As SLB, Baker Hughes and Halliburton rode waves of increased global drilling activity in first-quarter 2023, the Middle East and offshore drilling operations reflected a high increase in future activity. (Source: Shutterstock)

The three biggest oilfield service companies rode waves of increased global drilling activity to post stunning revenue gains in the first quarter. Based on the companies’ guidance, there will be a lot more to come this year.

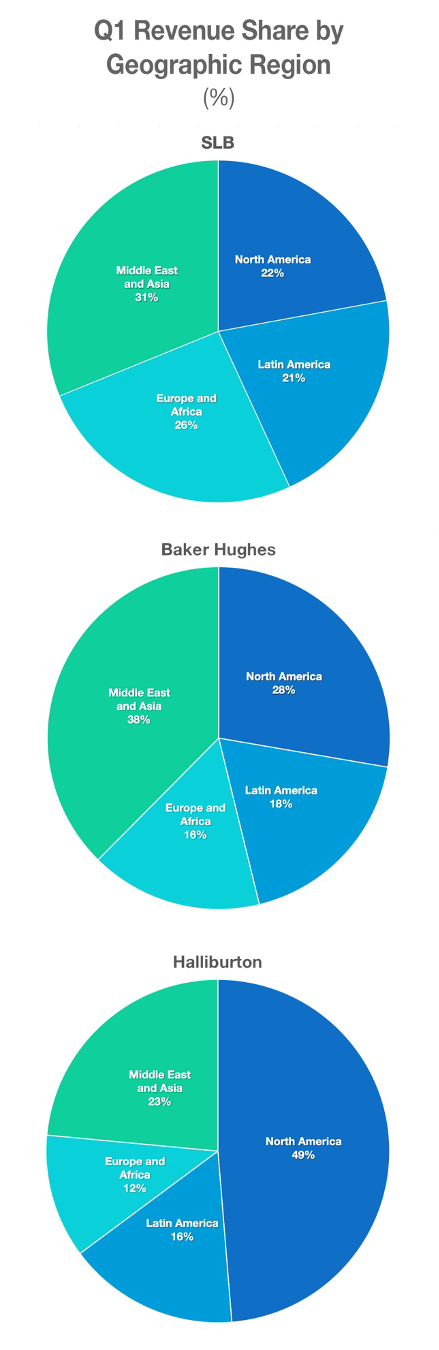

The year-over-year (yoy) quarterly gains for SLB (30%), Baker Hughes (19%) and Halliburton (33%) reflect strength across global regions, particularly in offshore segments. If there is a region to keep an eye on, though, it’s the Middle East.

“I would still argue early innings of activity increase in the Middle East,” Jeff Miller, Halliburton’s chairman, president and CEO, told analysts during the company’s earnings call. “I’m pleased with our growth. Rig counts aren’t necessarily at near peak, and I think we’ve got a lot of opportunity to continue to run.”

And everybody’s running: Halliburton’s Middle East/Asia revenues jumped 30% in the quarter yoy, Baker Hughes saw a 23% increase in the region and SLB’s revenues rose 18%. But it’s the outlook that drives the top executives’ confidence.

“The intensity of activity in [the] Middle East—that is, a mix of short-cycle and long-cycle development projects—this combination is unique,” said Olivier Le Peuch, CEO of SLB, during his company’s earnings call.

“In the Middle East, the largest-ever investment cycle has now commenced,” he said. “This will support ongoing capacity expansion projects over the next four years, in both oil and gas. Consequently, this year we expect to post our highest revenue ever in the Middle East, putting us on track to achieve our multi-year growth aspirations.”

Rystad Energy analysts noted in an April 26 report that huge demand for oilfield services in the region has boosted prices in the supply chain due to capacity constraints.

“The Middle East is already set to exceed all the other regions this year in terms of the offshore upstream sector, driven by massive projects in Saudi Arabia, Qatar and the UAE,” Rystad said. “Around $33 billion is set to go on offshore investments in the Middle East in 2023, a near doubling of the $17 billion seen just two years ago.”

