Independence Contract Drilling Inc. floorhand Oscar Benevides waits to make a pipe connection while drilling Indigo’s CB Farm 19&30-9-12HC #1 in northern Sabine Parish. (Source: Tom Fox/Hart Energy)

[Editor's note: A version of this story appears in the May 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The Haynesville’s been keeping some secrets, everyone. It’s producing as much as ever—more than 10 billion cubic feet a day (Bcf/d). And there are about as many rigs drilling it as the Marcellus. Yes, the Marcellus.

Just 24 or so months ago, it remained stuck on a 6-Bcf/d axis after getting tangled in the spring of 2012 with a relentless sub-$3 strip. Strip’s still about $3, yet the Haynesville’s up 66%.

The rig count had declined to a dozen by 2016. There were whispers that there had been trolling: “Haynesville: Hi, Marcellus. Marcellus: New number, who dis?”

is uniquely

positioned

to capture

improved natgas

supply/demand

fundamentals

going forward,

said Welles

Fitzpatrick,

analyst with

SunTrust Robinson

Humphrey.

The oracle HaynesvillePlay.com quit regularly posting on New Year’s Eve 2015, closing with “It’s Been A Gas.”

Now, though, the Haynesville rig count is about 60. The Marcellus count, 65.

“The Haynesville is going to recapture its crown as the No. 1 gas play in the Lower 48,” Welles Fitzpatrick declared in Shreveport in February. The SunTrust Robinson Humphrey securities analyst addressed more than 1,000 attendees at Hart Energy’s second annual DUG Haynesville conference.

“While gas prices are depressed now, we expect that to improve in 2019 and beyond,” he said.

U.S. gas and associated-gas producers are forecasting significantly slower production-growth rates. Meanwhile, Gulf Coast LNG-export demand is continuing to grow.

“And when those prices do turn up,” he said, “the Haynesville is going to be one of few plays positioned to take advantage of that upturn.”

Natgas—in general—no matter from the Haynesville, Marcellus or another play—hasn’t mustered much love in the past half-dozen years as oil took center stage. But Tudor, Pickering, Holt & Co. analysts wrote in March that it’s won their attention again.

“It’s increasingly clear that global demand growth for natural gas—[the] preferred energy transition fuel—will likely outpace that of crude oil,” they wrote.

“So, despite the sometimes seemingly hyper-focus on all things Permian oil-related, it’s well worth investors broadening the energy opportunities lens and spending time analyzing and debating prospective global natural gas value chain winners/losers heading into the next decade.

“We’re undertaking this very exercise.”

The Jerry Jones Factor

Haynesville pure-play Comstock Resources Inc. was picked in 2018 by Jerry Jones, the Dallas Cowboys owner, to roll his existing E&P assets into, primarily in the Williston Basin. Comstock has drilled Haynesville wells since the early days, beginning in 2008.

RELATED: Executive Q&A: Jerry Jones

Haynesville operators—down to about a dozen these days as a result of ongoing play consolidation—report modern-recipe completions are proving the Bcf per lateral foot that was originally expected from the rock in 2008—and at a lower cost. Net/net: The Haynesville is economic now, even at $3 strip.

“In 2008 into ’12, we were alive, and it was an okay basin,” said Jay Allison, Comstock chairman and CEO. It retreated as natgas prices declined, but was reborn post-2014 by lower oilfield service costs and advancement in best completion practices.

“It competes against any region in the United States today—both oil and gas—with high-cash margins,” Allison said. “It’s good enough that Jerry Jones would put $620 million of his assets into the company—with no debt.”

Jones now owns 84% of Comstock shares. “You have one of the savviest businessmen in the world who saw the trophy and used his own money—he didn’t use private-equity money; he used his own money.”

And Jones knows oil and gas, Allison added. “He made his fortune in the oil and gas business. That’s what he bought the Cowboys with [in 1989] and now he’s back in oil and gas—in a much bigger mode with a public platform.”

Comstock had been drilling the Cotton Valley underlying the Bossier/Haynesville beginning in 2001 before Chesapeake Energy Corp. announced its horizontal Haynesville discovery in early 2008. First-generation Haynesville wells—Comstock drilled more than 100 of these between 2008 and 2012—were short laterals. Comstock was completing with stages about 250 feet apart.

“Today, they’re 150 feet [apart], but the main thing is spacing of our frack clusters,” Allison said. These used to be 50 feet apart; today, about 15 feet apart. “What it does is create a more effective completion around the wellbore.”

Comstock uses about 3,800 pounds of proppant per lateral foot in its current completion design. “It’s the same amount of proppant. We just condensed everything. We shortened our stages, and we increased the density of our spacing.”

