Higher demand for oil, gas and coal will delay peak emissions past 2030 and push the world beyond Wood Mackenzie’s base transition case and closer to a 3 C pathway, the consultancy said in a new report. (Source: Shutterstock.com)

The chance to reach milestones over the next several years—goals needed to reach 2050 net-zero emissions targets—are slipping further and further away.

Geopolitical conflicts, trade tensions, changing investor appetites and the need to up infrastructure investments to $3.5 trillion annually have all had a hand in derailing plans.

However, analysts at Wood Mackenzie say it’s not too late to hit 2050 net-zero targets, according to its annual energy transition outlook released Oct. 29. The road is long; it’ll take policy certainty, a doubling of annual investments and continued innovation to get there—even as energy demand rises, they say.

“The world is running out of time to achieve net zero. We’re today in the middle of the 2020s. This is a decade that’s pivotal to accelerate the energy transition,” Jonathan Sultoon, head of markets and energy transitions for Wood Mackenzie, said during a media briefing. “And no major countries and very few companies are actually on track to meet their 2030 climate goals. Even the most altruistic, if you like, are actually seeing some sort of setbacks.”

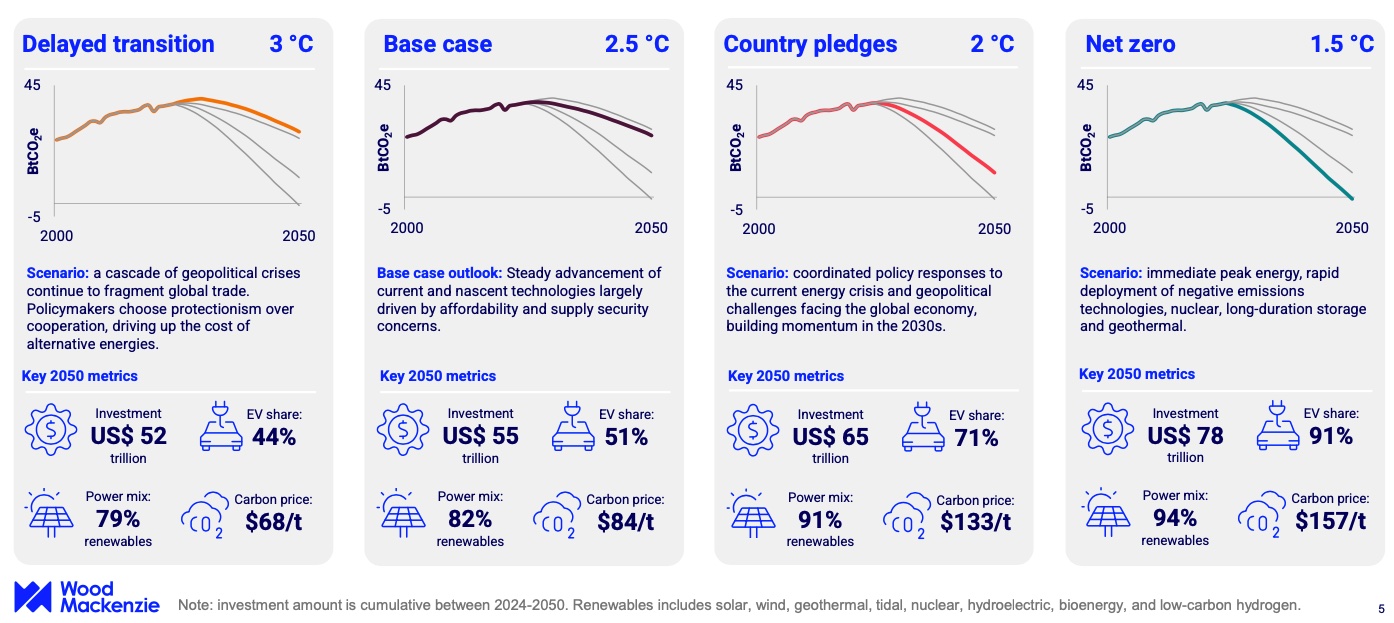

The energy consultancy’s outlook explored four potential emissions trajectories in its assessment, and included for the first time a delayed transition outlook in which geopolitical crises continue to impact trade, ultimately leading to higher alternative energy costs and a potential 3 C increase in global warming.

