Joe Foran, chairman and CEO, Matador Resources Co., speaks at Hart Energy’s SUPER DUG Conference & Expo in Fort Worth, Texason May 15. (Source: Hart Energy)

Matador Resources continues to go all-in on the Delaware Basin, announcing a $1.9 billion takeover of private operator Ameredev II.

Experts have pondered whether Matador could be a target for M&A itself as oil majors and super-independents scour the Permian Basin for future drilling inventory.

But Joe Foran, Matador’s founder, chairman and CEO, insists that the Dallas-based E&P still holds a long runway of growth ahead.

After closing the Ameredev acquisition, Matador anticipates that its enterprise valuation will grow from $9.7 billion to approximately $11.5 billion.

It’s a major growth story for a brand that Foran originally launched in 1983 with just $270,000 in backing from friends and family.

“We’re hoping [the Ameredev deal] is recognized and appreciated in the market,” Foran said during a June 12 conference call with analysts.

“We know it makes us a bigger and better company,” he said. “We see a lot of potential and a lot of locations that we can turn into profitable wells.”

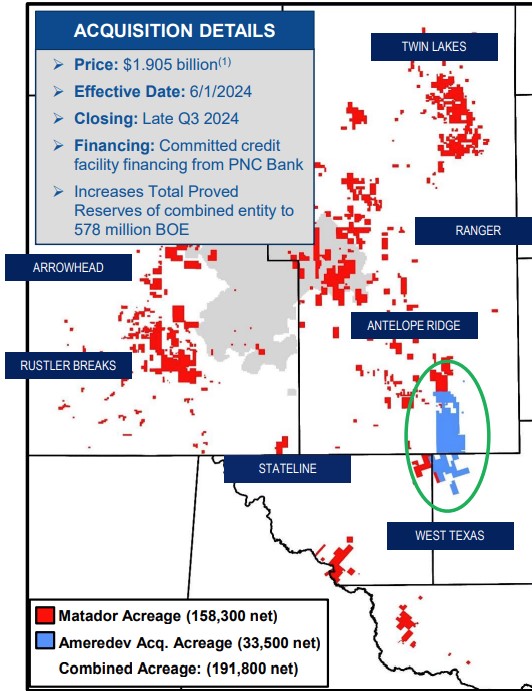

The $1.905 billion cash acquisition of Ameredev II, an EnCap Investments LP portfolio company, represents the largest deal in Matador’s corporate history.

Last year, Matador inked what was at the time its largest acquisition ever: a $1.6 billion takeout of Advance Energy Partners—another EnCap portfolio company.

Executives at Matador and EnCap go way back: Foran and EnCap founder Gary Peterson are both natives of Amarillo, Texas, and the two have shared a decades-long friendship.

“Similar to the Advance Energy transaction we closed in April of 2023, the long relationship with Gary and EnCap was critical to the smooth negotiation of this transaction,” Foran said in a news release.

RELATED

Matador Resources Buys EnCap E&P Ameredev II for $1.9B

Going long

Matador executives are excited about the blocky acreage position from the Ameredev acquisition, they said on the call with analysts.

The deal includes producing assets and undeveloped acreage in Lea County, New Mexico, and Loving and Winkler counties, Texas—an area that operators and experts largely consider to be the core of the Permian’s Delaware Basin.

The Ameredev portfolio includes about 33,500 contiguous net acres in the northern Delaware, adjacent to Matador’s existing Antelope Ridge and West Texas asset areas. Estimated production from the acquired assets is expected to average 25,000 boe/d to 26,000 boe/d (65% oil) during third-quarter 2024.

