Energy Transfer Leads the Midstream Consolidation Flow

Energy Transfer co-CEOs discuss pipeline pain points, needed M&A, regulatory woes and much more in this Midstream Business exclusive.

Energy Transfer co-CEOs Tom Long, left, and Mackie McCrea took the reins of the midstream giant in late 2020 and have since presided over acquisitions totaling more than $26 billion. (Tom Fox/Hart Energy)

Midstream magnate Kelcy Warren handed Energy Transfer’s metaphorical baton—or pipe—to right-hand men Mackie McCrea and Tom Long in the height of the pandemic and amid much industry uncertainty after announcing them as co-CEOs in October 2020.

At the time, ET traded at about $6 per unit during the temporary COVID-19 bust. Now it’s nearly triple that value as Energy Transfer leads the newest wave of industry consolidation and organic growth in the midstream sector, including its ongoing control of Sunoco and USA Compression Partners.

Earlier this year, Sunoco scooped up NuStar Energy for $7.3 billion. ET-controlled Sunoco promptly joined with Energy Transfer to form a new Permian Basin crude oil and produced water joint venture, utilizing much of those NuStar assets.

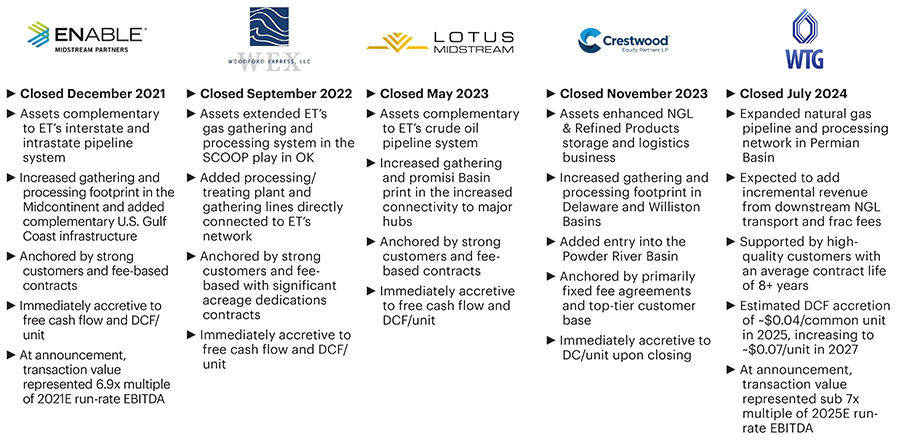

Energy Transfer's run of midstream consolidation since 2021. (Source: Energy Transfer)

And they’re not about to stop. McCrea and Long insisted much more midstream M&A is still required, and that ET will continue to stand out as the leader in the consolidation space.

Even when [consolidation] wasn’t the popular thing to do, we never stopped talking about it, we never stopped pursuing it, and look where it’s gotten us. And now, all of a sudden, it’s the thing that the others are trying to play catch-up on.—Tom Long, co-CEO, Energy Transfer