Using this design—beginning in January of 2015, when Comstock decided to devote all its ongoing capex to its Haynesville asset—it’s drilled 70 of these new-generation wells.

“And it’s been consistent: Our IP rate has averaged 25 million cubic feet a day [MMcf/d] over all of those 70 wells,” Allison said.

Comstock also stayed with its core leasehold. “We tried not to drill in areas that weren’t already derisked. That’s kept us from having a blip on any well.”

A completed 4,500-foot lateral costs about $7.3 million; 7,500-foot, $9.8 million; and 9,500-foot, $11.5 million. “For all those lateral lengths, we’re getting from 2 to 2.4 Bcf [of EUR] per 1,000 feet. So a 4,500-foot lateral, you typically get about 10 Bcfe [Bcf equivalent],” Allison said.

probably had the

same [Haynesville]

economics as

you have today at

$3 gas, if you’re

looking at the

rate of return,

because the costs

have come down

and the EURs are

double,” said Jay

Allison, Comstock

Resources Inc.

chairman and CEO.

Original expectations for the Haynesville were about that much, but the first-generation wells weren’t proving it. “A 4,500-foot lateral back then, maybe you had 5 or 6 Bcfe [total EUR]. And the costs were a lot higher back then.

“So at $5 gas, you probably had the same economics as you have today at $3 gas, if you’re looking at the rate of return, because the costs have come down and the EURs are double.

“That’s how much the economics have changed.”

Market Valuation

Goodrich Petroleum Corp. president and COO Rob Turnham and other operators at the DUG Haynesville conference reported similar findings. Turnham said, “I remember $9 gas and margins that were less than we have currently, and it’s because service capacity was too tight.”

VIDEO - DUG Haynesville 2019 Operator Spotlight On Goodrich Petroleum Feat. Rob Turnham

New wells today are highly profitable, Turnham said. “That’s what is missing in the market. There’s an assumption that ‘it’s gas and, therefore, you can’t generate competitive rates of return.’

“This is wrong.”

With lower service costs, coupled with EURs of 2.5 Bcf per 1,000 feet, “even the short [one-section] laterals at $2.75 to $3 gas are 41% to 61% IRR,” Turnham said. Longer laterals, “we’re at 65% and 89%.” The 10,000-footers “are even better at 79% to 100%.”

Still, no love, though. Goodrich’s enterprise value was trading at 62% of PV-10 in March. On the measure of EBITDA, “we should be trading at an enterprise value at about $600 million,” Turnham said.

“And we’re trading at about 2.5 times [EBITDA, instead, for $250 million], which really doesn’t make much sense, but, unfortunately, that’s the market we’re in.”

Comstock’s Allison said, “There’s just no appetite. You look at the S&P 500. It used to be 16% energy. Now, it’s maybe 6%. The money’s going to Netflix, Google, Amazon … vs. energy.

“But, it will turn around after a while. You have to have what we have in order for them to have what they have: You have to have energy.”

Turnham said natgas equities, in particular, are “simply hated” in the market.

That’s the case even for Appalachian producers, according to Danny Rice, co-founder of Rice Energy Inc., which merged with EQT Corp. in 2017. While at Hart Energy’s Energy Capital Conference in March, he was asked what Rice Energy would be today had it not merged with EQT.

He quipped, “We would be an unloved pure-play Appalachian company along with the rest of them.”

RELATED: Things Get ‘Awkward’ For Rice Brothers Thanks To EQT Feud

had been that “the

Haynesville was

a high-cost basin.

Not anymore.

It’s low finding

cost,” said Rob

Turnham, Goodrich

Petroleum Corp.

president and

COO.

Turnham said at DUG Haynesville that a lot of why natgas stocks are “so hated … you have a bunch of [securities] guys who don’t want to do the work. They assume the Haynesville, Marcellus and other basins have a high-cost structure and, therefore, $2.75 gas doesn’t work.”

Haynesville well economics compete, though, Turnham said. “We’ve got to educate the market and get investors back to the space.”

Allison told Investor that he’s found an impression among equity traders that Haynesville economics are still like that of pre-2015, and many traders are only paying attention to oil anyway.

“People say, ‘I remember that old, burned-out play that didn’t have good economics.’ And that’s just not true now. A 7,500-foot well costs $9.8 million. Your EUR is 17 Bcfe and, at $3 gas, you get a 90% ROR.”

Turnham said, “If you look at low-cost basins, the reputation used to be the Haynesville was a high-cost basin. Not anymore. It’s low finding cost.”

Goodrich has a finding and development (F&D) cost of $1 or less per thousand cubic feet (Mcf). And the Haynesville’s proximity to Henry Hub in South Louisiana gets it a spot price of 15 or fewer cents less than Henry.