“In order to get to two degrees, one and a half degrees and a net zero pathway, global emissions need to fall immediately, and they’ve actually been continuing to rise over the last two to three years,” Sultoon said. In the base case, which calls for 2.5 C of warming, CO2 emissions don’t start falling until 2027, despite efforts being made in parts of the world. “The risks are increasing that we actually get to that potentially catastrophic 3-degree pathway in which emissions don’t really peak until 2030.”

‘Stark choice is here’

Despite growth in renewables capacity and emissions reductions in some countries, the overall transition is being slowed by ongoing conflicts in the Middle East and Russia-Ukraine war, along with political uncertainty in the U.S., according to Wood Mackenzie. Trade tensions involving China are further contributing, which dominates low-cost clean technology production and critical materials supply chains, among others.

“A stark choice is here now: either the rest of the world needs to rely on Chinese manufacturing to speed the transition,” Sultoon said. Or continued reliance on China means “the West will pay a higher cost or in fact delay the transition.”

Wood Mackenzie’s base case estimates $55 trillion in investments will be needed to limit warming to 2.5 C. Under this scenario, renewables make up 82% of the power mix and there is a $84/ton carbon price. This compares to $78 trillion in investments required in the Paris Agreement’s net-zero target limiting global warming to 1.5 C. In that instance, renewables’ share of the power mix is 94% with a $157/ton carbon price.

Wood Mackenzie said infrastructure investments need to double to $3.5 trillion per year to get to net-zero emissions. At current levels, about two-thirds of that is being spent annually on clean energy infrastructure, he added.

“The frustration is that the transition is now slowing after a promising start,” Sultoon said.

Permitting delays have slowed deployment of clean energy infrastructure, leading to cost increases, and electorates are making compromises.

Analysts also attributed the slowed transition to low-carbon technologies that are not yet scalable, affordable or mature.

“A key constraint is the high cost of hydrogen, CCUS, SMR nuclear, long-duration energy storage and geothermal. Capital intensity is high, and the business case is weak without incentives,” the report stated. “Out of 3,000 announced hydrogen and CCUS projects, we estimate 30% have moved to operational or advanced development stage. Projects are facing delays due to a lack of firm offtake agreements, midstream infrastructure and cost inflation in the past two years. Policy certainty is crucial to unlock demand, and it may take longer to establish the use case.”

The numbers

Global emissions have risen by about 2% per year since 2020 as developing economies continue to rely on traditional fuels, including coal, according to David Brown, research director for Wood Mackenzie.

“However, that’s not to say there isn’t progress on low carbon supply,” he added.

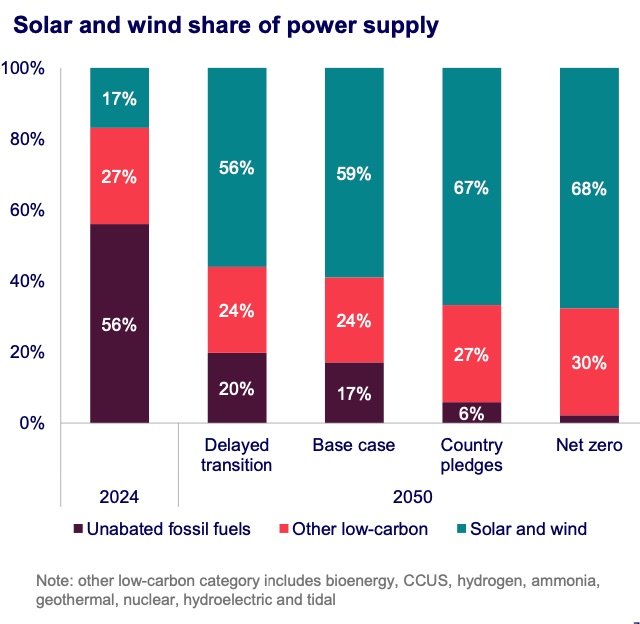

The share of solar and wind in the world’s power supply mix continues to increase, having grown from 4.5% in 2015 to 17% in 2024, according to the report.

“Global wind and solar capacity has surpassed 2500 gigawatts. About 47% of that capacity is in China. But upside of China, we’re seeing significant capacity additions, including in the United States,” Brown said.

The U.S. has become more resilient despite trade tariffs on Chinese-made equipment.

“One reason why we’re seeing continued investment in low carbon supply in the United States, despite trade tariffs, is that inventories for solar modules stand at around 35 GW right now. So, investors and companies have sufficient inventory to manage some of these trade tensions that we’re seeing,” Brown said. “Also, the sector has diversified outside of China into markets like Southeast Asia, and we’re also starting to see the emergence of a U.S. manufacturing base for solar and wind. Early days still there, of course, but we see that capacity growth maturing around 2030 and into the late 2040 period.”