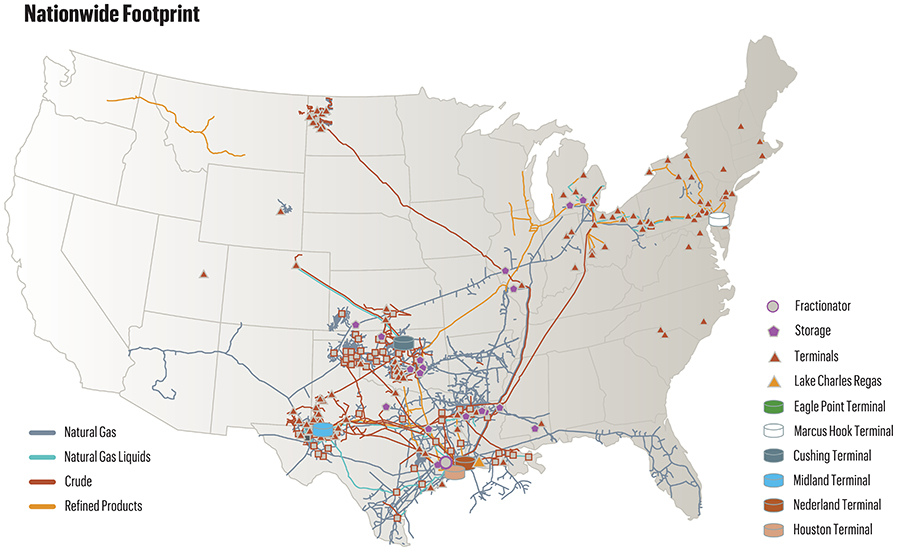

Energy Transfer increasingly has a dominant Permian presence—from gathering and processing systems to long-haul pipe—and strong positions in every key oil and gas basin in the country. ET also continues to grow in the burgeoning liquids and LNG export markets along the Texas-Louisiana Gulf Coast.

Warren, who remains executive chairman, grew ET aggressively from its birth nearly 30 years ago. McCrea joined Energy Transfer nearly from the beginning in 1997 as a senior vice president, working his way up to president and chief commercial officer before taking on the co-CEO role. Long signed on in 2015 and served as CFO for about five years.

The two can balance each other out on the operating and financial sides while leading business strategies together for an empire of more than 130,000 miles of pipeline and associated energy infrastructure spanning 44 states.

McCrea and Long sat down exclusively with Hart Energy’s editorial director, Jordan Blum, to discuss Energy Transfer, the state of the industry and changes on the horizon.

Energy Transfer co-CEOs Tom Long, left, and Mackie McCrea took the reins of the midstream giant in late 2020 and have since presided over acquisitions totaling more than $26 billion. (Source: Tom Fox/Hart Energy)

Jordan Blum: Starting a little broad, what’s your take on the overall state of the midstream sector in North America right now, especially U.S. shale, and, of course, Energy Transfer’s role there?

Mackie McCrea: From a macro level, what we see in the midstream industry is a lot of activity. There’s cryos [cryogenic gas plants] being built all over the Permian Basin. You’ve got pipelines being built or brought online in different areas of the United States. And, certainly, if you look at Energy Transfer specifically, we’re in that same boat. We’ve got a lot going on—building new pipe, proposing new pipes, adding export capabilities, adding cryos, etc. So, even despite what’s going on from an administration and political standpoint, where we are seeing a very difficult environment, the midstream [industry] is still thriving despite a lot of the hurdles that have been thrown up.

JB: What are the primary needs for the industry right now in terms of infrastructure gaps with growing demand and everything? I’m asking from the long-haul pipelines to whatever needs there are in terms of fractionation, blending and treating, etc., including a lot of the stuff that gets overlooked.

MM: I’ll focus on what we’re looking at, what our needs are, which of course is in much of the U.S., but I’ll start in the Permian. It’s probably the most prolific basin in the world from different aspects. There’s significant infrastructure needed out of there. There’s a lot of cryo being built. We’ve announced one and, more likely than not in the second half of this year, we’ll announce another one or so. We’ll see how that goes. In addition to that, there needs to be another [long-haul gas] pipeline. There’s a pipeline of 42 inches coming online here [Matterhorn Express Pipeline]. We hope that’s going to alleviate the pain for producers in the short term.

But we believe, within 18 to 24 months, if not sooner, it’s going to get tight again. So, there definitely needs to be more pipe built out of the Permian Basin, and we actually think there needs to be more pipes built in both directions eventually out of the Permian. That’s a big need. We believe there also needs to be another pipeline or more pipelines built out of East Texas and North Louisiana to feed into the growth along the Gulf Coast, certainly the LNG growth as well as other growth, and also connecting to pipelines that go more to the Southeast. And, additionally, there needs to be more pipelines built out of the Terryville [Louisiana] area where a lot of the big-inch pipelines come in there, and there needs to be more capacity built to the Southeast.