Combined with excess, existing takeaway capacity, “that’s a big, strategic advantage when comparing against the Marcellus,” Turnham said.

A six-well pad of 10,000-footers will IP between 150 and 180 MMcf. Goodrich’s LOE [lease operating expense] is about 5 cents per Mcf.

“It’s hard to fathom,” he said. “Your operating expenses are extremely low.” The wells pay out—in terms of cost—in 12 to 15 months.”

Investment in natgas equities has to continue, Turnham said. “On the supply side, if you look at the base of existing production, that decline is about 25% to 30%, which equates to about 25 Bcf/d.

“We can’t just stop.”

Sharing Data

Like Comstock, Goodrich began drilling in northwestern Louisiana in the early 2000s, initially for Cotton Valley, among other formations. Goodrich holds 23,000 net acres overall for Bossier/Haynesville pay.

completions used

between 28- and

35 million pounds

of proppant in

each. Per foot,

rates are between

3,800 and 5,000

pounds, said Frank

Tsuru, president

and CEO.

Most of its leasehold is in Bethany-Longstreet Field, straddling northern DeSoto and southern Caddo parishes in, Turnham said, “the best rock in Louisiana.”

In the past two years, it’s brought on 20 new-generation Haynesville wells. Its $10-million 2019 capex plan will get it 10 net wells averaging 7,500 feet in length. It operates 73% of its gross leasehold; Chesapeake operates most of the balance.

Nearly all of the play’s operators share drilling and completion information quarterly in a consortium, since “the land grab is over; all the land is basically HBP [held by production].”

Between 2008 and into 2014, Haynesville operators were drilling 4,600-footers, using about 1,000 pounds of proppant per foot in stages between 300 and 450 feet. “Our cluster spacing was quite wide too,” Turnham said. Goodrich was getting an EUR of about 1.1 Bcf per 1,000 feet.

More recently, in a Chesapeake-operated well, ROTC 1H in Caddo Parish, 5,000 pounds of proppant per foot was tested—analysts dubbed it and another the “Proppant-geddon” wells—with 90-foot frack intervals and cluster spacing between 20 and 50 feet.

Goodrich was nonop on it. Turnham said, “That’s the tightest we went.”

The well came in with 40 MMcf/d; it and a sibling, ROTC 2H, on the pad were at 19 Bcf of gross production at the 19-month mark.

The correlation of proppant per foot and EUR “is very high,” Turnham said. “There is no question you will get a higher EUR. The question is rate of return. What is the rate of return from the added proppant and more stages from tighter intervals?”

Goodrich has settled on a recipe of between 3,000 and 4,000 pounds for its operated wells, with slickwater, 125-foot intervals and 35 perforations per interval—five clusters; seven shots each. It finds it’s recovering a similar amount of gas in place by tightening the intervals rather than using more sand.

The Precarious Toe

Regarding 7,500-foot vs. 10,000-foot laterals, the latter appear to produce the highest IRRs, he said. But completions get tricky after 7,500 feet, Turnham said. “We would suggest 10,000 [-footers] have the highest IRRs. The question is of how much more risk you have at 7,500 to 10,000 feet.

“It’s not a risk of losing a well; it’s the risk of busting your AFE in cost overruns, mainly because, if you have to trip out of the hole and you’re at about 9,000 feet, that’s going to be three days or so to your AFE.”

The job’s costing $75,000 a day, “so you just added over $200,000 just to replace the bit or bottomhole assembly.”

Goodrich’s two most recent wells are 9,300-footers: Cason-Dickson 14&23 numbers 3 and 4, both 99% working interest, in Red River Parish. They peaked at 62 MMcfe/d, combined.

The wells join two others on the pad. Completed in early 2018, these IPed 54 MMcf combined, one from an 8,000 footer; the other, a 3,000 footer. The shorter lateral contributed 23 MMcf of the combined IP.

Analysts with Robert W. Baird & Co. reported in mid-March that Goodrich’s five operated Haynesville wells that came online in the 12 months ending Sept. 30, 2018, ranked No. 1 in the play—as well as when compared with Marcellus and Utica wells—in terms of first-three-month gross revenue per lateral foot ($773).

The No. 1 Marcellus well averaged $687; in the Utica, the No. 1 averaged $440.

Goodrich had one rig at work in early March and was expecting to add another. Its fourth-quarter companywide production averaged about 100 MMcfe/d. 2019 production is expected to average between 135 and 145 MMcfe/d with capex of between $90- and $100 million.

In 2018, it brought on 7.5 net wells (16 gross) in the Haynesville. Year-end proved reserves were 480 Bcfe. Proved reserve growth had an organic F&D cost of 92 cents per Mcfe.

