Encana’s RAB pad in the Permian Basin is one example of its multiwell activity.

[Editor's note: A version of this story appears in the July 2018 edition of Oil and Gas Investor. Subscribe to the magazine here.]

During his career, Doug Suttles has seen plenty of ups and downs, but none worse than the most recent one.

His grandfather moved to Midland in 1933—even then, the Permian Basin was one of the most productive oil provinces in the U.S. Suttles grew up in Midland; his father was in the oil business, and his daughter has joined the business as well.

After working at Exxon in the late 1980s, Suttles joined BP to serve in a number of roles here and abroad, eventually becoming COO of BP Exploration & Production Co. and president of BP Alaska. Since 2007, he has served on the University of Texas Engineering Advisory Board, where he has also been honored as a distinguished engineering alumnus.

As president and CEO of Encana Corp. (NYSE: ECA) since June 2013, he faced tough choices born of what he calls “inconvenient facts,” not least of which was cutting the staff dramatically while he whittled the vast portfolio down to four high-margin plays: the Permian and Eagle Ford in the U.S. and the Montney and Duvernay in Canada.

This year the budget is allocated about evenly between the Permian and the Montney, although in the first quarter, he increased the Eagle Ford count to three rigs from one and is pursuing the Austin Chalk as well.

Suttles joined Encana when oil was headed to $100 a barrel (bbl) and beyond—but the natural gas-heavy company was beginning to suffer from the bust in gas prices. That November he released a new company strategy based on the four growth plays and announced the goal of operating within cash flow.

“The concept was that we wanted to build an oil and gas company that would be successful in any commodity environment, and … never be the marginal barrel,” he told the Houston Producers Forum recently. “As an engineer, I do know that there’s always a straight line from A to B, but they do not make a forecast!”

Indeed, the path to better financial results and a new corporate culture was not straight. “We asked ourselves, ‘Where do we think we should be if we want to be successful?’ We came to the conclusion that unconventionals in North America had a bright future. The emergence of shale has disrupted the entire industry … and it presented a material opportunity at scale right here in North America. We also liked that it was short-cycle capital.”

Tightening The Portfolio

Suttles said he told company managers that they had to face inconvenient facts.

“In 2013, we had a very large gas position in western Canada, and then, unfortunately, this thing called Appalachia arrived, and no matter how good you were, you could not beat that. I asked them, ‘Do you realize what 20 Bcf [billion cubic feet] a day really is? That’s the largest gas field in the world and it’s only getting bigger.’”

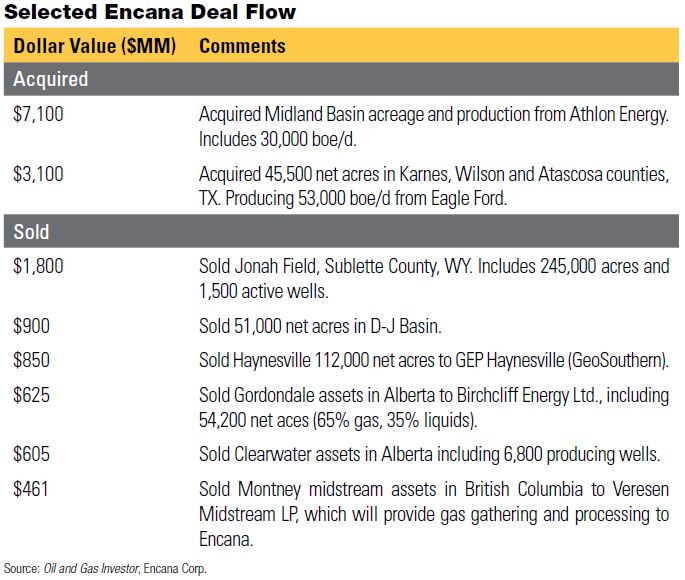

The decision was to sell some prized Canadian and U.S. gas assets, add NGL to the portfolio and focus much more on oily plays. Since 2014, the grand repositioning has entailed selling more than $11 billion of assets and acquiring $10 billion while powering through excruciating layoffs. The Calgary company is still the largest gas producer in Canada and the second or third largest in the U.S., with some 800 people based in Denver.

Suttles described the many challenges the company has endured while he changed the corporate culture. “When I joined in June 2013, we were in 28 different plays in North America and had 4,500 employees. We were in the North Sea and Ecuador. Debt was $7 billion.

“Today our G&A has totally shifted, and we are seeing a margin per barrel that is higher than it actually was in 2013 when oil was $100 and gas was $4,” he said. Debt is down to $3 billion.

Suttles set out to act in first-half 2014 (when the market was topping out, before the OPEC surprise in November that tanked oil prices). Encana paid $3.1 billion to acquire Eagle Ford Shale assets from Freeport-McMoRan Gold, including 45,000 net acres in three Texas counties. At the same time, it sold its interests in the much-vaunted Jonah gas field in Wyoming for $1.8 billion to a partnership between TPG Capital and Jonah Energy LLC. The company had been the biggest gas producer in Wyoming.

But the largest corporate merger of 2014 turned out to have Encana’s name on it, too: That November it purchased Athlon Energy Inc. of Midland for $7.1 billion. It gained 140,000 net acres in the Midland Basin, with production of 32,000 barrels of oil equivalent (boe/d). Many thought it had overpaid because oil was around $100/bbl at the time.

“We saw lots and lots of upside in the Permian and it fit our skill set,” Suttles said.

