Two years before basin consolidation swept across the Lower 48 with mergers including Diamondback Energy and Endeavor Natural Resources, Chesapeake Energy and Southwestern Energy, and a record-setting list of basin-specific asset deals, leadership at Cimarex Energy and Cabot Oil & Gas were looking for more than oil and gas scale.

They wanted scope, too. And they didn’t want to rely on the fortunes of one commodity over the other.

The firms found each other and, in 2021, completed an all-stock “merger of equals” under the Coterra Energy name and “CTRA” ticker symbol on the New York Stock Exchange.

Coterra achieved scale and diversity at its onset: an enterprise value of $17 billion, a top tier asset base of 664,000 net acres across the Marcellus Shale, Permian and Anadarko basins and base production of 605,000 boe/d.

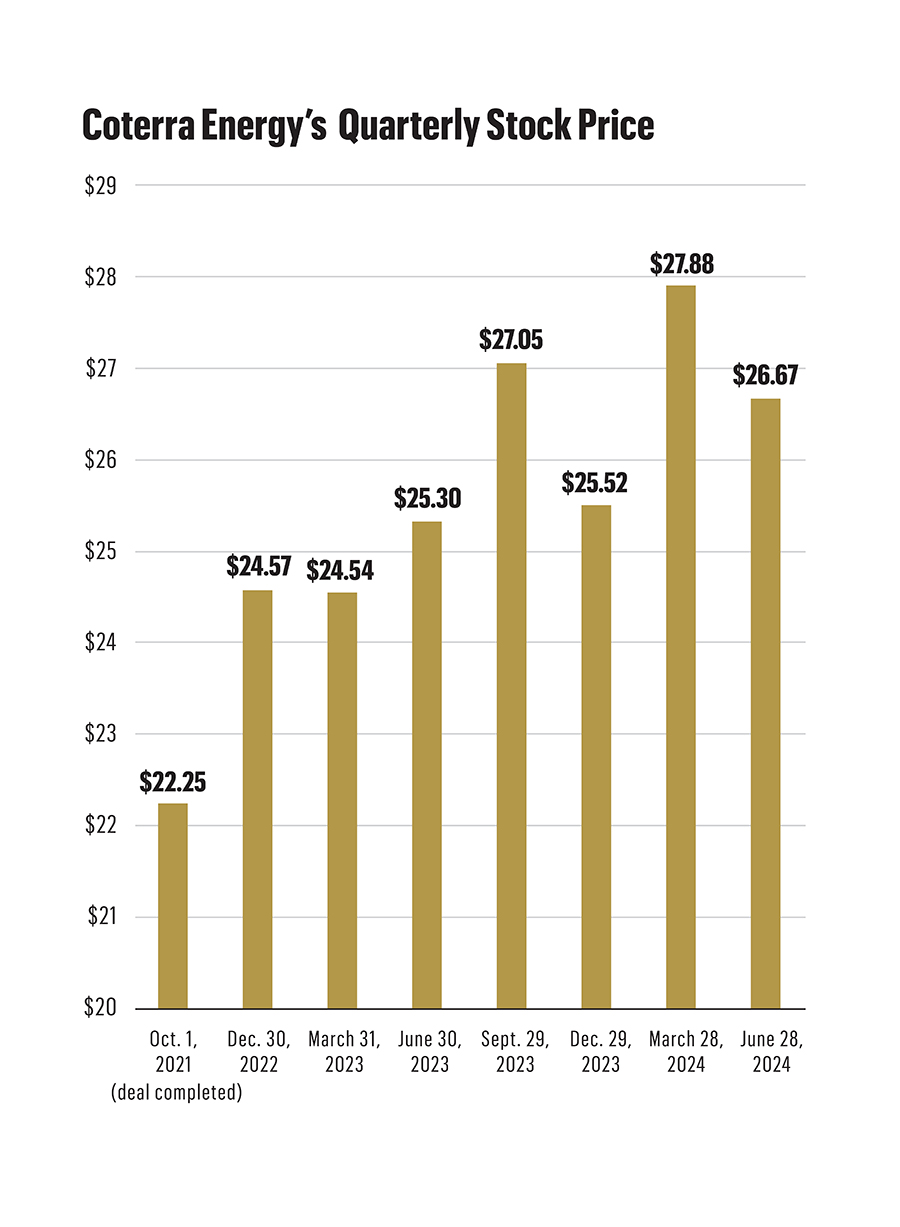

Now nearing its third anniversary, Coterra’s enterprise value is close to $22 billion—an increase of almost 30%. The firm routinely beats Wall Street’s quarterly expectations and its commodity-agnostic philosophy is working in its shareholders’ favor. The company has scaled down its natural gas activity with the relative weakness in prices; meanwhile, Truist Securities analysts say that next year could see a repeat of its current 10% year-over-year oil growth.