After Goodrich’s Feb. 21 operations update, Seaport Global Securities LLC (SGS) analysts reported that “Haynesville well results continue to impress.” The PV-10 value of Goodrich’s proved reserves was $418 million; its enterprise value was $259 million, though, they added.

Capital One Securities Inc. analysts also noted that Goodrich’s enterprise value was well below its year-end 2018 PV-10 value, adding, “value investors should note.”

In recent months, “well cost assumptions also crept up” to $13.1 million for a 10,000 footer vs. $12.4 million, they wrote; however, operating expenses declined. Meanwhile, “EUR of 2.5 Bcf per 1,000 feet remains unchanged” and, for a two-section well, the new PV-10 per well is $14.4 million, up 23%.

Goodrich estimates IRR of 106% at $3 gas. 2018 F&D was $1.20 per Mcfe, up from 87 cents in 2017.

An RS Energy Group analysis of 12 Haynesville operators indicated Goodrich brings on the greatest first-three-month production in the play’s core in Louisiana at 1.6 Bcfe per well; first six months, just under 3 Bcfe.

In first-12-month production, it was No. 2 at about 4.5 Bcfe; No. 1 was just under 5 Bcfe.

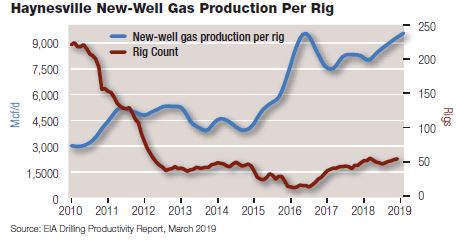

Haynesville operators are posting greater production per rig than in the play's early years, according to U.S. Energy Information Administration data.

The analysis was of wells completed since Jan. 1, 2016, among the operators. It included multiple lateral lengths. The operator in first place in first-12-month production has a longer average lateral length in the dataset, Turnham said.

“We’re producing as much as anybody. Certainly, the [Goodrich] completion recipe is working. And the acreage is in the right ZIP code.”

Zero To 1.3 Bcf/d

Indigo Natural Resources LLC got its leasehold start in the Haynesville in 2015. It’s leased more and also added some from Chesapeake and others for a total of about 435,000 effective net acres, 97% HBP, with net revenue interests (NRIs) of about 75% to 80%, mostly in DeSoto and Sabine parishes.

RELATED: Chesapeake Sells First Of Two Haynesville Packages For $450 Million

When getting started, the E&P aimed to grow gross production from 200 MMcf/d initially to 1 Bcf/d by year-end 2018. Frank Tsuru, Indigo president and CEO, said, “It was a very ambitious goal, and few people thought we could achieve it.”

Texas Haynesville]

competes with

the core of the

Haynesville [in

Louisiana] very

well. In fact, some

of this is better,”

said Alan Smith,

president and CEO,

Rockcliff Energy

II LLC.

But Indigo reached it. Current gross production is 1.3 Bcf/d; net, 950 million a day. Proved reserves are more than 4.5 trillion cubic feet equivalent (Tcfe). Total reserves are 17 Tcfe.

Indigo has eight rigs working in northwestern Louisiana. Most laterals are 1.5 section or greater. The 2018 average was 7,250 feet.

“Lateral length depends upon our acreage position,” Tsuru said. “A two-stack section results in 10,000-foot laterals, and a three-stack section results in 7,000-foot laterals.”

It also has two dedicated completion crews. “It’s not necessarily the number of drilling rigs that paces growth,” he said. “It’s truly the number of completions crews employed and the efficiency in which fracks are placed.”

In addition to new-well completions, Indigo was re-stimulating a 3,628-lateral-foot, former Chesapeake well, Nabors 12-11-12 H 1, of 2011 vintage in Red River-Bull Bayou Field, DeSoto Parish, about 12 miles southeast of Mansfield, in mid-March. The original well had IPed 18.6 MMcf on a 22/64-inch choke. Pressure was 7,845 psi.

Indigo made 46 new-well completions in 2018, using between 28- and 35 million pounds of proppant in each, totaling 1.3 billion pounds. Per foot, rates are between 3,800 and 5,000 pounds, Tsuru said.

It also owns Momentum Midstream LLC. Acreage it’s amassed over the years wasn’t under gathering/treating or shipping contract. Tsuru cited Indigo’s joint venture with Momentum as contributing to the E&P’s growth.

“We felt it was important. Not only did we want to control our destiny, but we wanted to keep the economics as much in-house as possible—as much of the value chain we thought viable.”

Momentum’s Longstreet plant in northern DeSoto Parish gathers, treats and compresses virtually all of the Indigo acreage production. It’s currently constructing a plant in northern Sabine Parish and discussing a third, in southern Sabine.