If you look at just NGLs, there’s been some announcement of NGLs coming out of the Permian Basin, and we certainly are needing to look very closely at what we’re going to do with our NGL growth. We already have a lot of growth. We already have a lot of third-party business. We’re adding cryos. We’ll need to be able to get those NGLs to Mont Belvieu [Texas], and a lot of that on the water. Finishing up, there’s a lot of production in this country and it cannot be absorbed and consumed in the United States, and there’s a dire need for LPG growth and natural gas growth throughout the world. So, there’s a significant importance for getting both natural gas and natural gas liquids on the water. We do see a continued growth feeding on what we’re already doing for export capacity for NGLs along the Gulf Coast.

(Source: Energy Transfer)

JB: Do you see crude oil pipeline capacity as being pretty solid, at least for now compared to greater needs for NGLs and gas?

MM: I think that sums it up very well. You look back around the pandemic times, and then where volumes have grown from there. Oil has kind of consistently grown moderately over the last three or four years, and gas has just exploded and taken off. So, we don’t really see a need short term for crude oil. Now, there are some rumors out there that there may be some repurposing of some crude pipes. So, there could be some things that happen where all of a sudden there’s a need. But, certainly, from our standpoint over the next year or two, we don’t see any rush for more crude capacity out of the Permian Basin.

JB: Is Energy Transfer looking at repurposing possibilities?

MM: What I was just referring to is not us, but we have teams that are looking at everything we own that’s underutilized. Would it make sense to put it into a different product service? Absolutely. We’re always making those analyses and reviews.

JB: Switching gears a little bit and, obviously, you’ve been very involved in this, but what’s your take on how midstream consolidation is unfolding? There’s been a big wave of upstream consolidation ongoing and it seems to be coming into midstream now. There’s fewer and fewer players with a handful dominating in the three Es—Energy Transfer, Enbridge and Enterprise Products Partners—and then a few others more gas- or NGL-focused in Kinder Morgan, Williams Cos., Targa Resources and ONEOK.

Tom Long: We are very, very excited about the whole consolidation that’s occurring. You can pretty much ask anyone out there when they talk about M&A, and Energy Transfer is going to be the first name that comes up as very, very active in this. Even when it wasn’t the popular thing to do, we never stopped talking about it, we never stopped pursuing it, and look where it’s gotten us. And now, all of a sudden, it’s the thing that the others are trying to play catch-up on. If you go back, not even that long ago to 2010 or so, we were really gas-focused. Then, you just saw us continue to make acquisition after acquisition that now has us in every commodity—not just natural gas, but all the natural gas liquids and the crude oil.