It’s all upside, really. Coterra is on track to generate more than $2.5 billion in free cash flow for 2025.

“We really do believe in decentralization, being in multiple basins, but also having a diverse revenue stream,” Coterra CEO Tom Jorden told Oil and Gas Investor (OGI). “If you can tell me which commodity will be the best one in the long run, then I’ll pick that and we can be a one commodity company. But we’ve never been very astute at picking. I don’t know that anybody has. So, we made the decision to try to diversify our revenue stream between gas and oil and then seek to have very low cost of supply in both commodities.”

Headquartered in Denver, Cimarex had mostly produced from Permian Basin operations in both Texas and New Mexico, as well as in the Anadarko Basin. Cabot leveraged a portfolio of some 173,000 gas-weighted acres in the Marcellus Shale.

Clearly, Coterra’s forbearers were onto something that the supermajors and large integrated firms have long understood: diversification matters. Since the Coterra closing, SM Energy is poised to enter the Uinta Basin with its acquisition of XCL Resources; Civitas Resources took a few steps outside its Denver-Julesburg base with its 2023 buys of Vencer Energy, Hibernia Energy IUII and Tap Rock Resources.

And in a deal that captures both the diversification and pure-play strategies, Continental Resources made a splashy debut in the Permian Basin when it bought Pioneer Natural Resources’ entire Delaware portfolio, leaving Pioneer a Midland Basin pure play, in late 2021. Pioneer has since been absorbed by Exxon Mobil.

The making of Coterra checked a lot of boxes: revenue and geographic diversity; low cost supply and high value assets; and low debt.

“Putting the two companies together was really structured around that philosophy: diversity of assets, diversity of revenue and low cost of supply. It was certainly unanticipated [by the market], and I’ll say a bit of a breaking from the herd at that point in time,” Jorden said. “But we’re really pleased with where we sit right now as a consequence of that merger.”

OGI visited Jorden at Coterra’s Houston headquarters in June for an afternoon discussion about the company’s strategy and culture.

Deon Daugherty: How did you find the wherewithal to go against the grain of what everyone else was doing with regard to M&A back in 2021?

Tom Jorden: We have convictions. We have a North Star as a management team. We really believe that the way to run a company is to first and foremost manage a company by return of invested capital. And so, we seek to have the highest returns we can, irrespective of commodity type. That was our guiding principle and the merger of the two companies certainly offered that to us.

We are agnostic on commodity and, from time to time, that’s not an easy discipline to maintain. But our experience tells us that gas and oil can cycle. At times it’s coupled and at times it’s decoupled. But what we saw in forming Coterra was the opportunity to have a very consistent revenue stream so that we weren’t subject to the vicissitudes of these cycles.

If you go back [several] quarters, natural gas was our dominant revenue source. And then over the last four or five quarters, oil’s been our dominant revenue source. But if you look ahead to the strip and look at what people are projecting for ’25, oil and natural gas will be about equal as revenue sources. And that’s exactly what we wanted to establish: a balanced revenue stream that would allow us to manage our business with greater predictability and greater consistency. It’s as simple as that.

DD: Coterra has produced extraordinary success, outpacing expectations just about every quarter since closing. Tell me more about your management philosophy, this “North Star” and how it guides your team.

TJ: Well, there are several elements to it. First and foremost, we believe that proper management of an E&P company is [based] around allocation of invested capital. We don’t manage by commodity type. We don’t manage by production growth targets. We look to see how much capital we’re going to invest and we really seek to find the highest returns on that capital.

Now, that also has several elements. First and foremost, you have to have a price file prediction. At whatever price file we look to see high returns, whether it’s the strip or a flat price file or a mid-cycle price file, we run them all. The second critical element is how much windage do you have between whatever price you forecast and how low you think the price could fall. That … provides your insurance, that provides your protection. If you make that investment, you will not destroy capital over those cycles because we’ve seen that in our business.

We’ve seen companies pull out the stops when prices are high and costs are high. They make massive investments and then the price falls and those investments end up destroying capital.

Then the third element is repeatability. You really think you have great repeatability. So those are really foundational elements of our capital allocation decisions.

But I’ll go further in answering your question. We really believe in the role of technology. We really believe in the power of human intellect when teamed with like minds or even unlike minds. So, at Coterra, we’re strong believers in a very open culture. We’re strong believers in a culture where people are not only welcome to disagree, but expected to disagree.

DD: How does that work in a room filled with experts?

TJ: If people have a contrarian viewpoint, we want to hear it—in real time. When we’re all in the room, we manage by eye contact. We make sure that people feel connected and therefore are empowered and trust that, if they disagree, that viewpoint’s welcomed.