The Momentum system can deliver the rich gas of the Cotton Valley to third-party processors; the lean gas of the Bossier/Haynesville is treated at the Longstreet plant. Overall, Momentum gathers, treats and/or compresses some 1.2 Bcf/d; that’s expected to increase to 1.6 Bcf/d by year-end.

On water, Indigo put in a 100,000-barrel-a-day produced-water system, reducing its LOE, improving reliability and keeping up with its Cotton Valley wells that produce thousands of barrels of water a day. The Haynesville, meanwhile, comes with virtually no produced water.

Its freshwater system for completions has delivery capacity of 150,000 barrels a day and can store 3 million barrels.

Its latest integrated expansion is an in-field sand mine, Gen6 Proppant, that’s expected to open in the second half of this year. Indigo uses 100% local sand in its wells. “What we found was well performance was unaffected by using local sand over Northern White,” Tsuru said.

At full capacity, Gen6 is expected to produce 2.8 million tons a year: 50% of it, 70/140; the rest, 40/70. Its completion costs are expected to decline by about $250,000 per 7,500 footer.

LLC aims to be

a Haynesville

consolidator, said

Craig Jarchow,

president and CEO.

“We would like to

be a player in that.”

“If you drill 50 wells per year, it’s about $12.5 million. It’s substantial,” he said.

Taking The Core To ETX

Rockcliff Energy II LLC’s assets are primarily in Harrison, Panola and Rusk counties in and around the Carthage Field area on the Texas side of the border with Louisiana. It’s turning up EURs of between 2.5 and more than 3 Bcf/d per 1,000 feet of lateral in the East Texas Haynesville.

“We think it competes with the core of the Haynesville [in Louisiana] very well. In fact, some of this is better,” said Alan Smith, Rockcliff president and CEO.

The privately held producer is not new to East Texas. Smith and his teams acquired and developed ArkLaTex assets in five of six prior start-ups they built and sold for combined gross proceeds of $6.4 billion for it and partners. “It’s not by chance we ended up here [again],” Smith said.

In its newest venture, Rockcliff II acquired the East Texas and North Louisiana assets of Samson Resources II LLC for $525 million in 2017 as Samson narrowed its focus to the Powder River and Green River basins of Wyoming.

It has 276,000 net acres, more than 90% HBP, with some 78% NRI, producing 440 MMcf/d gross, up from 90 MMcf/d initially. Of its 34 new drills to date, 29 are in the Haynesville; five, in the Cotton Valley.

At 800-foot spacing, it has more than 1,400 Haynesville locations left to drill.

“A lot of people think East Texas is inconsistent, but, when you map it, there is a significant amount of gas here and it’s thicker than the [Louisiana] core, which makes it a lot easier to come in and wine-rack the development,” that is, stack wells.

Haynesville gas production has soared in just the past two years, according to EIA data.

First 30-day IPs range from 16- to 25 MMcf/d from laterals mostly between 7,500 and 10,000 feet. He added, “We’re very strict on the choke management to protect the reservoir. We’re not trying to give you any fluff here.”

Its current completion recipe is 100-foot spacing and 3,500 pounds of proppant per foot. A 7,500 footer, drilled and completed, costs about $10.5 million in Harrison County.

It has four rigs at work and expects to drill roughly 40 Haynesville wells this year—about as many as in 2018. Completions will be about 30, gross.

“A lot of people still don’t put East Texas [Haynesville] on their map,” Smith said.

“Not only do we want to see it put on their map, we want to see it get put on there as the core being extending into East Texas, because we clearly think that is the case based on the results we’re having.”

Rockcliff has legacy Cotton Valley production in its position as well. That formation in its area is delineated, but it requires additional geological understanding, compared with the Haynesville, Smith said.

48 unit, BPX

Energy, already

had good assets,

but the addition

of BHP Billiton

Ltd.’s Haynesville,

Eagle Ford and

Permian package

“upgrades us,”

said Mohit Singh,

BPX senior vice

president and

head of business

development and

exploration.

It will drill a few Cotton Valley wells this year. “We have a lot of Cotton Valley inventory, so we’ll get around to that [in the future].” It’s all HBP.

A Long-Term Hold

Goodrich’s Turnham said, “We too believe in choke management. We’re looking at 10 to 30 pounds of drawdown per day. So the productivity, once you start unloading fluid, becomes fairly obvious in the Haynesville.

“… We let the well tell us what the IP should be and, then, we monitor the pressure drawdown on a daily basis to keep that between 10 and 30 pounds.”

Castleton Resources LLC president and CEO Craig Jarchow mentioned pressure management as well. “By properly managing pressure, you can actually increase your recovery by about 20% by the end of the day,” he said. “It’s economically the right thing to do.”