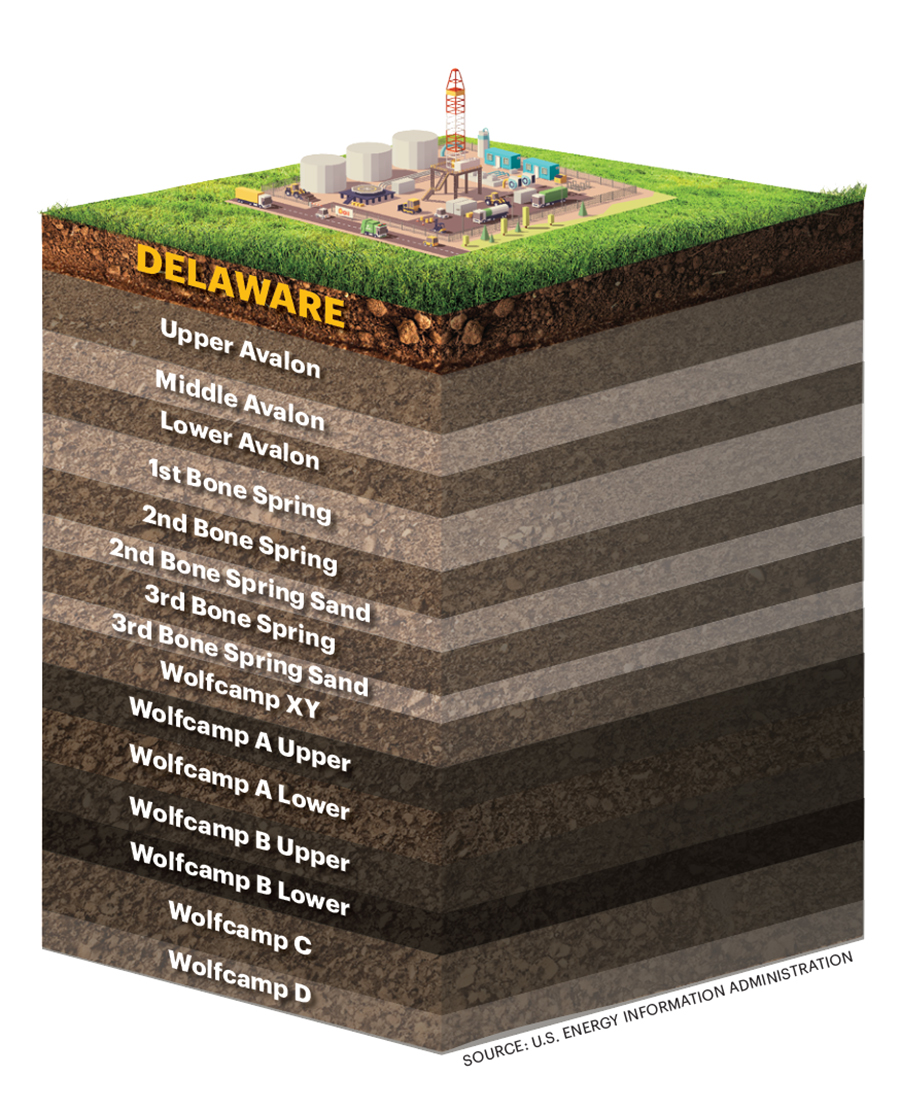

The deal is also accretive on inventory: Matador will add 431 gross (371 net) undeveloped locations for future drilling operations across the Wolfcamp and Bone Spring intervals.

Those inventory figures are based on developing roughly average 2-mile lateral wells, said Chris Calvert, Matador’s executive vice president and COO.

But after adding the blocky Ameredev acreage, Matador sees opportunities to drill longer 3-mile laterals in the future.

“The blocky-ness of the acreage and how contiguous it is does create potential to combine some things into longer 3-mile units,” said Tom Elsener, executive vice president of reservoir engineering and senior asset manager for Matador. “But I think it kind of starts around the 2-mile mark.”

About one-third of the undeveloped inventory is in the Wolfcamp A and Lower Bone Spring intervals, with the remaining two-thirds in the upper Bone Spring targets, Elsener said.

Matador also sees an opportunity to delineate another few dozen net locations in the shallower Avalon Formation.

