energy industry private equity firm.

“Most midstream private equity funds are much larger and are looking to invest in the hundreds of millions for any one company,” Melcher told Midstream Business. “Being in this lower middle market we see a lot of niche opportunities. We are interested in traditional midstream investments like maybe a 50- or 60-mile piece of pipeline, a gas processing facility or maybe trucking operations or barge operations; anything that is transportation, logistics or processing related.”

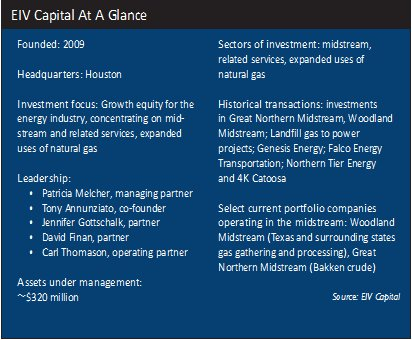

Houston-based EIV, formed in 2009, derives its competitive advantage from a small, but experienced, hands-on management team that is willing to spend more time with partners who need less capital than most institutional private equity firms are looking to invest.

“We’re attractive to portfolio companies and entrepreneurial management teams because of our experience,” she said. “We’ve started and operated our own companies; we’ve grown them; we’ve exited them. We’re a lot more collaborative with and available to our partners, as they need us; and have a lot more operational experience than a lot of the alternative sources of capital.”

That collective background allows the EIV team to quickly understand a potential partner’s business, identify challenges and gauge what is needed. Size matters, and in the case of EIV, small and nimble is an advantage. “I think that it’s attractive in the space where we play because they’re small teams,” Melcher said. “They’re typically experienced management, but they may not have a full suite of upper-level management. We can get more hands-on or provide more direct experience and help for them than they might typically find.”

Like Falco’s case, in which the need was for financial structuring expertise.

“One of the things about a small shop is that you always lack the CFO role,” Smith said. “[EIV] helped financially a lot. We were able to keep just a controller on board.”

For example, EIV devised a creative plan so that Falco could put more trucks into the field in a hurry to be able to capture a contract. EIV formed a leasing company that bought and leased 12 trucks to Falco in a very short period of time.

“They were very attentive in the financial arena and any time that something had to be done in a hurry, they were just very nimble and quick,” Smith said. “That was what we had to have as a startup.”

Not just number crunchers

That was not the only time that the EIV team revealed a skill set that surpassed spreadsheets.

In first-quarter 2011, the market prices of Brent and West Texas Intermediate (WTI) experienced a sharp divergence, with Brent shooting up to about$100 per barrel (bbl) while WTI lingered at around $80 per bbl. Many in the industry attributed the spread to geopolitical tensions, most notably the Arab Spring. EIV’s team not only identified the cause of the dichotomy for what it was—insufficient infrastructure to move rising crude production to market—it acted on it.

“We actually went out and leased a terminal that had a barge dock,” Melcher said. EIV had truck unloading stations installed, then proceeded to buy oil in Oklahoma, truck it to the terminal, load it onto barges at Tulsa’s Port of Catoosa on the Verdigris River and sell it directly to refineries, thus capturing the arbitrage. The barges traveled from the Verdigris to the Arkansas River, and finally to the Mississippi River, where the crude was sold to refineries in southern Louisiana.

“Because we had to enter into long-term contracts on the barges and the terminals, we put in place a hedging program,” she said. “We put hedges in place so that if this spread collapsed at any point, we could collect enough on the hedges to cover all our obligations and make some profit.”

The whirlwind project took about three to four months to put together and was a vivid demonstration of the little firm’s ability to convert insight into tangible results. More than just profit, the project earned EIV no small amount of credibility with portfolio companies.

“When we talk about this project that we put together, and all of the pieces that we were able to do, they see that we are not just a source of capital, but we also bring something to the table in terms of our experience and how we can be helpful to them as they execute their business plans,” Melcher said.

A little cash from my friends

EIV’s equity investment size ranges from$20 million to $60 million, though it is willing to invest as little as $10 million for opportunities that intrigue the team, and can reach as high as $80 million or more with co-investment from its partners. Each fund targets eight to 12 investments to provide EIV with the time required to be a resource and sounding board for its management teams.

“Our first fund was $50 million, and we found that we were definitely under-capitalized,” Melcher said. “Our second fund, which we closed in December, is about $270 million. We were fortunate to attract some really brand name institutions to be our investor partners.”

The firm seeks to invest the majority of its capital in traditional midstream businesses like transportation, logistics and processing. It also pursues deals in businesses like oilfield services related to the midstream. These investment opportunities are usually post-completion related or along the lines of flare reduction or water logistics and cleanup.