Castleton entered the Haynesville with the $1 billion acquisition of Anadarko Petroleum Corp.’s East Texas portfolio in 2016 in Harrison, Panola, Upshur, Gregg and Rusk counties.

“We are one of the biggest producers in East Texas now,” Jarchow said.

Production, including from some leasehold northwest of Houston, is about 290 MMcfe/d, about 20% liquids. Proved reserves are 1.6 Tcfe, 79% gas and 17% NGL. PV-10 value is about $1.1 billion, about 74% PDP. Total leasehold is 163,000 acres.

In the Carthage area near the Texas-Louisiana border, Castleton halved the decline rate “just due to blocking and tackling on the operations side,” Jarchow said. It pared operating costs 30%. About half of its back-office functions are based overseas now, driving general and administrative expenses (G&A) per Mcfe down to about 14 cents.

“The Haynesville is performing well for us. The gas recoveries we’re seeing from long horizontal wells and high-intensity completions are much higher than even we expected, so our finding costs are materially lower than what we underwrote the acquisition at.”

In 2018, with a $3.09 realized gas price—Castleton is about 95% to 90% hedged—its EBITDAX was $2.23 per Mcf. In 2017, at an average of $3.09 gas, EBITDAX was about $2.20. “So we’re making well north of $2 on $3 gas,” Jarchow said.

The assets’ decline rate is about 22%—low due to the conventional production the portfolio includes.

Castleton’s business model isn’t that of build-and-sell. It’s owned 70% by Castleton Commodities International LLC (CCI) and 30% by Tokyo Gas America. CCI was Louis Dreyfus Highbridge Energy that was taken private in 2012 by roughly 25 family offices.

“The key there is these investors own shares in CCI directly. They don’t invest through funds, so there’s no 10-year life between our investors and us, which is a real advantage.

“It means we have long-term, patient, permanent capital—and lots of it.”

Plans To Consolidate

Castleton is aiming to be a Haynesville consolidator. “What’s next for the Hayneville? Ultimately, this basin is for sale,” Jarchow said.

He estimates all the East Texas portion of the Haynesville is for sale or will be for sale. “Same thing is true in North Louisiana.

“Obviously, this cries out for consolidation, and that is the right answer. That’s the right thing to do. That’s the strategic imperative.”

Jarchow believes only operational scale can truly capture the play’s profit potential. A $250-million company has scale for G&A and LOE—the fixed cost of the E&P business.

The next level is scale for capex—“keep rigs busy for a long period of time, keep pressure-pumping equipment busy for a long time, speak for a lot of proppant.” At $1.1 billion in PV-10 value, Castleton itself is “just barely big enough,” he said.

Next is scale “to drive midstream outcomes and to resist the rent-seeking behavior on the part of midstream companies.”

The “holy grail” of scale—“and this almost never gets talked about”—is a low capital cost. “You have to be at least a $2.5-billion enterprise value or $5- to $10 billion.”

A 1% lower cost of capital for Castleton, for example, increases its enterprise value by $100 million “and that’s just us: little Castleton.”

That holy grail of scale—“really, none of us in the basin on the upstream side is quite big enough yet, and we need to get there.”

During the unconventional revolution across the Lower 48, operators were building drilling inventory. The imperative was “to go find the next shale play, go find inventory.

“Well that game is over, and we don’t need any more inventory. So the name of the game, the strategic imperative, is to consolidate.”

The bid-ask in the Haynesville is a hurdle, but, “ultimately, the value of achieving scale trumps all of this. So we’re optimistic about consolidation. We would like to be a player in that.

“We have access to private capital—and lots of it.”

BP Plus BHP

An operator with that holy grail of scale, BP Plc bought out BHP Billiton, now BHP Group, onshore the Lower 48 in October, bolting on its Haynesville leasehold in northwestern Louisiana. The $10.5 billion total included acreage in the Permian and the Eagle Ford as well.

BPX Energy—BP’s Lower 48 unit—has deemed the Haynesville “the most revenue-generative gas play in the U.S.,” said Mohit Singh, BPX senior vice president and head of business development and exploration.

RELATED: BP’s BPX Energy Pursues US Shale Mission

The BHP bolt-on doubled BPX’s production there to 61,000 boe/d, 100% gas, and more than tripled its leasehold to 194,000 net acres. Gross drilling locations now total 727. After-tax IRR is estimated at 16% to 27% on new wells based on a $2.75 Henry Hub.

“We are very excited about increasing our footprint in the Haynesville,” Singh said.

BPX took over operations in March at the end of a transitional services agreement. BPX had six rigs operating in the Haynesville—all on the East Texas side of the play.