We really do tolerate a high degree of technical debate. It’s foundational to our company. One of our North Stars is that people are expected, if they have a viewpoint based on the data, [to] bring it on. And I don’t care whether it’s somebody that’s a 30-year career person or somebody that’s three weeks out of school. If they’re in the room and they have a viewpoint based on data, we really want to hear that. We work hard with a shared conviction that our company be a true meritocracy of ideas, and that there are as few barriers to really bright people sharing their viewpoints as we can possibly muster.

DD: That sounds very unusual.

TJ: Well, it’s not for everybody.

It can be very uncomfortable. In my experience, anything in life that you want to accomplish—be it business, physical fitness, spirituality, relationships, education—ultimately it comes down to a very simple choice between progress or comfort.

If you want to make progress, you have to be prepared to be very uncomfortable. And we do not strive for Coterra to be a comfortable place to work. And we say that unapologetically, but not uncomfortable politically because we don’t tolerate politics.

It’s all on the tabletop. We make eye contact, we have a commitment that the worst thing we’re going to say is when we’re making eye contact and in person and it works.

DD: So, give me an example of how one of those conversations might play out.

TJ: We tell our board and our organization that we’ve been very successful—and we’re worried sick over it. We never want success to get in the way of future innovation. Good is never good enough. There are always ways you can push the envelope. You have to have a certain amount of pride, but also humility because we work in an industry with some really bright people and some great organizations. We look at our competitors and we try to learn from them.

We try to be willing to change our minds constantly on better ways to do things. And we have a lot of examples of that. We’re altering our spacing right now in the Windham [Row] project, which is in Culberson County [Texas]. We talked on our recent earnings call that most of our prior experience tells us that in the Delaware Basin, where we have multiple target zones stacked on top of one another, depending on the vertical distance between these zones, that we can develop them one at a time and come back later and get the zones above or below.

But this isn’t true for everywhere in the Delaware Basin. We recently saw some data that suggested that that may not be wholly true, so we’re rethinking it and going back to looking at some stack tests.

We’ve also been very forward in the adoption of artificial intelligence or machine learning. That can help one be objective. I won’t say it doesn’t have bias, but I’ll say it has very manageable bias, whereas with humans, it’s harder to manage our biases.

DD: What are some of the ways that you’re using artificial intelligence?

TJ: We started by applying it to subsurface modeling. Then we said to ourselves, if we could get artificial intelligence to do a good job at well prediction, then that would be the Holy Grail. There may be 15 or 20 different parameters when you drill a well that govern the production response depth, lateral length, completion type, geological parameters, spacing, parameters.

Generally, they fall into three main categories: geological; completion and spacing; and geometry. But within those three major buckets, there may be 15 impactful parameters, and these are very expensive experiments. If you’re doing them in the field, you may permeate one or another, but you will exhaust yourself financially to try all different iterations.

Machine learning gives you the ability to say, “Well, here’s this combination of the 15 parameters; how well did it actually do in practice?” We have a lot of different wells with machine learning, we can look at how each one of them had the geology, the completion, and the spacing, and see how good a job we can do at predicting that outcome.

Because if you can nail that, you get to the point where you give me the 15 parameters that govern that well, and I can do a very effective job of predicting what it should have produced. And if that is truly a good match over what it did produce, then I’m off to the races. I don’t have to spend $10 or $15 million on every iteration of those parameters. I can let the machine do it and I can find the optimum solution, not only optimize my production, but optimize my return on capital.

We’ve really instituted that heavily here. It’s changed our thinking across the board. We’ve taken machine learning from something that people were initially a little suspicious about, and we’ve turned it into a technology where, here at Coterra, there’s no meaningful operational meeting where machine learning isn’t at the table. And our operations people insist on it because they’ve seen the value and the illumination it brings to any meaningful problem set.

Look, we didn’t get it right straight out of the chute. We had some false starts, but we really found a rhythm where today our machine learning on predicting well performance is outperforming our best and brightest reservoir engineers.

DD: And this is being applied across your assets?

TJ: Yes, across the assets.

DD: What has that done to your growth plans?

TJ: It helps us more effectively complete our wells. It helps us get more per well. We’ve talked about some of our spacing. In the Permian and the Delaware Basin a couple of years ago, we talked at length about that. We thought—and again, not everywhere, but in many places—we thought we were able to drill fewer wells in some cases, fewer wells than our competitors, and recover the same volumes. And we’ve demonstrated that time and time again where we’ll be next door to an operator that may be drilling one or two additional wells, and yet our drilling spacing unit is producing equivalent volumes to the one next door. We’re doing it with $15-$20 million less investment.

Now, that’s not true everywhere. But I will say that the application of machine learning has really given us a more sophisticated understanding of spacing and completion efficiency.

DD: I want to dig in a bit more on how Coterra has managed to outperform by almost every metric during every quarter.