Evercore ISI agreed with Rystad’s assessment.

“We recently reiterated our bullish stance on the oilfield services, equipment & drilling space as we remain convinced we are in the early stages of a long and strong upcycle for E&P spending, especially in the Middle East and broadly offshore,” Evercore said in a report.

Softening North America

In general, the big three reported analyst-pleasing numbers for first-quarter performance. Baker Hughes, in particular, garnered applause.

“This was the quarter and outlook we and… [Wall] Street had been waiting on, with a beat and a second-quarter guide above the Street estimates,” Piper Sandler bubbled in its report.

EBITDA of $782 million beat consensus expectations of $730 million and earnings of $0.28/share beat the consensus forecast of $0.26/share. Second-quarter EBITDA guidance of $845 million to $905 million contrasted with consensus estimates of $859 million.

Piper Sandler noted progress in Baker Hughes’ oilfield services and equipment segment, despite softening in the North American market compared to initial expectations. The analysts said they believe the company can hit its 20% EBITDA margin target by 2025.

“We expect this macro backdrop to still support a double-digit increase in global upstream spending in 2023 with multiple international projects being executed and the offshore development pipeline growing,” Baker Hughes Chairman and CEO Lorenzo Simonelli told analysts. “We continue to believe current environment remains unique with a spending cycle that is more durable and less sensitive to commodity price swings relative to prior cycles.”

SLB’s outlook is also strong, following a quarter in which its EBITDA of $1.79 billion beat expectations of $1.74 billion and earnings soared to $0.65/share from $0.36/share in first-quarter 2022.

The second quarter “is expected to see strong growth with seasonal recovery in the Northern Hemisphere, capacity expansion projects in the Middle East that are in various stages of ramp-up and robust activity in Asia and Sub-Sahara Africa,” Piper Sandler wrote. “This growth scenario provides support for broad sequential margin expansion across the Divisions and geographies.”

Halliburton beat financial expectations as well, with earnings of $0.72/share compared to the analyst consensus expectation of $0.65/share. The completion and production segment led the way, bringing in $3.4 billion in revenue.

Halliburton’s Miller cited many years of structural underinvestment in oil and gas as cause for the sector’s resurgence. Elevated customer demand and a tight services market will push growth in spending this year and in the future.

“We expect much of this investment will be directed towards development activity, which is great for Halliburton as it drives outsized demand for our products and services,” he said. “My view of this upcycle is confirmed by what I hear from our customers and see in the world’s oil and gas markets. The Halliburton outlook for both the current year and the long term is strong.”

No argument from Rystad.

“With energy security being a priority for most countries and supply chains remaining capacity constrained on many fronts, Rystad Energy believes market fundaments necessary for OFS [oilfield services] players to boost their financial performance will remain strong for the rest of the year,” the analysts wrote. “This aligns with our previous analysis highlighting the revenue growth potential and margin improvement trend expected for the OFS sector as a whole in 2023.”

Recommended Reading

Saudi Aramco Discovers 14 Minor Oil, Gas Reservoirs

2025-04-10 - Saudi Aramco’s discoveries in the eastern region and Empty Quarter totaled about 8,200 bbl/d.

Analysts’ Oilfield Services Forecast: Muddling Through 2025

2025-01-21 - Industry analysts see flat spending and production affecting key OFS players in the year ahead.

SM Energy Marries Wildcatting and Analytics in the Oil Patch

2025-04-01 - As E&P SM Energy explores in Texas and Utah, Herb Vogel’s approach is far from a Hail Mary.

Winter Storm Snarls Gulf Coast LNG Traffic, Boosts NatGas Use

2025-01-22 - A winter storm along the Gulf Coast had ERCOT under strain and ports waiting out freezing temperatures before reopening.

US Drillers Add Oil, Gas Rigs for First Time in Eight Weeks

2025-01-31 - For January, total oil and gas rigs fell by seven, the most in a month since June, with both oil and gas rigs down by four in January.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.