“Eventually, we will start progressing the locations on the Louisiana side,” Singh said.

It’s selling pre-existing onshore properties—exiting the San Juan, Green River and Anadarko basins—toward raising between $5- and $6 billion to balance the BHP package’s cost “and we have two years to do it,” Singh said.

Its northernmost East Texas property—in Glenwood, Woodlawn and Oak Hill fields, consisting of about 45,000 net acres—is for sale and has Cotton Valley, Haynesville and other potential, 100% HBP. These produce some 6,000 net boe/d, 75% gas, and annual operating cash flow of $35 million from 600 wells, 77% vertical. BPX operates 471 of the wells.

“Unfortunately, we haven’t done much in this field for a long time,” Singh said. “Every budget cycle, … just the scale and the running room was not there for us, so we decided not to fund these. But whoever acquires these will get these execution-ready projects.”

Essentially, it’s selling everything that isn’t in the Permian, Eagle Ford or Haynesville. The portfolio addition “has to displace whatever else you were doing.” BPX already had good assets, he said, “but BHP upgrades us.”

to produce 1.5

Bcf/d by 2023.

“On the M&A side,

we’re talking to

everybody,” said

John Howie, senior

vice president of

upstream.

Having also gained 3,390 drilling locations in the Permian and adding 1,402 locations in the Eagle Ford, “we’re looking at decades and decades of drilling inventory.”

On the matter of scale—BP has a commodities-trading business—so “we think of gas … all the way down the pipe, all the way down to the LNG tanker and where can you take that LNG tanker and create the most value.”

And, with its heft, it’s even offering to finance buyers. If buying a $1-billion package, for example, “I’m giving you a term sheet on $600 million of financing. You really only need to think about how to raise the remaining $400 million,” Singh said. And, of course, BP will offer hedging and marketing services as well, he added.

BPX’s annual capex had been about $1 billion. “Going forward, that number will be $2- to $2.5 billion. So it’s a significant investment by BP in the onshore business.”

Well-To-Beach

Building wellhead-to-market scale is Tellurian Inc., which owns a foothold in Haynesville-producing acreage. It has completed open seasons for planned pipelines from the Permian and Haynesville to ship natgas to its planned LNG export terminal in southwestern Louisiana.

In addition, it has a London-based international LNG-marketing unit.

Its upstream entry was in 2017 with 9,200 net acres—100% HBP, 92% operated, undedicated to takeaway contract—from Rockcliff II in DeSoto and Red River parishes and a small portion at the intersection of Sabine, DeSoto and Natchitoches parishes. Rockcliff had gained the acreage as part of the package it bought from Samson.

Net production is 4 MMcf/d; operated wells total 19; drilling locations, up to 138; total net resource, 1.3 Tcf.

Tellurian founder Charif Souki had said “‘I need you to buy 15 Tcf of resource,’” said John Howie, senior vice president, upstream.

Toward that, “at the top of our list is the Haynesville. We like it very much. It’s materially derisked, but materially undeveloped. It’s close [to the Gulf Coast], and it’s big.”

VIDEO - DUG Haynesville 2019 Operator Spotlight On Tellurian Feat. John Howie

Existing and previous Haynesville operators “cracked the code. They threw away the lock.” Tellurian’s plan is to pass new, improved Haynesville economics onto investors. “We’re going to enjoy wholesale [natgas] rather than retail,” Howie said.

Plans are to produce 1.5 Bcf/d by 2023. “That’s a resource of 15 Tcf.” Tellurian will be buying more property. “On the M&A side, we’re talking to everybody,” Howie said.

“There are some really good companies in the Haynesville. They’re all making money. At some point, we hope one of them will sell their assets to us.”

“[The Haynesville] does need to be consolidated. It doesn’t need to be consolidated with debt; it does need to be done with equity.” —Jay Allison, Comstock Resources Inc.

Tellurian is open to buying operated gas in other plays, too. “We are also looking at a couple other basins as well,” Howie said. Eagle Ford is one, “so maybe not exclusively Haynesville, but that’s where we’re concentrating right now.

“It’s derisked, and the Eagle Ford [gas] is becoming derisked. We have no desire to prove up these plays. We are not going to delineate and sell. We are holders for the life of these assets.”

Tellurian is drilling now with plans for four new wells and has participated in 12 nonops. “We are well aware we started with 0.004 Bcf/d,” he said. “We’re heading to 1.5 Bcf/d. That’s ambitious.”

But Indigo got to 1.3 Bcf/d in four years via leasing, acquisition and drilling, he said. “So we know it’s doable.”

Tellurian’s integrated natgas business model—produce, ship, liquefy, market—“makes Tellurian a little bit different” than other LNG exporters and exporters-to-be.