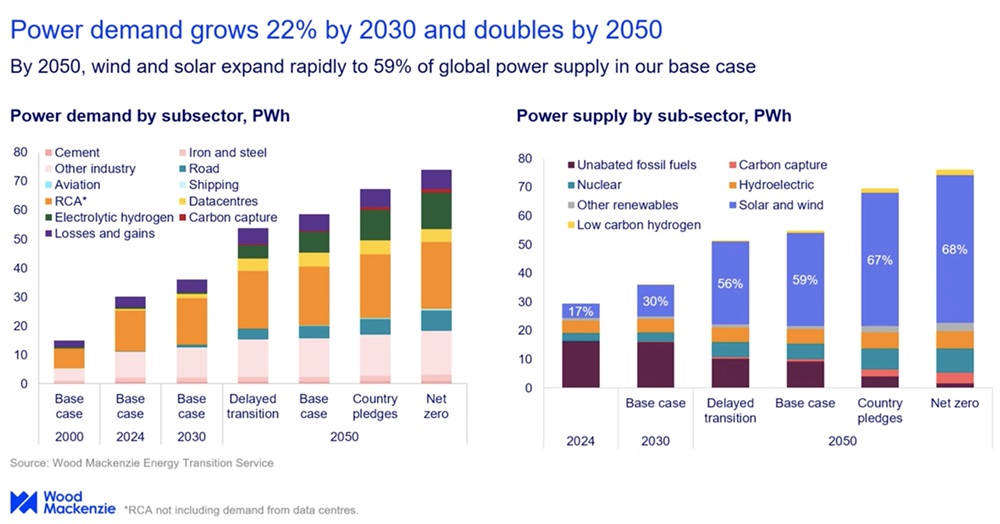

In each scenario, Wood Mackenzie sees renewable and nuclear increasing. Solar continues to drive growth, followed by wind, nuclear and hydro. Their share of the electricity supply mix is expected to rise from 41% today to between 47% and 58% by 2030 and between 80% and 90% by 2050.

EV sales are also forecast to continue rising.

However, Prakash Sharma, vice president, head of scenarios and technologies for Wood Mackenzie, pointed out in a news release that “any number of challenges—from the supply chain, critical minerals supply, permitting and power grid expansion—could dampen aspirations for renewables capacity.”

The challenges are being faced as power demand rises. Global energy demand is forecast to grow by up to 14% by 2050, according to report. For economies with rising populations, energy demand could grow by 45%.