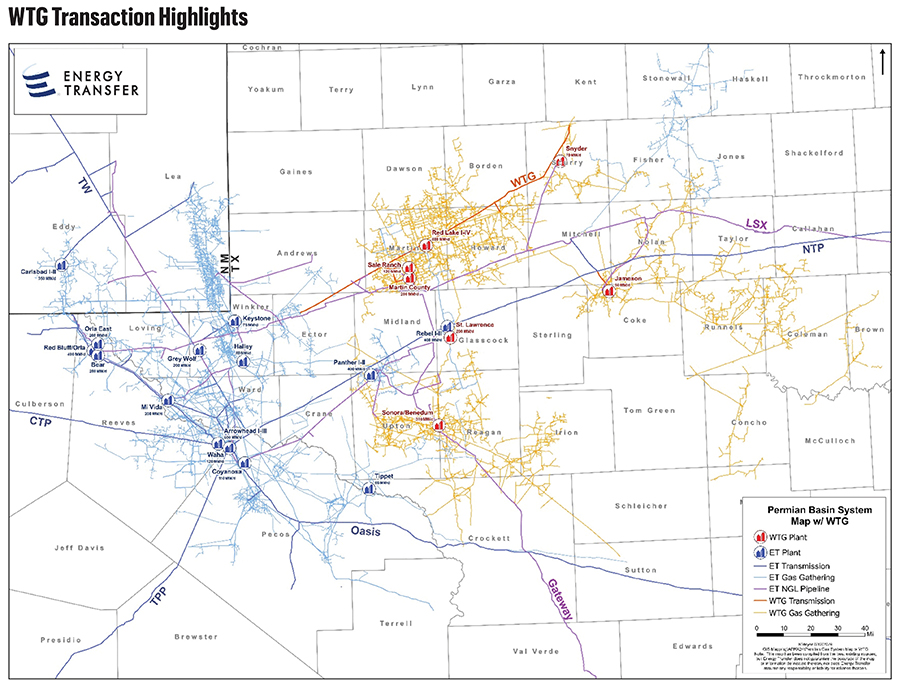

You can also see from a geographic standpoint how we’ve moved all the way to the wellhead and to the water and any markets in between, and also on the international front. We’re continuing to look at every aspect of it. I think you’re going to continue to see it, and you’re going to see that a lot of these were pretty small midstream companies that were started up by private equity firms. You’re not seeing private equity firms invest a whole lot more, and you’re actually seeing them exit. West Texas Gas [WTG] that we just closed on was a good example of that. We now have the ability to provide the broadest scope of services to the upstream customers. A lot of these others—when they look out and start thinking five, 10 years down the road—they’re kind of landlocked, they can’t really move upstream a whole lot more, and there’s not necessarily a whole lot more they can do downstream. They usually have to bring the product back to us to get to the markets. It’s just not a good place to be.

We’ve created an unbelievable footprint entity here that can participate in pretty much any market and have access to all the major producing basins. You’re also seeing what’s happening to our [upstream] customers with all the consolidation that’s occurring there. So, it makes sense. All in all, this M&A has been very good for the industry, and we feel like we were and still are the leader in the consolidation that’s occurring.

JB: Do you feel like you’re really strong in where you want to be in basically every basin now? You look at the map, and you’re basically everywhere, but is there anywhere you specifically still want to grow?

TL: That is a very commonly asked question. What they tack onto it is how much larger can you get without running into FTC [Federal Trade Commission] issues?

When you look at each one of these basins, we feel that there’s still enough competition. We still feel it makes sense as long as you have a few competitors in each area. Remember, we are not just natural gas. We’re natural gas liquids and crude oil. So, when you stack this up, you can look just about in any of these basins, and we feel like there’s still more we can do that does make sense, and we have no intention of slowing down here.

(Source: Energy Transfer)

JB: Delving into WTG, that makes you even stronger in the Midland Basin and farther east. I just wanted to see if I could get you to elaborate on just the fit there, but also for future positioning as Permian producers try to extend those sweet spots in Mitchell County and different areas. Does that position you well for the future as well as the present?

TL: Just continuing with what I was just rolling through, West Texas Gas, Crestwood, Lotus, Enable, those are the more recent ones. When you really look at how we go through the process here, we first look at a fit and then everything I talked about being in all the commodities and pretty much all the basins. It fits a pretty easy box to check when you really think about it. So now it comes down to if it’s accretive on a distributable cash flow per unit. We want to make sure that we’re creating value for our stakeholders, for our equity holders. And then the third thing we’ll look at is leverage. We want to make sure that we continue to create value for the debt side of our capital structure, meaning that we’re bringing leverage down and continuing to strengthen the balance sheet.

Once again, when you participate in all the commodities, it’s pretty easy to find a lot of value downstream of these acquisitions we make. A lot of these have been the ones, especially the most recent, that I call more in the gathering and processing side of the equation. We’re very excited about these, and they are clearly checking all the boxes.