TJ: Certainly by having an open organization; the power of that is remarkable. Now, every company has their own culture and every company believes in their own culture. Or if they don’t, they should reform their culture.

I heard it said years ago, and it’s been attributed to many, … but the quote is, “In the long run, the only source of competitive advantage a company has is its culture.”

And that has absolutely been my experience. Assets will come and go, and much as I hate to say it, people will come and go. But if a culture can survive that and be organic, then that can be the heartbeat of a company. I think Coterra is a meritocracy. We really encourage open collaboration amongst our people, either across business units or vertically. We don’t silo people, nor do we have a viewpoint that says management is command and control.

You put that philosophy in with a multi-basin approach and all of a sudden you have a place where good ideas spread like wildfire. An innovation in the Marcellus can quickly find its way to the Anadarko or the Permian, or vice versa. We have a lot of collaboration going on every day between our business units, sharing best practices, querying one another on problem solutions, and it’s given real dividends.

Certainly, we have a great field staff, very dedicated field staff, but we really have a very focused organization that sets a standard of excellence for one another. That may sound trite, it may sound arrogant. But we really do have an expectation of one another that is based upon a shared commitment to excellence.

DD: So, taking that approach is how Coterra returned 90% of its free cash during the first quarter? Is that size of return sustainable?

TJ: Well, we’ve committed to 50% plus, but we’ve refused to get into an arms race on cash return promises.

We’ve seen that companies will say 50%, then another company will say 75% and another company will say 90%. And we’ve just refused to make those promises because, simply put, we really believe in commitments and that’s why we make so few of them. We don’t want to make commitments that we’re not going to honor. And so, we’ve returned in advance of what we’ve telegraphed, but we’re happy to do that. We have a tremendous balance sheet, great cash flow, low cost of supply, and quite frankly, the last few years have been really good years in our business.

DD: During the first-quarter call, you discussed being optimistic about natural gas. It’s been especially volatile, so how do you hold that disposition?

TJ: Well, it’s hard not to be optimistic about natural gas as you look ahead in the future. We’re kind of all born optimists in this business because we’re in a business where you can do everything, and yet it can go really badly. The commodity price can fall out from underneath you suddenly and without warning. Or you can have terrible mechanical problems and overexpend or lose holes, or we have weather events. Just a lot can go wrong in this business.

Our psychological defense against that is our optimism, and we’re an optimistic group generally in our business. Sometimes, when you find optimism, it’s just kind of people’s stubborn reaction to reality. But when it comes to natural gas, I will say it’s very difficult to look at the fundamentals of either U.S. or global energy and not see a really strong role for natural gas.

DD: How do conversations about phasing out fossil fuels figure into your calculus?

TJ: It depends on who’s doing the talking. Are there NGOs [non-governmental organizations] or environmental groups doing that talking? Are there government officials and regulators doing that talking? Or is the consumer doing that talking? Because those are all very different voices.

When we look at the consumer’s behavior and the marketplace, we see very strong future for our products, both oil and natural gas, particularly hardened by the growing conversation around electricity generation, about the need generated by data center growth and artificial intelligence adoption and what that’ll mean for U.S. power demand and the role of natural gas in satisfying that demand.

So, you give me the choice between all of those voices, I’m going to take the marketplace, and I think the marketplace is sending us pretty clear signals that our products will be needed for many decades to come. And it will be a healthy business within a certain behavior set that is responsible, that attempts to deliver our products as emissions-free as we can, and that is not tone deaf to the energy transition. I mean, all of that is true simultaneously.

Recommended Reading

Trump Nominates E&P Advocate Sgamma to Head Bureau of Land Management

2025-02-12 - If confirmed by the Senate, Kathleen Sgamma, president of the Western Energy Alliance, would oversee management of approximately 245 million acres of surface lands.

RWE Slashes Investment Upon Uncertainties in US Market

2025-03-20 - RWE introduced stricter investment criteria in the U.S. and cut planned investments by about 25% through 2030, citing regulatory uncertainties and supply chain constraints as some of the reason for the pullback.

What's Affecting Oil Prices This Week? (Feb. 3, 2025)

2025-02-03 - The Trump administration announced a 10% tariff on Canadian crude exports, but Stratas Advisors does not think the tariffs will have any material impact on Canadian oil production or exports to the U.S.

BP Cuts Renewable Investment, Boosts Oil and Gas in Strategy Shift

2025-02-26 - BP aims to grow oil and gas production to between 2.3 MMboe/d and 2.5 MMboe/d in 2030.

Confirmed: Liberty Energy’s Chris Wright is 17th US Energy Secretary

2025-02-03 - Liberty Energy Founder Chris Wright, who was confirmed with bipartisan support on Feb. 3, aims to accelerate all forms of energy sources out of regulatory gridlock.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.