Its planned export facility near Lake Charles, La., will have loading capacity of 4 Bcf/d, which is “166 MMcf of natgas moving onto these ships an hour. That’s the cha-cha line.”

Meanwhile, internal estimates are that natgas demand in southwestern Louisiana—LNG terminals, the petchem industry—is going to grow by 2022 from 4 Bcf/d currently to 12 Bcf/d. “This is going to be the epicenter of natural gas for the entire United States.”

That’s where Tellurian’s pipelines come in—bringing Permian associated gas as well as gas from the Haynesville into the region. In addition, a Tellurian tap on an existing interconnect via a third pipeline is to assure 24/7 supply to the LNG plant.

Nonbinding open seasons for both the Permian and Haynesville pipes were oversubscribed. “In the Permian, producers are paying pipelines to take away their gas,” Howie said. “That’s our kind of gas market.”

The Tellurian model anticipates drilling and completion (D&C) of 88 cents per Mcf; operating, 36 cents; processing/transporting, 79 cents; and contingencies, 22 cents. That’s $2.25 delivered to the terminal. Then, there’s 75 cents to liquefy and “we’re on the beach at $3.”

With $20 billion of anticipated debt, there’s $1.50 per Mcf in interest. “So our cost for LNG on the water is about $4.50 per million Btu [British thermal units].” The JKM spot price for LNG in 2018 averaged about $10.

Skinnier Brackets

Comstock spent about $224 million in 2018 on Haynesville/Bossier development—$197 million on new-well D&C and the balance on refrack and other activity—for 49 (17 net) new horizontals with an average lateral length of 8,300 feet and completing 46 (16.1 net) of which 16 were drilled in 2017.

An additional 13 wells IPed an average of 28 MMcf each—ranging from 17 to 40 MMcf/d—from laterals averaging 9,470 feet.

2019 capex includes $340 million for D&C in the Haynesville/Bossier.

Comstock acquired 254 Bcfe proved in the Haynesville/Bossier in 2018 and added 1 Tcfe from new wells drilled and from proved undeveloped reserves (PUDs). PUDs grew to 299 (187.4 net) at year-end from the year-end 2017 number of 83 (60.7 net). Improved well performance added 41 Bcfe to proved estimates.

Comstock has four rigs drilling. It was negotiating this spring to pare Haynesville transportation costs between 10% and 20%, SGS analysts reported.

Its 2018 acquisitions were in two deals. From Shelby Shale LLC, it picked up 88% interest in Haynesville rights on 6,124 acres in Harrison and Panola counties, Texas. The price is to be paid over four years in carrying Shelby (12% working interest) in new wells up to $20.5 million.

Comstock estimates the property can take 33 (22.9 net) new wells, including 27 (22.4 net) operated by Comstock.

In the Louisiana Haynesville, Comstock bought Enduro Resource Partners LLC’s 21,000 gross (9,900 net) acres in Caddo and DeSoto parishes for $37 million.

The package includes 120 (26.2 net) wells producing 26 MMcf/d with 49 (14.7 net) of these producing from Haynesville. Proved reserves gained were 288 Bcfe. Comstock expects the property will take 112 (31.0) net new wells of which 21 (17.9 net) would be Comstock-operated.

Allison said of the consolidation trend in the Haynesville, “It’s like March Madness. The brackets get skinnier and skinnier.”

He added, “It does need to be consolidated. It doesn’t need to be consolidated with debt; it does need to be done with equity.

“Jerry Jones would like to help this company consolidate the sector by providing that equity. That’s a big advantage.”

SunTrust’s Fitzpatrick said at DUG Haynesville that historical gas supply/demand data show the difference between a bull gas-price market and a bear is between 2 and 4 Bcf/d of undersupply and oversupply.

VIDEO - DUG Haynesville 2019 Analyst Spotlight Feat. Welles Fitzpatrick

His optimism about U.S. natgas prices this year and beyond includes analysis of 60 public E&P companies’ gas-production-growth expectations. Guidance had been of a total of 10 Bcf/d added at year-end 2020, but that’s declined to 6 Bcf/d.

“That’s 4 Bcf/d,” Fitzpatrick noted. “Again, that’s the difference between a bull and a bear market.”

The “big dogs” of the Marcellus? Their growth estimates have come down 60%. “That’s driven by long-term factors,” including that “growth isn’t being rewarded.”

A new U.S. gas play hasn’t been discovered in 10 years, and “we definitely need new gas,” he said.

That will take higher natgas prices, and “the Haynesville … is uniquely positioned among the gas plays to take advantage of this confluence of events.”

Nissa Darbonne can be reached at ndarbonne@hartenergy.com.

Recommended Reading

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.