MM: You look at WTG, you look at Crestwood, you look at Lotus, those were assets and companies that were in dire need of Energy Transfer. And what I mean by that, and Tom alluded to it, is they kind of were stuck. They gathered gas, they processed it, and then they gave it to some other parties. Now, we can go to those same producers that are already on the systems and attract new customers and we say, “Where do you want to go? Do you want to go to a power plant? Do you want go across the state with your gas to an LNG facility? Do you want to move your liquids to Mont Belvieu? Do you want your liquids exported?” So, it’s that next step from all these assets they really couldn’t do on their own. We’re really able to create some significant savings when we buy these companies, but also significant synergies. They will feed into our NGL network, they’ll feed into our intrastate and interstate networks, and they will also help our export projects in a big way.

TL: The way that we will talk to the Street about these is they were starved for capital. They didn’t have the balance sheet to do it and yet, talking to their commercial folks, they had a long list of projects that they would’ve loved to do. That’s what we bring to the table. And we are absolutely second to none when it comes to the operations side of it. We’ve got a formula here that’s working, and the market gets it. They see how successful we’ve been at this and, once again, we’re seeing some of our peers stop and take note of this. I think some are going to try a little bit harder to see what they can do, but it’s maybe a little too late.

But what we’re really doing, too, is gathering more crude to Dakota Access, and we’re bringing it to areas where Dakota Access is the outlet. With all the trouble we went through to get that [DAPL] in service, what a great asset that is for us, for our country, for refineries.—Mackie McCrea, co-CEO, Energy Transfer

The Mont Belvieu Facility is an integrated liquids storage and fractionation facility located 30 miles east of Houston along the U.S. Gulf Coast. The facility has strategic access to multiple Natural Gas Liquids (NGLs) and refined products pipelines, the Houston Ship Channel trading hub, and numerous chemical plants, refineries and fractionators. (Source: Energy Transfer)

JB: We talked about WTG. And you mentioned Lotus and Crestwood, which are all strong in the Permian. But Crestwood also has a big Williston Basin presence. What’s your take on growth in that region and supporting DAPL [Energy Transfer’s Dakota Access Pipeline]?

MM: We’re really excited about what’s going on up there. With prior acquisitions, we kind of got in the water business. But that [Crestwood] put us in a big way in the water, which is a big deal up in the Bakken. What it’s really doing is, and I can’t go into the specifics, but it’s giving us the opportunity to increase our processing business. When we bought Crestwood, they had assets that were available, but just weren’t full. So, we are negotiating, and hopefully finalizing soon, new deals to fill up those cryos. But what we’re really doing, too, is gathering more crude to Dakota Access, and we’re bringing it to areas where Dakota Access is the outlet. With all the trouble we went through to get that [DAPL] in service, what a great asset that is for us, for our country, for refineries. And we are the dominant player there. Regardless of how much the Bakken may grow, we will see most of that growth because of what we can offer to customers by delivering to the refineries in the Midcontinent or all the way down the Gulf Coast.

JB: I wanted to bounce around the other basins a little bit, too. Going back about three years, you grew in the Midcon and in the Haynesville Shale with Enable, and you have Gulf Run [Pipeline] online and some other projects. Can I get your thoughts on those basins as well?

Energy Transfer increasingly has a dominant Permian presence—from gathering and processing systems to long-haul pipe—and strong positions in every key oil and gas basin in the country. (Source: Energy Transfer)

MM: You look at a pipeline map, and you’ve got to get some gas out of Oklahoma or North Louisiana or the Permian or East Texas, and where can you go where one company can do all that? There’s only one company that can do that. So, we’re very bullish on our position to be able to accommodate whether it’s markets along the Gulf Coast or other areas of the U.S., or whether it’s producers trying to find the best outlet, most efficient, most profitable outlet for them and they’re looking at our assets, and certainly Enable helped that in a big way. That gave us a very good position, a better and stronger position across North Louisiana with the enormous reserves in Haynesville. And then it connected the dots by connecting the Oklahoma assets with our East Texas 42-inch assets that come into Carthage [Texas], with our 42-inch pipelines that come out of Carthage all the way to Terryville, with our Gulf Run that goes down and connects to Golden Pass [LNG], and some other projects that we have planned. So, Enable has been an incredible asset to us that continues to create value that we didn’t really even see when we were in the process of acquiring it.