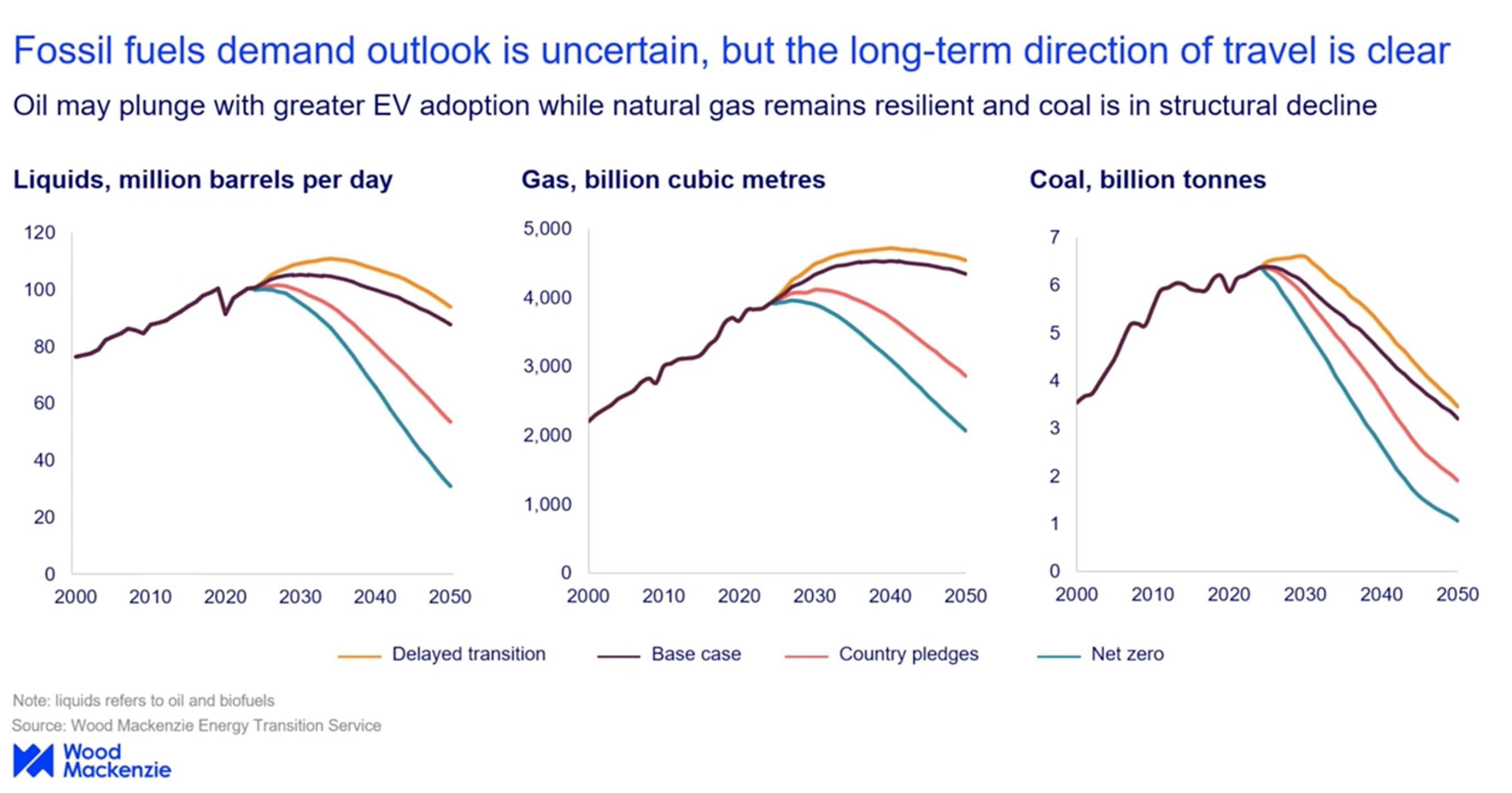

Given electrification also faces challenges, including long development time for transmission infrastructure, fossil fuels are expected to continue helping with power needs.

“A slower pace of electrification would mean more energy consumption met by fossil fuels,” according to the report. “Higher demand for oil, gas and coal will delay peak emissions to post-2030 and push the world beyond our base case and closer to a 3 C pathway.”

Brown added Wood Mackenzie believes natural gas is the most resilient of the fossil fuels, saying the upside for U.S. natural gas demand by 2030, for example, is about 6 Bcf/d constrained by infrastructure and permitting.

“The Mountain Valley pipeline may be the last greenfield infrastructure to be [permanently] built at least for the next ten or so years,” Brown said before turning to natural gas infrastructure volume permitted in the U.S. “In 2023, it was around 4 Bcf/d. So, there is a mismatch between what infrastructure can provide and what commodity markets are demanding in terms of natural gas.”

Significant investment will be required across every scenario, Brown said.

Recommended Reading

E&Ps Pivot from the Pricey Permian

2025-02-01 - SM Energy, Ovintiv and Devon Energy were rumored to be hunting for Permian M&A—but they ultimately inked deals in cheaper basins. Experts say it’s a trend to watch as producers shrug off high Permian prices for runway in the Williston, Eagle Ford, the Uinta and the Montney.

Exxon Enlists Baker Hughes to Support Uaru, Whiptail Offshore Guyana

2025-02-03 - Baker Hughes’ will provide specialty chemicals and related services in support of the Uaru and Whiptail projects in the Stabroek Block.

Tamboran, Falcon JV Plan Beetaloo Development Area of Up to 4.5MM Acres

2025-01-24 - A joint venture in the Beetalo Basin between Tamboran Resources Corp. and Falcon Oil & Gas could expand a strategic development spanning 4.52 million acres, Falcon said.

New Fortress Signs 20-Year Supply Deal for Puerto Rican Power Plant

2025-01-23 - The power plant, expected to come online in 2028, will be the first built in Puerto Rico since 1995, New Fortress said.

TGS to Conduct Ocean-Bottom Node Survey Offshore Trinidad

2025-04-07 - TGS has awarded a client a shallow water ocean bottom node contract offshore Trinidad.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.