“Everything in your enterprise has to follow your strategy—you can’t bolt your strategy onto the stuff, you have to have the strategy first. You have to be more nimble than a major, and I can say that because I came from a major.”

Suttles said he is pleased with the results of the transition. In 2018, top line production will grow 30% year-over-year companywide, and by the same percentage in the Permian Basin alone. Encana produces about 330,000 bbl/d, but Suttles said that later this year, it will cross an important threshold of more than 400,000 bbl/d on a budget of $1.8 billion (all figures in U.S. dollars). It could be producing up to 425,000 bbl/d by year-end. It has five rigs running in the U.S.

Encana’s RAB pad in the Permian Basin is one example of its multiwell activity.

“One of the things I’m most proud of is that our average margin per barrel is actually higher now than it was in 2013—that was big. In fact, one time in 2013 when I was in Houston visiting with another CEO, he asked me, ‘Doug, what’s your netback per barrel?’ and I said it was $14. He said, ‘Mine’s $47.’ And I said, ‘Bummer.’”

Cultural Changes

When Suttles saw that Encana had to become more efficient and operate with higher margins, culture changes were also in order, just as much as buying and selling assets.

“We asked ourselves, ‘What is the culture that allows us to be sustainable?’ This was the hardest thing we did; we looked at it really deeply and spent a lot of time on this.

“We came up with three simple values: We are one, agile and driven. One: we are all on one team and if Encana wins, then everybody wins. All our decisions have to be aligned. Two: agility. Innovation is such a powerful force in our industry, so we have to be able to try new things, move quickly, and from that what emerges are opportunities.

“Lastly is driven. I talked to some people in the company who said they were trying hard, but this is not little league soccer where everybody gets a trophy. We have to get to the finish line, and it’s about perseverance.”

Suttles said he wanted employees to realize how things could change by the way the management team acted. The company had to do four basic things well, he said. First was to have good rocks in the right places. Second was to improve operating performance. (The best players in any play are 40% more efficient than the average, he said.)

Third, it had to manage margins through adept marketing and hedging, to control the price obtained for its products. The last thing was, and is, capital allocation. “I would encourage all of you to say ‘No.’ That’s the most important word in capital allocation,” he told attendees.

Permian Cubes

Since the Athlon deal, Encana has done 14 more transactions to core up and enable longer lateral drilling in what it calls the cube, meaning it spaces and stacks multiple wells across multiple landing zones and watches how these react over time. It has some drill pads accommodating up to 64 wells.

The company is one of three in North America to have drilled 5,000 horizontal wells, Suttles said. “All we do is multistage fracturing.”

In the first quarter, in Martin County, for example, one cube had 10 wells that averaged 1,300 boe/d in the first 90 days. In Midland County, an eight-well cube averaged 1,500 boe/d over 30 days.

Today in the Permian, Encana boasts 12,000 locations, 3,450 of which it deems premium ones that could generate an after-tax rate of return of more than 35% at $50 WTI and $3 gas. (This is based on 450- to 660-foot well spacing, and some 40% of these will be drilled out to 10,000 feet horizontally.) The bulk of the acreage is in Martin, Midland, Howard and Glasscock counties. The company is testing the Jo Mills, Middle Spraberry and Wolfcamp C zones.

In first-quarter 2018, Encana produced 55,700 bbl/d out of the Midland Basin. It has 25,000 bbl/d of firm takeaway lined up to Houston, as well as 31,000 bbl/d hedged at $0.81/bbl for this year to offset the basis differential. Between the pipeline capacity and hedges, analysts say, it will deliver peer-leading free cash flow in 2019, and it is not exposed to the widening Midland crude price discount.

In a May research note, Tudor, Pickering, Holt & Co. analysts said they were “encouraged by consistent Permian performance these past few quarters, Permian marketing and Montney gas plant planned start-ups supportive of near-term growth plans and execution thus far on the long-term outlook including share repurchases.

“Our price deck true-up and inventory tweaks have increased our NAV by +$3/share to $14/share in our updated model … We’re watching for longer-dated cube production in both the Permian and Montney to further de-risk inventory and drive quarterly results from the company's core assets.”

Morgan Stanley vice president Benny Wong still recommends investors remain overweight Encana, and he has confidence in the path toward free cash flow in 2019. In his view, the company will graduate from a growth-focused E&P to a vehicle that provides total shareholder return via dividends and stock buybacks while growing production.

Leslie Haines can be reached at lhaines@hartenergy.com.

Recommended Reading

ChampionX’s Aerial Optical Gas Imaging Platform Secures EPA Approval

2025-03-05 - ChampionX Corp.’s aerial optical gas imaging platform combines optical technology with a gimbal system to detect and locate methane leaks.

Baker Hughes, Woodside Partner to Scale Net Power Platform

2025-03-06 - Net Power’s platform uses natural gas to generate power while capturing nearly all CO2 emissions, Baker Hughes said in a news release.

Montana Renewables Closes $1.44B DOE Loan for Facility Expansion

2025-01-13 - The expansion project will lift annual production capacity to about 300 million gallons of sustainable aviation fuel (SAF) and 330 million gallons of combined SAF and renewable diesel.

BP Monitoring Air Following Leak at Whiting Refinery

2024-12-27 - BP says the Midwest refinery is now operating normally.

Equigas, CO2Meter to Partner in Offering Gaslab Detection Devices

2025-02-14 - The devices are used in industrial operations to monitor gas leaks and maintain air quality and safety compliance.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.