JB: Earlier, you mentioned having pipes go more in both directions from the Permian. I know this is to serve growing domestic power demand and, therefore, natural gas demand for data centers and artificial intelligence. But the focus still remains on heading to the Gulf Coast for bullishness on LNG facilities, even if they’re going slower than you’d like.

MM: A lot of stuff that we’re working on is early stages and pretty confidential, but I guess it’s fair to say the growth is all over the United States for different needs of electricity. Certainly, a lot of things are going on, for example, in Arizona around data center growth and power plant demand. There’s a need—there’s a significant need—for more gas, certainly in California, and they’re going to import their stuff, but also more gas in Nevada and more gas in Arizona. So, we do see that as growth potential.

When you talk about natural gas transportation and natural gas delivery, we couldn’t feel better about where we sit and where the upside is for our assets. I mean, other than the Eastern Seaboard, there’s really no market area that we can’t touch with our significant intra- and interstate pipeline system. We’re very excited about this so-called transition because what we’re transitioning into is a significant need in demand growth for natural gas.

JB: It seems like AI and data centers are going to be huge for the industry even if you’re not actually utilizing the AI.

MM: Exactly. Unlike crypto, they can’t go down. So, you’re not going to run a data center on solar; you’re not going to run a data center on wind. You’ve got to have natural gas.

Located on the Sabine-Neches Waterway between Beaumont and Port Arthur, Texas, Energy Transfer’s Nederland Terminal receives, stores and distributes crude oil, NGLs, feedstocks, petrochemicals and marine vessel fuel for refiners and other large transporters. Energy Transfer is working on the potential Blue Marlin Offshore Port, a deepwater crude export terminal offshore the Nederland Terminal. (Source: Energy Transfer)

JB: Obviously, exports are key, including your Nederland [Texas] terminal hub. But I also wanted to get your thoughts on the future of crude exports and where things might stand with the potential for the Blue Marlin Offshore Port [deepwater export terminal offshore of Nederland] down the road.

MM: I’ve joined our team over in Europe and parts of Asia, and it’s very clear there is more than enough support to support at least one [deepwater terminal]. And there may only be one, and we believe it will be ours. When you look at some of the competition, and there’s not a lot out there, they just don’t compare in a number of ways. One, they can’t easily get as many barrels into their projects as we can to ours. We also are brownfield. This isn’t a greenfield project like some of our competitors. The pipe is already laying in the Gulf. It already is going out to a dock to a terminal that we will be upgrading out offshore. So, yeah, we’ve got to build some tanks and build some pipe onshore, but we’ve got a huge advantage there, and I think the market has recognized that.

We’re working hard, we’re being very aggressive. This is a big commitment with the size and volumes of projects like this, but they [TotalEnergies and other potential customers] vastly prefer our project. It’s brownfield, less expensive, more supply flexibility, just a lot of pluses. We’re very optimistic that if a [project] gets to the finish line it will be ours.

JB: It went from a lot of competitors prior to the pandemic to very few, as you said. I don’t know if you can elaborate on this, but is it kind of a Blue Marlin versus SPOT [Enterprise’s Sea Port Oil Terminal] race at this point?

MM: That’s probably pretty fair.

JB: Staying on crude, I was going to ask initially how the Sunoco-NuStar deal factors into the broader ET umbrella, and if you would eventually want to consolidate more with Sunoco. But now you’ve announced the Permian Basin crude oil joint venture with Sunoco and the NuStar assets, so will you elaborate on that and if that kind of suffices on that front?