“We’re interested in what we call the expanded uses of natural gas,” Melcher said. Among those are landfill gas-to-energy projects, in which landfill gas and natural gas are processed and used for power generation. The electricity is then sold under long-term, fixed-fee offtake agreements, eliminating commodity price risk. EIV is also looking at gas-to-liquids types of opportunities, as well as logistics in the petrochemical space, and other select projects in the downstream space that follow midstream-like commercial arrangements.

Knowing when to leave

Typically, EIV invests with a five- to seven-year horizon, a comfortable time frame in which to invest, work with management to execute its growth plan and choose a good time to exit and give way to an MLP or other yield-type company.

“It works very well in our space where we can invest in the smaller companies, grow them to a point that they are attractive acquisitions to much larger MLPs,” Melcher said. “There’s a lot of capital out there in the private equity space focused on the midstream. It takes a lot of work to invest in the smaller opportunities. We focus on helping entrepreneurs in this space because it is what we enjoy doing. It’s very effective also for the larger acquirers if our teams can manage through the growth cycle and exit to them with a stable set of cash flows.” Melcher makes sure that the company’s management is aligned with the exit strategy well before EIV makes the investment.

Sometimes, though, it just happens. In Smith’s case, Falco was not for sale. “We were busy growing the company and were approached by JP Energy,” he said of the natural gas company. “They wanted to get into the crude oil space. We had a mutual friend at JP. They contacted us, and we entered into private negotiations and a company that wasn’t for sale, was for sale,” and sold in 2013.

Limited risk

The EIV senior investment team brings various backgrounds to the negotiating table:

- Co-founder Tony Annunziato was a commodities trader and hedge fund manager;

- Melcher was in investment banking and private equity;

- Partner Jennifer Gottschalk was a consultant across the energy value chain, including petrochemicals, and ran her own midstream company;

- Operating partner Carl Thomason is a longtime industry entrepreneur and executive; and

New partner David Finan brings considerable experience in investment banking and private equity.

That kind of experience can breed a “keep calm and invest on” attitude when encountering an industry down-cycle, but EIV’s basic strategy—in good times and bad—is to avoid taking commodity price risk.

“Everything we do, we look to mitigate commodity price exposure,” Melcher said. “We look to use long-term contracts or any number of tools to mitigate that commodity price risk exposure but still leave up-side so that we can generate private equity returns.”

Which is why EIV continues to roll during this period of commodity price struggles.

Downturn opportunity

“I look at this downturn in prices as more of an opportunity,” she said. “I don’t know how long it will last. I don’t know if prices will go up or down, but there are still opportunities, there are still companies that need growth capital, and we are looking for those and looking for how to invest successfully despite oil prices.”

The company finds its investments through management’s personal and professional networks, not investment banks. Like the Falco investment, most of EIV’s deals grow through a referral from someone who knows the firm and wants to connect it to an entrepreneur in need of capital.

Before the deal is done, EIV does its homework in evaluating the quality of a management team. “We spend a lot of time getting to know them before we invest with them,” Melcher said. “We want to be sure that their ethics and values are aligned with ours. It’s very important that they have their capital invested so that there’s alignment between our investors and our management teams.”

Beyond the strategic alignment, she wants there to be trust and communication between her team and the management team. The last thing the investor needs is to be the last to know when things go south.

“We want to create an environment where we really work together well, where they are willing to keep us in the loop, where they’re not afraid to tell us things,” she said. “When you’re building a company or building a project, things always have their bumps, so we work through them and get ahead of them.”

EIV’s approach made its investment in Falco Energy Transportation, now known as JP Falco, a success.

“The personal relationship that they have with their partner is just very good,” Smith said. “They’re very attentive, but—a lot of guys will be concerned about them being in your business on a day-to-day basis—and they’re not that. Those are keys that I’m looking at when I’m looking at a private equity partner.”

There are few, if any other private equity firms in midstream’s lower middle market space, and Melcher is fine with keeping it that way.

“I’d like stay in this lower middle market; I think that’s where we’re effective,” she said. “The next fund may be a bit bigger but I don’t see us going more than $400 million or $500 million. I think that’s the sweet spot. It’s the part of the market we really enjoy.”

Recommended Reading

ChampionX’s Aerial Optical Gas Imaging Platform Secures EPA Approval

2025-03-05 - ChampionX Corp.’s aerial optical gas imaging platform combines optical technology with a gimbal system to detect and locate methane leaks.

Baker Hughes, Woodside Partner to Scale Net Power Platform

2025-03-06 - Net Power’s platform uses natural gas to generate power while capturing nearly all CO2 emissions, Baker Hughes said in a news release.

Equigas, CO2Meter to Partner in Offering Gaslab Detection Devices

2025-02-14 - The devices are used in industrial operations to monitor gas leaks and maintain air quality and safety compliance.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.