The Ameredev inventory adds about four years of drilling runway to Matador’s portfolio, based on the company’s 2024 pace of 94 net completions, according to Gabriele Sorbara, managing director of equity research at Siebert Williams Shank & Co.

For EnCap, the Ameredev sale “looks like another winning deal” for the private equity firm, which has been particularly active in carving off pieces of its portfolio, said Andrew Dittmar, principal analyst at Enverus Intelligence Research.

EnCap is monetizing the Ameredev position for approximately $20,000 per acre for the undeveloped upside.

“While the acreage contains some very high-quality inventory, its position on the eastern edge of the Delaware Basin may impact multi-zone development relative to assets located to the west,” Dittmar wrote in a June 12 report.

RELATED

Decoding the Delaware: How E&Ps Are Unlocking the Future

Crystal ball

Analysts, investors and service companies alike are curious how Matador will approach drilling on the Ameredev asset once the deal closes—expected in the third quarter.

Amid a historic run of land-grabbing and corporate consolidation in the Permian, acquisitive public operators have largely targeted a buy-and-cut strategy once their deals close.

Permian operators are in no hurry to drill through their best rock. Realistically, why should they be?

Oil prices are healthy, clearly constructive for an active A&D market. Free cash flow has been near record levels. Operators are already returning oodles of cash to investors.

Only a few public E&Ps are planning to organically grow their oil and gas production through the drill bit in the near term.

That’s because operators and the broader market are essentially wholly focused, almost obsessively, on inventory depth and preservation.

Data shows public acquirers in the Permian drastically slashed rig activity on their new assets after their deals close.

Acquired private operator rig counts were reduced by nearly 70% in 2023 due to Permian upstream consolidation, according to data compiled by East Daley Analytics.

Before the deal closes, Matador expects Ameredev to continue operating one drilling rig and one completion crew, working through operations on 13 DUC wells.

Matador expects to continue operating a total of nine drilling rigs for the immediate future on the combined acreage, approximately 192,000 net acres. But the Ameredev position does immediately compete for development capital within Matador’s portfolio, the company said.

Permian M&A activity has centered more on the Midland Basin in West Texas, where Exxon Mobil recently acquired Pioneer Natural Resources for $60 billion.

But as dealmaking hits the Delaware, there are fewer private M&A targets still left standing in the basin.

A few notable names left outstanding across the Permian include Franklin Mountain Energy, Double Eagle IV and FireBird Energy II, Dittmar said.

Family-owned oil companies such as Mewbourne Oil and Fasken Oil & Ranch also stand out as attractive inventory holders in the Permian Basin, according to Enverus.

RELATED

Permian Pulse: Franklin Mountain Stands Out Among Delaware M&A Targets

Recommended Reading

Phillips 66’s NGL Focus, Midstream Acquisitions Pay Off in 2024

2025-02-04 - Phillips 66 reported record volumes for 2024 as it advances a wellhead-to-market strategy within its midstream business.

Dividends Declared Week of Jan. 13

2025-01-17 - With 2024 year-end earnings season underway, here is a compilation of dividends declared from select upstream, midstream and downstream companies.

Michael Hillebrand Appointed Chairman of IPAA

2025-01-28 - Oil and gas executive Michael Hillebrand has been appointed chairman of the Independent Petroleum Association of America’s board of directors for a two-year term.

Pinnacle Midstream Execs Form Energy Spectrum-Backed Renegade

2025-02-03 - Renegade Infrastructure, led by Permian-centric Pinnacle Midstream developers Drew Ward and Jason Tanous, have received a capital commitment from Energy Spectrum Partners.

Not Sweating DeepSeek: Exxon, Chevron Plow Ahead on Data Center Power

2025-02-02 - The launch of the energy-efficient DeepSeek chatbot roiled tech and power markets in late January. But supermajors Exxon Mobil and Chevron continue to field intense demand for data-center power supply, driven by AI technology customers.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.