MM: We’ve got a really good relationship and partnership in some areas with Sunoco. This really is one of those deals that we believe is going to be better for the customers because this combined JV approach is going to give them more flexibility, more things to do with their oil. It’s also going to be very beneficial to our two partnerships. It really is one of those situations where one and one are going to be a lot more than two, whether it’s offering more downstream storage or downstream access to longer-haul pipes and a lot of other things we can do. So, we’re very excited about that JV.

JB: Switching back to gas and LNG, obviously LNG should be bullish for you regardless of what happens. And things are on pause a little bit, but can I get you to elaborate on just how things are looking with the FID [final investment decision] for the Lake Charles LNG? Obviously, you got the FERC [Federal Energy Regulatory Commission] approval, but then there’s the time extension issues [recently denied] and you’re maybe looking for partners on the project. So where do things stand?

MM: This one has been frustrating to us. Usually, when we set our minds to something, especially significant projects, sooner or later we get there. We still believe we’ve got a good chance of getting there. We had a lot of momentum. We felt pretty good about how we were proceeding. And then the pandemic hit that brought everything, at least from our standpoint, to a screeching halt. Then we had Russia-Ukraine, and that turned everything on a 180 in the other direction. We picked back up, had tremendous momentum, had already secured a significant amount of commitments. We’re in the process of solidifying enough commitments to get us to FID or close to FID. FERC had extended our permit. We were assured all along the way by the DOE [U.S. Department of Energy] and had no indication whatsoever that they might not extend it even up until about two weeks before they came out and said, “We’re not extending it.” So that certainly cut our legs out from under us. But the way I would describe it is, we’re not slowing down. Right now, we’re in negotiations with over 33 million tonnes that have an interest in our project, but they want to know that we’re for real, that we’re moving forward. So, we’re doing everything we can to solidify the commitments from our customers, to solidify the approximately 75% to 80% equity interest that we need to bring in. Our interest is only keeping about 20% of the LNG facility, but we’re continuing to push.

Our goals right now are to keep the EPC [engineering, procurement and construction] iron hot, keep that as fresh as we can and get to the end of this year, see what happens in November [presidential election], and be prepared to go to FID if all these boxes are checked. We’ve got the equity partners, we’ve got the minimum commitments we need, all the supply and everything we need is lined up. We hope to be ready to go to FID as soon as maybe another [Trump] administration would approve it fairly promptly sometime maybe in February. So that’s our goal. A lot of things can happen. We certainly had a tough road for all the reasons I mentioned. We’re not giving up, and we still think we’ve got a good chance of getting it to FID.

JB: So, a lot is hanging on the GOP winning the White House and the recent U.S. Supreme Court ruling overturning the Chevron deference doctrine that had given more authority to federal agencies, including the DOE?

MM: We feel confident if there’s an administrative change, they’re not going to come in and say, “Oh, you’ve got to do this. You’ve got to do that.” They’re going to say, “Follow the laws.” Whether it’s FERC, DOE, SEC, FTC, whatever, follow the laws and we can all play by those rules. We do believe there’ll be a sensibility, a reasonableness coming out of the new administration across the board. And that probably means pushing some new folks into the administrative arm of these regulatory agencies to follow the law, not to make a law, but to follow it.

JB: Lastly, I wanted to get your take on MLP trends and having fewer partnership players, and just the viability of that structure going forward?

MM: The MLP structure really was the big driver on the infrastructure buildout that you’ve seen in the U.S. When we look back on this, you can just see how it really changed starting from a little retail investment option and, all of a sudden, the institutionals started moving in and it worked. It accomplished exactly what it was set up to do and that’s helped incentivize, in a tax-efficient manner, the buildout of the midstream space within the U.S. When we look out, we have no intention of not being an MLP. We’re going to stay in that format. The consolidation [wave] is going to continue a little bit more, and you can probably see the ones out there that aren’t of the same scale and size that will probably be rolled up at some point.

I really think that the U.S. would not be enjoying this energy independence and security if it wouldn’t have been for the midstream space and what all we’ve done.

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.